Saudi Arabia Honey Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Table Honey/Consumer Honey, Industrial Honey/Ingredient Honey), By Nature (Organic, Conventional), By Source Type (Monofloral (Acacia Honey, Clover Honey, Manuka Honey, Others), Multifloral), By Processing Type (Raw, Filtered, Pasteurized, Ultra-filtered), By Form (Liquid, Creamed/Whipped, Comb, Crystallized/Granulated, Powdered), By Application (Food & Beverages, Pharmaceuticals, Nutraceuticals/Dietary Supplements, Personal Care & Cosmetics, Foodservice), By Distribution Channel (Retail Offline (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Pharmacies/Health Stores), Retail Online (E-commerce Platforms, Direct-to-Consumer)), By Packaging Type (Glass Jars, Plastic Bottles/Squeeze Bottles, Tubs, Sachets/Single-Serve Packs, Bulk Drums/Containers), By End User (Household Consumers, Food Manufacturers, Beverage Manufacturers, Pharmaceutical Companies, Cosmetic & Personal Care Companies, Foodservice Operators), By By Region (East, West, South, Central) ... Read more

|

Major Players

|

Saudi Arabia Honey Market Statistics and Insights, 2026

- Market Size Statistics

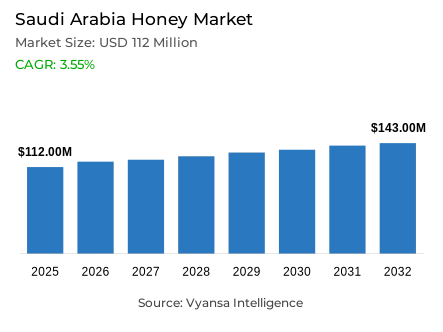

- Honey market size in Saudi Arabia was valued at USD 112 million in 2025 and is estimated at USD 119 million in 2026.

- The market size is expected to grow to USD 143 million by 2032.

- Market to register a CAGR of around 3.55% during 2026-32.

- Product Type Shares

- Table honey/consumer honey grabbed market share of 70%.

- Competition

- More than 10 companies are actively engaged in producing honey in Saudi Arabia.

- Top 5 companies acquired around 30% of the market share.

- Royal Honey, Queen Bee Honey, Raheeq Honey, Balqees Honey, Hatta Honey etc., are few of the top companies.

- Packaging Type

- Glass jars grabbed 55% of the market.

Saudi Arabia Honey Market Outlook

The Saudi Arabia honey market was valued at USD 112 million in 2025, establishing a commercially stable foundation within the Kingdom's expanding premium food and natural wellness consumption ecosystem. Projected to advance from USD 119 million in 2026 to USD 143 million by 2032, the sector registers a compound annual growth rate of 3.55% across the forecast horizon. Growth is supported by a convergence of steady household demand, strengthening premium local honey positioning, and rising quality awareness across the category reflecting a market whose commercial momentum is anchored in authenticity-led differentiation and institutional supply chain development rather than volume-driven commodity expansion.

The domestic production foundation underpinning this market's supply architecture is both substantial and institutionally supported. Saudipedia documents Saudi Arabia producing over 5,000 tons of honey annually, operating with more than two million beehives, and maintaining a registered beekeeper base exceeding 20,000 confirming that the Kingdom's honey production ecosystem has achieved meaningful scale and organizational formalization. The Saudi Reef program's empowerment of over 80,000 people, delivery of more than SAR 3 billion in direct financial aid, and support for the production of approximately 250 million kilograms of agricultural goods collectively demonstrate the depth of institutional commitment to rural agricultural development that creates a structurally favorable operating environment for domestic honey producers seeking to invest in quality improvement, production scaling, and premium market positioning.

Despite the strength of domestic production, the category's import dependence creates a structural competitive dynamic that shapes pricing, quality standards, and labeling compliance requirements across the value chain. World Bank WITS data confirms Saudi Arabia imported 18,509,200 kg of natural honey valued at USD 68.66 million in 2024 a volume that substantially exceeds domestic production and maintains intense competitive pressure on local producers across retail price points and quality positioning tiers. This import intensity is accompanied by a tightening compliance environment Saudi Arabia's WTO notification of a new mandatory honey labeling requirement in October 2025 mandates the phrase "Not suitable for infants below 12 months" on all honey and edible apiculture products effective 29 December 2025 raising the operational compliance threshold for both importers and domestic brand owners simultaneously.

