US Honey Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Table Honey/Consumer Honey, Industrial Honey/Ingredient Honey), By Nature (Organic, Conventional), By Source Type (Monofloral (Acacia Honey, Clover Honey, Manuka Honey, Others), Multifloral), By Processing Type (Raw, Filtered, Pasteurized, Ultra-filtered), By Form (Liquid, Creamed/Whipped, Comb, Crystallized/Granulated, Powdered), By Application (Food & Beverages, Pharmaceuticals, Nutraceuticals/Dietary Supplements, Personal Care & Cosmetics, Foodservice), By Distribution Channel (Retail Offline (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Pharmacies/Health Stores), Retail Online (E-commerce Platforms, Direct-to-Consumer)), By Packaging Type (Glass Jars, Plastic Bottles/Squeeze Bottles, Tubs, Sachets/Single-Serve Packs, Bulk Drums/Containers), By End User (Household Consumers, Food Manufacturers, Beverage Manufacturers, Pharmaceutical Companies, Cosmetic & Personal Care Companies, Foodservice Operators), By By Region (West, Midwest, South, North, Northeast) ... Read more

|

Major Players

|

US Honey Market Statistics and Insights, 2026

- Market Size Statistics

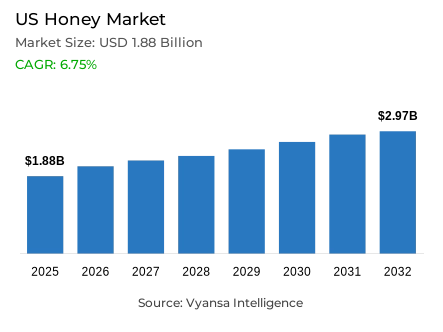

- Honey market size in US was valued at USD 1.88 billion in 2025 and is estimated at USD 1.98 billion in 2026.

- The market size is expected to grow to USD 2.97 billion by 2032.

- Market to register a CAGR of around 6.75% during 2026-32.

- Product Type Shares

- Table honey/consumer honey grabbed market share of 55%.

- Competition

- More than 10 companies are actively engaged in producing honey in US.

- Top 5 companies acquired around 35% of the market share.

- Rice Honey LLC (Local Hive Honey), Bee Maid Honey Limited, GloryBee Inc., Sioux Honey Association Co-op, Barkman Honey LLC etc., are few of the top companies.

- Packaging Type

- Glass jars grabbed 45% of the market.

US Honey Market Outlook

The US honey market was valued at USD 1.88 billion in 2025, establishing a commercially resilient foundation within the country's expanding natural food and premium sweetener ecosystem. Projected to advance from USD 1.98 billion in 2026 to USD 2.97 billion by 2032, the sector registers a CAGR of approximately 6.75% across the forecast horizon. The category advances on the back of health-led consumption, stronger end user interest in natural sweetening options, and steady household demand across everyday food and beverage applications reflecting a demand environment shaped by deliberate, wellness-oriented purchasing behavior rather than passive commodity consumption.

Growth is further being shaped by a structural shift in end user preference toward cleaner and more premium product positioning. Within honey consumption, buyers demonstrate rising interest in products associated with natural sourcing, raw variants, and organic appeal a premiumization dynamic that is elevating honey from a commodity pantry staple into a considered, quality-conscious purchase across health-aware household segments. At the same time, supply-side pressure from a declining domestic bee base remains an important factor influencing product availability and overall category sentiment, creating a market environment where supply constraint and demand premiumization operate simultaneously to reshape commercial dynamics.

Packaging trends reflect equally strong end user demand for familiarity, quality signaling, and shelf appeal. Glass jars account for 45% of the category, confirming that end users continue to prefer packaging formats associated with product purity, visual transparency, and premium presentation credentials. This packaging preference supports stronger in-home use frequency and gifting occasion relevance particularly within segments where quality cues at the point of purchase exert meaningful influence over brand selection and purchase conversion decisions.

The category's overall outlook remains well-supported by health awareness, natural-product preference, and favorable product perception across sweetening use cases. Even as the supply environment remains under pressure, honey continues to benefit from premiumization momentum and stronger end user attention toward organic and raw positioning. Policy support mechanisms and market-backed promotion provide additional commercial momentum creating a more resilient operating environment for market participants navigating both supply-side constraints and evolving end user expectations through 2032.

