New Zealand Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

New Zealand Juice Market Statistics and Insights, 2026

- Market Size Statistics

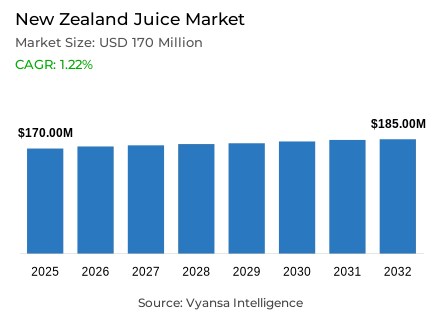

- Juice market size in New Zealand was estimated at USD 170 million in 2025.

- The market size is expected to grow to USD 185 million by 2032.

- Market to register a CAGR of around 1.22% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 60%.

- Competition

- More than 15 companies are actively engaged in producing juice in New Zealand.

- Top 5 companies acquired around 80% of the market share.

- Oriental Merchant (NZ) Ltd, Tokyo Food Co Ltd, Nekta Nutrition Ltd, Frucor Suntory New Zealand Ltd, Coca-Cola Amatil (NZ) Ltd etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 80% of the market.

New Zealand Juice Market Outlook

The New Zealand juice market is now shifting with end user abandoning the traditional breakfast habits in favor of all day, health conscious refreshment. The market is estimated to reach USD 170 million in 2025 and is expected to increase to USD 185 million in 2032 with a CAGR of about 1.22% over the forecast period. Although health issues related to sugar content, which are emphasized by the Health Star Rating system, are a challenge, the innovations in low-sugar, functional, and sparkling juice forms, which are in line with the modern lifestyle, are supporting the growth.

The category is being redefined by a significant move towards premiumisation and natural processing. Despite 100% Juice dominating the market at 60% market share, there is an increasing trend in not-from-concentrate and cold-pressed juices, including Homegrown Juice Co, which focus on authenticity and freshness. Also, coconut water is a high-potential niche, which is being positioned as a natural electrolyte drink to use daily as a wellness beverage. On the other hand, cheaper juice beverages are still strong in the face of price-sensitive end user who want to have a casual drink at a cheaper rate.

Frucor Suntory dominates the competitive environment with half of the market share due to its strong portfolio that incorporates brands such as Just Juice and McCoy. The company will also be able to consolidate its presence with the help of the Suntory Oceania platform, which will combine its non-alcoholic line with the larger sales scale beginning in 2026. Meanwhile, major retailer-owned private labels are also on the rise, with Woolworths launching low-end alternatives to trending items, like coconut water and high-end nectars, to address the current cost-of-living crises.

The sales is still focused on the retail setting, with off-trade channels taking 80% of the market. The industry is dominated by supermarkets, which use loyalty programmes and online platforms to make juice a part of the weekly shopping of groceries. In the meantime, the most active channel is retail e-commerce, which is fuelled by the digital capabilities of personalised promotions and buy again notifications. The convenience is also growing with forecourt retailers such as Z Energy, where the development of EV charging infrastructure is opening new impulse-buying opportunities in chilled, on-the-go juice formats.

New Zealand Juice Market Growth DriverWellness-Driven Consumption Sustaining Juice Relevance Beyond Traditional Breakfast Occasions

New Zealand end user New Zealand are increasingly relating their daily beverage decisions to long-term health consequences, and are continuing to show a greater interest in juice that seems cleaner and has less sugar in it. According to the Ministry of Health, one out of three adults, or 34.2%, is considered obese in 2024/25, which supports the emphasis on sugar and calorie minimization across the packaged beverage categories.

At the same time, in 2024/25, the proportion of adults who adhere to vegetable intake recommendations is 6.8%, which indicates a larger nutrition gap that can be addressed by fruit and vegetable-based beverages with a better-for-you positioning signal. This trend is prompting suppliers to update juice products with lower sugar content, organic assertions, and functional components, and to provide smaller, portable pack sizes that fit snacking and on-the-go consumption habits.

New Zealand Juice Market ChallengeCost-of-Living Pressures Constraining Premium Juice Uptake

Despite the end user preference of healthier beverage choices, the limited household budget restricts the purchasing power. The 2024/25 New Zealand Health Survey showed that 21.4% of children live in households where food supplies are limited often or occasionally, which proves that affordability is a significant pressure point. Cost barriers also appear in health access patterns, with 14.9% of adults saying that they had not seen a general practitioner in the 12 months before the 2024/25 survey because of cost factors.

This wider cost-of-living pressure forces certain end user to switch down to less expensive juice beverages and own-label multipacks at the expense of high-end chilled juices, making it harder to justify higher prices and at the same time making low sugar reformulation.

Unlock Market Intelligence

Explore the market potential with our data-driven report

New Zealand Juice Market TrendHealth Star Rating Visibility Accelerating Reformulation and Portion Control Strategies

The front-of-pack nutrition labels are becoming more influential in the way shoppers compare juice to other drinks, forcing brands to focus on reduced sugar content and more obvious wellness indicators. According to New Zealand Food Safety, 83% of shoppers use Health Star Ratings at least partially when buying a food product the first time, which makes label performance more commercially important.

