South Africa Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade), By Region (Gauteng, Western Cape, Eastern Cape, North West, Others) ... Read more

|

Major Players

|

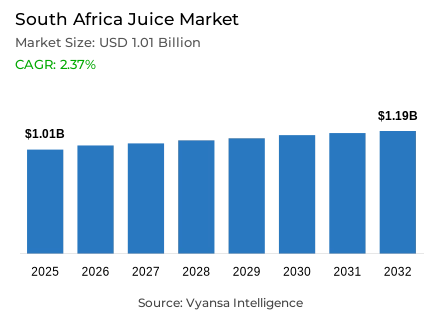

South Africa Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in South Africa was estimated at USD 1.01 billion in 2025.

- The market size is expected to grow to USD 1.19 billion by 2032.

- Market to register a CAGR of around 2.37% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 75%.

- Competition

- More than 15 companies are actively engaged in producing juice in South Africa.

- Top 5 companies acquired around 55% of the market share.

- Lactalis SA (Pty) Ltd, Spar South Africa (Pty) Ltd, Pacmar Pty Ltd, Pioneer Foods (Pty) Ltd, Clover SA (Pty) Ltd etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 85% of the market.

South Africa Juice Market Outlook

The South Africa juice market is in a period of stable recovery and modernisation after the supply chain shocks of the last few years. The market is estimated to grow to USD 1.01 billion in 2025 and to USD 1.19 billion in 2032, with a CAGR of approximately 2.37% in the 2026-32 forecast period. This expansion is supported by the stabilisation of prices and a high consumer shift towards the natural health advantages of fruit and vegetable juices.

One of the major forces behind this growth is the 100% juice segment, which currently holds a leading market share of 75%. end user are becoming more interested in pure juice as a convenient source of vitamins and antioxidants, and they are willing to compromise natural sugars with clear nutritional value. Functional offerings, including probiotic shots and coldpressed versions of brands like Sir Fruit, and an increasing focus on sustainable, recyclable packaging by large players like LiquiFruit, further drive innovation.

The competitive environment is typified by the fact that Clover remains a leader with its Clover Krush brand that has been able to adjust to the onthego trends with new canned products. At the same time, the major retailers like Woolworths and Shoprite are rapidly expanding their privatelabel products that offer highquality and lowprice products that appeal to valuesensitive end user.

The sales channel is still skewed towards physical retail, with the offtrade channel taking 85 per cent of the market. Although supermarkets remain the main venue of bulk and impulse purchases, ecommerce is becoming the most rapidly expanding channel. Convenience is being redefined by platforms like Checkers Sixty60 and Woolworths, which offer fast delivery and customised digital offers to make the juice category available to a wide range of South African end user.

South Africa Juice Market Growth DriverStabilising Food Inflation and Strong Citrus Supply Restoring Juice Purchasing Confidence

Improved price stability drives a revival in the consumption of juice. According to Statistics South Africa, the average headline consumer inflation is 5.3% in 2024 and levels off in 2025, with food inflation decreasing relative to previous highs. This stabilization lowers the pressure on household disposable income after steep cost increases of 20232024. With the reduction in price volatility, end user will feel confident to buy packaged beverages, such as 100% juice forms. The economic stabilization creates the positive environment of the discretionary beverage spending recovery and category volume growth.

At the same time, South Africa remains a major citrus producer, thus guaranteeing the availability of raw materials locally. According to the Department of Agriculture records, the citrus export volume is over 165 million cartons in 2024, which is a good production capacity. Better supply terms minimize cost shocks and enable manufacturers to sustain competitive prices, which strengthens volume recovery in the juice category. The two drivers are the increased consumer affordability and the stability of manufacturer costs due to the combination of inflation moderation and strong domestic citrus production. These converging forces create structural support to the continued growth of the juice category, which allows both volume growth and margin protection due to constant input costs and restored purchasing power.

South Africa Juice Market ChallengeHealth Promotion Levy Sustaining Structural Pressure on Higher-Sugar Beverage Demand

The Health Promotion Levy in South Africa is still a structural limitation on sugary drinks. The 2025 Budget Review by National Treasury confirms that the tax on sugarsweetened drinks is still in effect as a national health policy. The tax will be imposed on drinks that contain more than 4 grams of sugar per 100 ml, which will directly affect the pricing policies of juice varieties that have a higher%age of natural sugar. This economic pressure imposes economic disincentives on naturally sweet juice formulations and promotes reformulation to lowersugar formulations.

Regulatory pressure is also strengthened by public health considerations. According to the World Health Organization (2024), 27 per cent of adults in South Africa live with obesity, and noncommunicable diseases are a major health burden. The growing awareness of sugar consumption puts more scrutiny on the fruit juice even though it is positioned as natural. This climate is forcing manufacturers to focus on reformulation, portion control, and sugar reduction technologies to cushion demand. The overlapping of fiscal policy and the health of the population puts a longterm strain on the conventional juice formulations. Manufacturers have to strike a balance between natural product positioning and sugar reduction needs, and have to comply with regulations and preserve taste profiles and consumer acceptance.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Juice Market TrendRapid Digital Grocery Adoption Reshaping Juice Route-to-Market and Discovery

Retail online grocery stores are radically changing the beverage buying behaviour. According to the State of the ICT Sector Report 2025 by the Independent Communications Authority of South Africa, mobile broadband penetration is over 100 % SIM penetration, indicating that internet access is widespread. This connectivity enables quick expansion of online grocery ordering and appbased retailing in urban centres, establishing new sales channel channels and consumer touchpoints outside the traditional brickandmortar retail formats.