US Honey Market Growth DriverRising Metabolic Health Awareness Redirects Sweetener Selection Toward Natural Alternatives

The substantial and growing scale of diabetes and prediabetes prevalence across the US population represents a primary structural driver of honey demand, functioning as a health-awareness catalyst that keeps end user attention persistently focused on sweetener ingredient choices across everyday food and beverage consumption occasions. As households manage blood sugar concerns with greater consciousness and dietary intention, the sweetener selection decisionhistorically a low-engagement commodity purchasebecomes a deliberate health-adjacent choice in which honey's natural origin, minimal processing profile, and perceived nutritional complexity relative to refined sugar create meaningful competitive differentiation. This health-motivated sweetener reappraisal behavior is progressively expanding honey's addressable end user universe beyond traditional culinary users into a broader health-conscious demographic that evaluates sweetener choices through a wellness lens.

The population-scale of the health pressure driving this demand dynamic is documented with precision by the CDC. An estimated 40.1 million people in the United States have diagnosed or undiagnosed diabetes, equivalent to 12.0% of the total population, while an additional 115.2 million adults are identified as having prediabetescreating a combined metabolic health-affected population of extraordinary commercial scale whose sweetener purchasing decisions are shaped by health management motivations. This scale of metabolic health pressure sustains high sugar-conscious purchasing intensity across the US end user base and supports honey's positioning within end user sweetener decision frameworksparticularly among households seeking natural, minimally processed alternatives to refined sugar in daily tea, breakfast food, home remedy, and recipe applications through 2032.

US Honey Market ChallengeDeclining Bee Colony Health Tightens Supply Conditions and Pressures Price Stability

The continuing deterioration of domestic bee colony health and the resulting contraction in honey production capacity constitutes the most critical structural challenge confronting the US honey market, creating a supply constraint environment that simultaneously pressures product availability, complicates retail pricing management, and introduces production volatility risk that undermines the supply chain planning confidence of packers, distributors, and retail buyers. The structural nature of this challengerooted in the complex intersection of pesticide exposure, habitat loss, parasitic threats, and climate-related foraging disruptiondistinguishes it from cyclical agricultural production fluctuations and establishes it as a persistent operating constraint that requires strategic rather than tactical management responses from market participants.

The quantitative severity of this supply deterioration is documented with precision by USDA NASS. The number of colonies producing honey in the United States fell to 2.41 million in 2025, representing a 7% decline from 2024confirming that colony contraction is an active and accelerating trend rather than a stabilizing condition. Total honey production in 2025 dropped to 116 million pounds, reflecting a 14% year-on-year decline, while producer honey stocks fell 15% to 34.8 million poundssimultaneously reducing current availability and depleting the inventory buffer that historically moderated retail price volatility during production shortfalls. The direct commercial consequence of this supply tightening is reflected in average honey prices rising 27% in 2025 to USD 3.05 per pounda price inflation dynamic that creates margin pressure across the value chain and affordability headwinds for volume-sensitive retail segments through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Honey Market TrendOrganic and Raw Positioning Captures Growing Share of Premium end user Demand

The rising end user preference for organic and raw honey formats represents a defining structural trend within the US honey market, reflecting the broader clean-label movement's progressive penetration into the sweetener category and the growing end user appetite for food products that communicate minimal processing, transparent ingredient provenance, and verified natural authenticity. This premiumization trend is reshaping the competitive landscape by creating a high-value product tier within the honey category where brand differentiation is constructed on certification credentials, sourcing transparency, and processing methodology communication rather than price competitiona dynamic that rewards investment in organic certification, artisanal production narrative, and premium packaging presentation.

The institutional infrastructure supporting organic honey's market development is documented with specificity by USDA AMS. The Organic Market Development Grant program reached USD 85 million in total awarded funding by August 2024 and is expected to benefit more than 119 million producers, buyers, and end usersdemonstrating the scale of federal investment in building the organic supply chain and retail ecosystem infrastructure that enables certified organic honey brands to access mainstream distribution channels. The confirmation by USDA AMS that honey may be certified under USDA organic labeling rules provides the formal certification pathway through which honey brands can access the organic premium positioning framework and compete credibly within the broader organic food retail ecosystem. As end user interest in natural-product purchasing continues its structural deepening, organic and raw honey formats are expected to capture progressively larger share of total category value through 2032.