Nevertheless, there is a low product coverage. According to the Health Star Rating system, the label is present on 33% of the target packaged products in New Zealand as of November 2024. This discontinuity pushes an apparent transformation to portion-controlled pack formats, lower sugar recipes, and functional ingredients that allow juice to compete with low or zero sugar substitutes at the retail shelf.

New Zealand Juice Market OpportunityExpanding Mobility and Forecourt Retail Unlocking Single-Serve Juice Growth

The convenience-based buying is on the increase and mobility sites are providing new avenues of impulse buying of beverages that fit in smaller juice packs. EECA reports that 341 high-speed public DC charge points are eligible to be co-funded by the government in 168 charging units, which adds about 25% to the fast charging capacity. This infrastructure deployment also injects money into retail sites, and EECA reports that there is co-funding of up to 15 million dollars, which opens the door to nearly 37 million dollars of private investment.

The long stay at charging and forecourt locations promotes chilled ready-to-drink juice, sparkling fruit drinks, and coconut water placed around natural hydration, added electrolytes, and portion control to travel and post-activity refreshment and convenient lunchbox supplements.

Unlock Market Intelligence

Explore the market potential with our data-driven report

New Zealand Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the New Zealand juice market, where 100% Juice grabbed a market share of 60%. This leadership is sustained by the deep-rooted end user association of 100% fruit content with quality and nutrition. However, the segment is diversifying to maintain its relevance; while reconstituted juices remain the volume driver due to their affordability, there is a growing appetite for premium "not-from-concentrate" variants. These minimally processed options attract health-conscious shoppers who prioritize ingredient integrity and fresher taste profiles.

To address concerns over natural sugar, manufacturers are innovating with reduced-sugar blends and portion-controlled packaging. Local players are also leveraging high-pressure processing (HPP) technology to preserve the nutritional quality of 100% juice without using heat. As the forecast period progresses, the 100% juice segment is expected to remain the core of the market, increasingly defined by these high-value, functional, and "clean-label" innovations that justify premium price points.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 80% of the market. Supermarkets are the primary engine of this channel, benefiting from the country's stable grocery duopoly and their ability to offer a massive variety of brands, from mass-market favorites to premium niches. By integrating juice into weekly digital shops and offering aggressive loyalty-linked discounts, supermarkets have successfully defended their dominant position against rising cost-of-living pressures and a shifting beverage landscape.

Beyond traditional grocery stores, convenience and digital channels are growing rapidly. Retail e-commerce is the most dynamic sub-channel, as major operators use personalized apps to turn juice into an easy "add-on" purchase. Additionally, forecourt retailers are capturing on-the-go occasions by tailoring their offerings to busy commuters and those using EV charging stations. This robust off-trade presence ensures that whether end user are stocking up at home or looking for a quick refreshment, juice remains highly accessible across New Zealand through 2032.

List of Companies Covered in New Zealand Juice Market

The companies listed below are highly influential in the New Zealand juice market, with a significant market share and a strong impact on industry developments.

- Oriental Merchant (NZ) Ltd

- Tokyo Food Co Ltd

- Nekta Nutrition Ltd

- Frucor Suntory New Zealand Ltd

- Coca-Cola Amatil (NZ) Ltd

- Homegrown Juice Co Ltd

- Campbell Australasia Pty Ltd

- The Better Drinks Co Ltd

- Ocean Spray Cranberries Inc

- Woolworths (New Zealand) Ltd

Competitive Landscape

New Zealand’s juice market in 2025 is led by Frucor Suntory, holding around 50% share through a diversified portfolio spanning Just Juice, Fresh Up, and sparkling extensions, supported by strong local manufacturing and distribution scale. Coca-Cola Amatil’s Keri brand remains a close competitor, increasingly active in premium and sparkling formats. Private label players, particularly Woolworths, are gaining traction amid cost-of-living pressures, offering affordable multipacks and expanding into coconut water. Emerging niche brands such as Homegrown Juice Co differentiate through not-from-concentrate positioning and high-pressure processing. Indirect competition from functional waters, sports drinks, and zero-sugar RTDs constrains growth. Key differentiation opportunities lie in reduced-sugar innovation, functional fortification, sparkling and on-the-go formats, premium clean-label positioning, and deeper omnichannel integration across supermarket and digital platforms.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- New Zealand Juice Market Policies, Regulations, and Standards

- New Zealand Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- New Zealand Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-20

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- New Zealand Juice Market Policies, Regulations, and Standards

- New Zealand Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- New Zealand Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- New Zealand 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- New Zealand Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- New Zealand Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- New Zealand Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- New Zealand Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Frucor Suntory New Zealand Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coca-Cola Amatil (NZ) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Homegrown Juice Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Campbell Australasia Pty Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The Better Drinks Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Oriental Merchant (NZ) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tokyo Food Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nekta Nutrition Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ocean Spray Cranberries Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Woolworths (New Zealand) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Frucor Suntory New Zealand Ltd

- Company Profiles

- Disclaimer

- Market Segmentation

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Category

- Market Size & Growth Outlook

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.