The forward outlook through 2032 is defined by the progressive elevation of regionally identified premium Saudi honey varieties, the expansion of value-added apiculture product categories beyond liquid honey, and continued formalization of quality standards that reward investment in certified, traceable, and authentically positioned honey products. Table honey and consumer honey command 70% of the product mix confirming that direct-consumption formats remain the category's commercial backbone while glass jars account for 55% of packaging demand, reflecting end user preference for transparent, premium-presentation formats that support quality inspection and shelf credibility. The SFDA's recommendation to store honey in its original container specifically a glass jar or food-safe plastic container while avoiding metal containers to reduce oxidation risk provides official quality guidance that reinforces glass packaging's structural market leadership. These converging demand, supply, and regulatory dynamics define the market's commercial trajectory through 2032.

Saudi Arabia Honey Market Growth DriverInstitutional Rural Support Programs Strengthen Domestic Production and Supply Confidence

The comprehensive institutional support architecture deployed by the Saudi government across rural agricultural development with specific and measurable benefits for the domestic beekeeping and honey production sector represents the primary structural driver of supply-side market development, creating a progressively more organized, better-resourced, and commercially capable domestic honey production ecosystem. This institutional investment transforms beekeeping from a traditional practice into a formally supported agricultural enterprise sector improving production consistency, enabling quality investment, and building the supply chain infrastructure that sustains domestic honey's competitive positioning against imported alternatives in Saudi retail channels.

The quantitative scale of this institutional support is documented across multiple official sources. Saudipedia confirms Saudi Arabia produces over 5,000 tons of honey annually, operates with more than two million beehives, and maintains a registered beekeeper base exceeding 20,000 reflecting the organizational scale that institutional support programs have helped build. The Saudi Reef program has empowered over 80,000 people, delivered more than SAR 3 billion in direct financial aid across its sectors, and supported the production of approximately 250 million kilograms of agricultural goods demonstrating the breadth of rural economic development investment within which honey production support is embedded. The combined effect of beekeeper registration formalization, direct financial aid delivery, and agricultural production support creates a domestic supply base that is progressively better positioned to compete on quality, consistency, and premium provenance credentials through 2032.

Saudi Arabia Honey Market ChallengeImport Dependence and Tightening Compliance Standards Intensify Operational Pressure

The Saudi Arabia honey market's substantial reliance on imported supply combined with a progressively more demanding regulatory compliance environment constitutes a critical structural challenge that simultaneously pressures domestic producer competitiveness and raises the operational investment threshold for all market participants. The scale of import volume relative to domestic production creates an intensely competitive retail price environment that constrains domestic honey producers' ability to expand market share purely through volume competition redirecting competitive strategy toward quality differentiation, provenance authentication, and premium positioning as the viable pathways to sustainable commercial growth within an import-dominated market structure.

The quantitative dimensions of this import dependence and compliance challenge are documented with precision across official data sources. World Bank WITS confirms Saudi Arabia imported 18,509,200 kg of natural honey valued at USD 68.66 million in 2024 a volume representing a substantial multiple of the Kingdom's estimated 5,000-plus ton domestic production. The compliance environment is simultaneously tightening: Saudi Arabia's WTO notification of a new mandatory honey labeling requirement in October 2025 mandates that all honey and edible apiculture products carry the phrase "Not suitable for infants below 12 months" effective 29 December 2025 raising the labeling compliance threshold for both importers and domestic brand owners across the entire category. For market participants, the combination of intense import competition and escalating compliance requirements creates a dual-pressure operating environment that demands both competitive quality investment and regulatory management capability through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Saudi Arabia Honey Market TrendRegional Variety Premiumization Elevates Saudi Honey Into a Heritage Specialty Category

The rising commercial visibility and consumer demand for regionally identified premium Saudi honey varieties represents a defining structural trend reflecting a progressive shift in market positioning from commodity honey competition toward a heritage specialty segment where floral source specificity, regional identity, and production provenance authenticity command meaningful price premiums and generate strong consumer loyalty among quality-conscious buyers. This premiumization trend moves Saudi honey beyond its historical role as a domestic sweetener staple into a specialty food category with cultural heritage depth, wellness association credibility, and tourism-linked visibility that collectively create a defensible premium competitive space that imported honey alternatives cannot authentically replicate.

The commercial evidence validating this regional variety premiumization trend is documented with specificity across official Saudi sources. SPA's documentation of Al-Baha producing over 15 distinct honey types supported by more than 3,000 beekeepers contributing approximately 1,000 tons annually and representing about 20% of the Kingdom's total output illustrates the regional identity depth and variety diversity that are driving premium positioning in the country's most recognized honey production geography. In Najran, beekeepers harvested nearly 20,000 kilograms of Sidr honey in one recent blossom season against annual production of approximately 90 tons confirming that limited-availability premium varieties with specific floral source credentials are generating both commercial scarcity value and strong regional identity resonance. The growing prominence of these named local varieties is strengthening premium consumer appeal and giving regional honey a clearer, more differentiated commercial identity through 2032.