US Honey Market OpportunityFederal Policy Support Framework Provides Structural Resilience for Industry Expansion

The comprehensive federal policy support architecture available to the US honey market creates a strategically significant commercial opportunityproviding financial resilience mechanisms, production loss compensation programs, and market development investment that collectively stabilize market economics during difficult production periods and actively build the end user demand infrastructure that supports long-term category expansion. For honey producers and brands navigating the supply constraint environment created by declining colony counts and rising production costs, federal program access represents a meaningful operational risk management resource that preserves commercial viability during periods when market conditions alone would threaten producer sustainability.

The specific financial mechanisms comprising this policy support framework are documented with precision across multiple official sources. The USDA Farm Service Agency's Honey Program maintains the national loan rate for honey at 69 cents per pound for crop years through 2025, with loan deficiency payments not subject to payment limitationproviding a price floor mechanism that protects producer revenue during market price troughs. The Emergency Livestock Assistance Program covers honey bee colony, hive, and feed lossesbasing payments on a%age of fair market value and providing direct financial compensation for the colony loss events that are simultaneously driving the market's supply constraint challenge. The National Honey Board's assessment rate of USD 0.015 per pound funds research, promotion, and end user education programs that expand domestic honey demand at the category levelcreating a collective investment mechanism through which all market participants benefit from professionally managed end user awareness and demand development activity through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Honey Market Segmentation Analysis

By Product Type

- Table Honey/Consumer Honey

- Industrial Honey/Ingredient Honey

The segment with highest market share under Product Type is Table Honey/Consumer Honey, which is about 55% of the total market. This dominating stance demonstrates the structural congruency between end user honey formats and the daily household consumption events such as beverage sweetening, breakfast food applications, bakery and home health remedy preparation upon which the category is based in terms of repeat purchase. Having over half of the total market value held in one product category, table honey has become the commercial mainstay of the US honey market determining the priorities of retail shelf space allocation, brand investment planning, and supply chain planning needs across the entire value chain. Its hegemony proves that the main commercial applicability of honey has not yet been changed to the context of specialty or utility use.

The structural leadership of table honey is maintained by the universal familiarity of the product in house-holds, the versatility of application and high repeat purchase loyalty dynamics combined together to form a demand pattern with a steady baseline velocity and predictable seasonal amplification. Income, age and dietary preference cohorts of end users have long-standing table honey purchase behavior that is not disruptive but supported by the continuing premiumization of the category of organic, raw and varietal positioning of table honey to raise the average unit value of the product but not alter the primacy of the occasion of consumption. With an increasing health-conscious sweetener choice behavior spreading across the US end user population and the honey natural product standing as a stronger brand competitor to refined sugar products, the position of table honey as the primary income earner and a competitive focus of the category is likely to be maintained structurally through 2032.

By Packaging Type

- Glass Jars

- Plastic Bottles/Squeeze Bottles

- Tubs

- Sachets/Single-Serve Packs

- Bulk Drums/Containers

The largest market share segment by the Packaging Type comprises of Glass Jars and it constitutes about 45% of the overall market. This dominance is an indication of the underlying importance of the packaging trust signal in the purchase decision-making process of honey a subcategory whereby the product color, texture, clarity and perceived purity are physically assessed by the end user at the point of purchase as the primary quality proxies. The dominating share of glass jars is a testament to the fact that the US honey end user base is highly attentive to the transparent format of packaging that allows them to inspect the product directly and convey the message of high quality and purity positioning through material quality and appearance characteristics that cannot be reproduced using plastic squeeze bottle and opaque packaging formats, with the same degree of end user credibility especially in the organic and raw honey markets where the perception of quality and

Glass jars have a structural leadership based on its two-fold commercial relevance to both daily household and high-end gifting eventthe two main honey consumption settings where packaging presentation plays the most direct role in brand perception and justification of purchase. At gifting context in particular, glass jar honey products have significantly larger unit values and brand differentiation compared to functionally identical products in other packaging formatscreating a premiumization channel of brands that invest in glass packaging design, labeling refinement, and quality of retail presentation. With the ongoing end user relevance of organic and raw honey positioning, and the overall trend of the category toward increased premiumization, the glass jars connection with the integrity of the products, their natural authenticity, and their premium shelf values will continue to maintain and ensure their leadership in the packaging format well into 2032.

List of Companies Covered in US Honey Market

The companies listed below are highly influential in the US honey market, with a significant market share and a strong impact on industry developments.