This digital shift is further enhanced by urbanization. According to the World Bank, 67.8% of the South African population lives in urban centers in 2024, which contributes to the need to have conveniencebased shopping experiences. The ecommerce websites provide fast delivery, customised offers, and a wider range of products compared to the physical shelves. In the case of juice brands, this transition facilitates the premium product visibility, functional differentiation, and directtoconsumer interaction via digital ecosystems. The digital grocery trend is a core channel transformation, with convenience, personalisation, and breadth of assortment as its key priorities. This opens up opportunities to brands that have good ecommerce, digital marketing, and logistics optimisation that facilitate smooth online shopping experiences in the urbanised, digitally connected consumer market in South Africa.

South Africa Juice Market OpportunityEPR-Driven Circular Packaging Transition Enabling Sustainability-Led Differentiation

Environmental sustainability provides a strong competitive growth opportunity. In 2024, the Department of Forestry, Fisheries and the Environment reports that South Africa seeks to boost recycling rates within the Extended Producer Responsibility framework. Beverage packaging is directly in this area of regulation, promoting recyclable and lightweight designs. The regulatory sustainability requirements generate compliance imperatives and at the same time provide differentiation opportunities to early adopters who exhibit environmental leadership and packaging innovation.

At the same time, the World Bank (2024) states that South Africa is experiencing growing climate and resource pressures, which strengthens the need to implement energyefficient manufacturing and sustainable supply chains. The brands of juices that invest in recyclable cartons, material intensity, and energyefficient production are in line with the national sustainability priorities. This placement boosts brand equity among the environmentally conscious end user and satisfies the changing regulatory demands. Sustainability opportunity allows manufacturers to accomplish two goals: regulatory compliance and premium positioning by being a genuine environmental steward. Packaging innovation, carbon footprint reduction, and integration into the circular economy can be used to differentiate brands with credible sustainability commitments, as they tap into the increasing number of environmentally conscious end user in the resourceconstrained, sustainabilityoriented market environment in South Africa.

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the South African juice market, where 100% Juice grabbed a market share of 75%. This subcategory has proven to be the most resilient and dynamic, benefiting from a normalization of raw material costs and a wide variety of available flavors. end user increasingly prioritize "pure" options over diluted nectars, viewing them as a functional wellness supplement rather than just a beverage.

This dominance is further supported by a trend toward "cleanlabel" products and natural health positioning. As South Africans become more wellnessoriented, they are gravitating toward juices that offer high vitamin C and antioxidant content without added sugars. Manufacturers are responding by focusing on 100% fruit and vegetable blends, utilizing strategic promotional activities and flavor innovation to maintain high household penetration and consumer trust across the country.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

This segment with the highest share within the Sales Channel is the OffTrade, which managed to capture 85% of the market share. This huge majority comprises largescale retailers and supermarkets such as Checkers, Woolworths, and Pick n Pay, which act as the main hub for juice sales channel. They achieve this through their accessibility, attractive bundle deals, and the fact that more end user are opting for private labels, thus encouraging end user to visit their physical stores for their primary juice needs.

It is undeniable that the digital landscape has seen a significant rise, but the offtrade remains the mainstay of the industry because of the "onestop" benefit that it provides for family shopping needs. This has seen many of the supermarkets embracing omnichannel retail strategies to counter the threat of digital retailers. This offtrade segment has managed to cover a wide range of the market because of the different economic situations that many South Africans find themselves in, thanks to the presence of heritage brands as well as private labels.

List of Companies Covered in South Africa Juice Market

The companies listed below are highly influential in the South Africa juice market, with a significant market share and a strong impact on industry developments.

- Lactalis SA (Pty) Ltd

- Spar South Africa (Pty) Ltd

- Pacmar Pty Ltd

- Pioneer Foods (Pty) Ltd

- Clover SA (Pty) Ltd

- Pick 'n' Pay Retailers (Pty) Ltd

- Henties Juices Cape CC

- Real Beverage Co The

- Rhodes Food Group

- Darling Ltd

Competitive Landscape

The competitive landscape of juice in South Africa in 2025 remains concentrated, with Clover SA retaining leadership through its Clover Krush range, supported by no-added-sugar positioning, flavour innovation and new convenient can formats targeting younger, on-the-go consumers. Strong supermarket partnerships and consistent brand equity reinforce its visibility and consumer trust. At the same time, private label is intensifying competition, with retailers such as Woolworths Holdings Limited, Shoprite Holdings and Pick n Pay expanding premium and functional variants while maintaining competitive pricing. Enhanced quality perception, loyalty integration and greater supply chain control are enabling private label to capture incremental share across mainstream juice segments.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- South Africa Juice Market Policies, Regulations, and Standards

- South Africa Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- South Africa Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Region

- Gauteng

- Western Cape

- Eastern Cape

- North West

- Others

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- South Africa 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Pioneer Foods (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Clover SA (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pick 'n' Pay Retailers (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Henties Juices Cape CC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Real Beverage Co, The

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lactalis SA (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Spar South Africa (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pacmar Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rhodes Food Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Darling Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pioneer Foods (Pty) Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.