Saudi Arabia Honey Market OpportunityBeeswax Valorization Creates a New Value-Added Revenue Pool Across the Apiculture Economy

The substantial and largely untapped beeswax production potential within Saudi Arabia's beekeeping sector creates a strategically significant commercial opportunity for producers seeking to diversify revenue streams, reduce production waste, and build higher-value rural enterprises beyond the limitations of a single-product honey-focused business model. Beeswax valorization represents a natural extension of existing beekeeping operations that requires relatively modest incremental investment while unlocking access to high-margin specialty applications across cosmetics, personal care, candle manufacturing, and pharmaceutical ingredient markets applications where refined beeswax commands substantially higher unit values than commodity honey and serves consumer categories with strong and growing demand for natural, traceable ingredient inputs.

The quantitative opportunity scale and practical development pathway for this beeswax valorization opportunity are documented with operational specificity by FAO. Saudi beekeepers currently discard an estimated 300 tonnes of beeswax per annum representing a substantial raw material waste stream whose commercial conversion into refined specialty wax products would generate meaningful incremental revenue across the Kingdom's beekeeping community. To address this opportunity, solar-powered crude beeswax extractors have been pilot tested at six demonstration sites across Asir, Al-Baha, and Al-Madinah and promoted to more than 150 beekeepers and rural families establishing proof-of-concept for scalable beeswax valorization at the production level. The refined wax produced through this process is confirmed suitable for high-value applications including creams, lotions, lip balms, soaps, and candles product categories that align naturally with the broader premium natural personal care demand trends that are reshaping consumer spending priorities across Saudi Arabia's growing and increasingly wellness-conscious urban consumer base through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Saudi Arabia Honey Market Segmentation Analysis

By Product Type

- Table Honey/Consumer Honey

- Industrial Honey/Ingredient Honey

The segment with highest market share under the Product Type is Table honey/Consumer honey, accounting for approximately 70% of the total market. This commanding position reflects the deep structural alignment between consumer honey formats and the everyday household consumption occasions including direct consumption, beverage preparation, culinary application, and Saudi Arabia's culturally significant gifting traditions that anchor the category's repeat purchase foundation. With seven-tenths of total market value concentrated within a single product type, table honey defines the commercial priorities, retail shelf allocation strategies, and brand investment frameworks of the Saudi Arabia honey industry. Its dominance confirms that honey's primary commercial relevance in the Kingdom remains rooted in accessible, quality-conscious daily consumption rather than specialty processing or industrial application contexts.

The structural leadership of table honey is further reinforced by the strong cultural and heritage associations that Saudi consumers attach to premium local honey varieties particularly those from recognized producing regions including Al-Baha and Najran, where specific floral sources, regional identity, and beekeeper reputation create authentic provenance narratives that command meaningful price premiums over imported alternatives. SPA's documentation of Al-Baha producing over 15 types of honey with more than 3,000 beekeepers contributing approximately 1,000 tons representing about 20% of the Kingdom's total output illustrates the regional identity depth that differentiates Saudi table honey within a competitive import-dominated market. This combination of everyday consumption relevance and premium heritage positioning enables table honey to simultaneously serve mass-market volume demand and premium quality-seeking consumer segments through 2032.

By Packaging Type

- Glass Jars

- Plastic Bottles/Squeeze Bottles

- Tubs

- Sachets/Single-Serve Packs

- Bulk Drums/Containers

The segment with highest market share under the Packaging Type is Glass Jars, accounting for approximately 55% of the total market. This dominant position reflects the fundamental role that visual product assessment, quality trust signaling, and premium presentation credentials play in Saudi honey purchase decision-making a consumer environment where product color, texture, crystallization pattern, and perceived purity are directly evaluated through transparent packaging before purchase commitment is made. Glass jars' commanding share confirms that Saudi honey consumers strongly prefer packaging formats that enable comprehensive product quality inspection at the point of sale a behavioral orientation that is particularly pronounced in a category where authenticity verification and premium quality assurance carry significant purchase motivation weight across both everyday and gifting consumption segments.

The structural leadership of glass jars is institutionally reinforced by official SFDA guidance that explicitly recommends storing honey in its original container specifically a glass jar or food-safe plastic container while cautioning against metal containers that raise oxidation risk. This regulatory quality endorsement creates a formal credibility framework that aligns official storage best practice with consumer packaging preference, amplifying glass jars' market authority beyond aesthetic and presentation advantages into the domain of scientifically validated product preservation. The SFDA's additional clarification that honey quality is determined through laboratory analysis rather than informal home tests further elevates the importance of certified, properly packaged products in consumer purchase decisions reinforcing glass jars' structural dominance as the packaging format most associated with quality integrity and premium product confidence through 2032.