- Rice Honey LLC (Local Hive Honey)

- Bee Maid Honey Limited

- GloryBee Inc.

- Sioux Honey Association Co-op

- Barkman Honey LLC

- Dutch Gold Honey Inc.

- Golden Heritage Foods

- Nature Nate’s Honey Co.

- Savannah Bee Company

- Miller Honey Company

Market News & Updates

- Nature Nate’s Honey Co, 2025:

Nature Nate’s launched three naturally flavored honeys in November 2025—sea salt, lemon, and vanilla—to expand honey usage beyond traditional breakfast occasions into drinks, charcuterie, brunch, and everyday food applications. This is a strong U.S. honey-market update because it shows clear product innovation in flavored table honey, helping the brand widen usage occasions and strengthen premium shelf differentiation.

- GloryBee Inc, 2026:

GloryBee announced Hot Honey with Smoky Chipotle in February 2026, positioning it as a new honey product showcased at Expo West with custom formulation and flexible-packaging appeal for private-label and ingredient customers. This is important for the U.S. honey market because it reflects continued innovation in hot honey and flavor-led honey formats, which are helping move honey beyond basic sweetening into sauces, snacks, and value-added food applications.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- US Honey Market Policies, Regulations, and Standards

- US Honey Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- US Honey Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Table Honey/Consumer Honey- Market Insights and Forecast 2022-2032, USD Million

- Industrial Honey/Ingredient Honey- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Organic- Market Insights and Forecast 2022-2032, USD Million

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- By Source Type

- Monofloral- Market Insights and Forecast 2022-2032, USD Million

- Acacia Honey- Market Insights and Forecast 2022-2032, USD Million

- Clover Honey- Market Insights and Forecast 2022-2032, USD Million

- Manuka Honey- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Multifloral- Market Insights and Forecast 2022-2032, USD Million

- Monofloral- Market Insights and Forecast 2022-2032, USD Million

- By Processing Type

- Raw- Market Insights and Forecast 2022-2032, USD Million

- Filtered- Market Insights and Forecast 2022-2032, USD Million

- Pasteurized- Market Insights and Forecast 2022-2032, USD Million

- Ultra-filtered- Market Insights and Forecast 2022-2032, USD Million

- By Form

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- Creamed/Whipped- Market Insights and Forecast 2022-2032, USD Million

- Comb- Market Insights and Forecast 2022-2032, USD Million

- Crystallized/Granulated- Market Insights and Forecast 2022-2032, USD Million

- Powdered- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Food & Beverages- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceuticals- Market Insights and Forecast 2022-2032, USD Million

- Nutraceuticals/Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Personal Care & Cosmetics- Market Insights and Forecast 2022-2032, USD Million

- Foodservice- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets/Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Stores- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies/Health Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Direct-to-Consumer- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- Glass Jars- Market Insights and Forecast 2022-2032, USD Million

- Plastic Bottles/Squeeze Bottles- Market Insights and Forecast 2022-2032, USD Million

- Tubs- Market Insights and Forecast 2022-2032, USD Million

- Sachets/Single-Serve Packs- Market Insights and Forecast 2022-2032, USD Million

- Bulk Drums/Containers- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Household Consumers- Market Insights and Forecast 2022-2032, USD Million

- Food Manufacturers- Market Insights and Forecast 2022-2032, USD Million

- Beverage Manufacturers- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceutical Companies- Market Insights and Forecast 2022-2032, USD Million

- Cosmetic & Personal Care Companies- Market Insights and Forecast 2022-2032, USD Million

- Foodservice Operators- Market Insights and Forecast 2022-2032, USD Million

- By Region

- West

- Midwest

- South

- North

- Northeast

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- US Table Honey/Consumer Honey Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Source Type- Market Insights and Forecast 2022-2032, USD Million

- By Processing Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- US Industrial Honey/Ingredient Honey Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Source Type- Market Insights and Forecast 2022-2032, USD Million

- By Processing Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Sioux Honey Association Co-op

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Barkman Honey LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dutch Gold Honey Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Golden Heritage Foods

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nature Nate’s Honey Co.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rice Honey LLC (Local Hive Honey)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bee Maid Honey Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GloryBee Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Savannah Bee Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Miller Honey Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sioux Honey Association Co-op

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Nature |

|

| By Source Type |

|

| By Processing Type |

|

| By Form |

|

| By Application |

|

| By Distribution Channel |

|

| By Packaging Type |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.