List of Companies Covered in Saudi Arabia Honey Market

The companies listed below are highly influential in the Saudi Arabia honey market, with a significant market share and a strong impact on industry developments.

- Royal Honey

- Queen Bee Honey

- Raheeq Honey

- Balqees Honey

- Hatta Honey

- Emirates Beekeepers

- Geohoney

- Blossom Honey

- Al Dhafra Honey

Market News & Updates

- Geohoney, 2025:

Geohoney announced in January 2025 that it had launched an upgraded website alongside an expanded product lineup and new product ambitions for 2025. This is significant for the Saudi honey market because Geohoney is positioned around premium raw and monofloral honey, and the official announcement points to wider assortment expansion, stronger e-commerce access, and further innovation in high-value honey categories.

- Balqees Honey, 2026:

Balqees’ current official site in 2026 features Booster Honey sachets and newer functional fusion products such as Raw Honey & Matcha Fusion, showing ongoing innovation in single-serve and wellness-positioned honey formats. This is relevant to the Saudi honey market because it expands honey beyond classic jars into portable sachets and premium functional blends, supporting growth in wellness, gifting, and premium monofloral/fusion segments.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Saudi Arabia Honey Market Policies, Regulations, and Standards

- Saudi Arabia Honey Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Saudi Arabia Honey Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Table Honey/Consumer Honey- Market Insights and Forecast 2022-2032, USD Million

- Industrial Honey/Ingredient Honey- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Organic- Market Insights and Forecast 2022-2032, USD Million

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- By Source Type

- Monofloral- Market Insights and Forecast 2022-2032, USD Million

- Acacia Honey- Market Insights and Forecast 2022-2032, USD Million

- Clover Honey- Market Insights and Forecast 2022-2032, USD Million

- Manuka Honey- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Multifloral- Market Insights and Forecast 2022-2032, USD Million

- Monofloral- Market Insights and Forecast 2022-2032, USD Million

- By Processing Type

- Raw- Market Insights and Forecast 2022-2032, USD Million

- Filtered- Market Insights and Forecast 2022-2032, USD Million

- Pasteurized- Market Insights and Forecast 2022-2032, USD Million

- Ultra-filtered- Market Insights and Forecast 2022-2032, USD Million

- By Form

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- Creamed/Whipped- Market Insights and Forecast 2022-2032, USD Million

- Comb- Market Insights and Forecast 2022-2032, USD Million

- Crystallized/Granulated- Market Insights and Forecast 2022-2032, USD Million

- Powdered- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Food & Beverages- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceuticals- Market Insights and Forecast 2022-2032, USD Million

- Nutraceuticals/Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Personal Care & Cosmetics- Market Insights and Forecast 2022-2032, USD Million

- Foodservice- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets/Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Stores- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies/Health Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Direct-to-Consumer- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- Glass Jars- Market Insights and Forecast 2022-2032, USD Million

- Plastic Bottles/Squeeze Bottles- Market Insights and Forecast 2022-2032, USD Million

- Tubs- Market Insights and Forecast 2022-2032, USD Million

- Sachets/Single-Serve Packs- Market Insights and Forecast 2022-2032, USD Million

- Bulk Drums/Containers- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Household Consumers- Market Insights and Forecast 2022-2032, USD Million

- Food Manufacturers- Market Insights and Forecast 2022-2032, USD Million

- Beverage Manufacturers- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceutical Companies- Market Insights and Forecast 2022-2032, USD Million

- Cosmetic & Personal Care Companies- Market Insights and Forecast 2022-2032, USD Million

- Foodservice Operators- Market Insights and Forecast 2022-2032, USD Million

- By Region

- East

- West

- South

- Central

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- Saudi Arabia Table Honey/Consumer Honey Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Source Type- Market Insights and Forecast 2022-2032, USD Million

- By Processing Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Saudi Arabia Industrial Honey/Ingredient Honey Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Source Type- Market Insights and Forecast 2022-2032, USD Million

- By Processing Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Balqees Honey

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hatta Honey

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Emirates Beekeepers

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Geohoney

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Blossom Honey

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Royal Honey

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Queen Bee Honey

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Raheeq Honey

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Dhafra Honey

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Balqees Honey

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Nature |

|

| By Source Type |

|

| By Processing Type |

|

| By Form |

|

| By Application |

|

| By Distribution Channel |

|

| By Packaging Type |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.