Global Dry Pet Food Market Report: Trends, Growth and Forecast (2026-2032)

By Animal Type (Dog, Cat, Others), By Product Type (Extruded Kibble, Freeze-Dried, Others), By Ingredients Type (PROTEIN, Grain Based, Natural, Others), By Sales Channel (Retail Offline, Retail Online), By End-User Type (Household Owners, Commercial Breeders, Veterinary Clinics, Others), By Serving Type (Single-Serve Packaging, Multi-Serve Packaging, Others), By Region Type (North America, South America, Europe, Middle East & Africa, Asia-Pacific) ... Read more

|

Major Players

|

Global Dry Pet Food Market Statistics and Insights, 2026

- Market Size Statistics

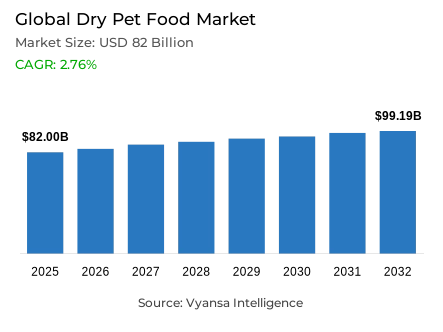

- Dry pet food market size in Global was valued at USD 82 billion in 2025 and is estimated at USD 84.12 billion in 2026.

- The market size is expected to grow to USD 99.19 billion by 2032.

- Market to register a CAGR of around 2.76% during 2026-32.

- Animal Type Shares

- Dog grabbed market share of 55%.

- Competition

- More than 20 companies are actively engaged in producing dry pet food.

- Top 5 companies acquired around 30% of the market share.

- Diamond Pet Foods , United Petfood, Champion Petfoods, Mars Petcare Inc., Nestlé Purina PetCare etc., are few of the top companies.

- Product Type

- Extruded kibble grabbed 75% of the market.

- Region

- North America leads with a 40% share of the global market.

Global Dry Pet Food Market Outlook

The Global dry pet food market was valued at USD 82 billion in 2025 and is projected to advance from USD 84.12 billion in 2026 to USD 99.19 billion by 2032, registering a CAGR of 2.76% across the forecast period. This measured and consumption-anchored expansion reflects a commercially resilient growth environment within the Global dry pet food market, where the structural role of dry kibble as a convenient, shelf-stable, portion-controlled, and nutritionally complete daily feeding product sustains consistent household demand across income tiers, retail formats, and pet ownership profiles. Growth is not driven by category novelty but by the deepening integration of premium dry pet food into routine pet care spending, the progressive premiumisation of formula segmentation, and the expanding adoption of e-commerce subscription models that convert repeat-purchase behaviour into recurring revenue streams for manufacturers and retailers alike.

Dog dry food commands approximately 55% of the animal type segment within the Global dry pet food market, reflecting the consistent and volume-intensive feeding demand associated with dogs whose larger average body size, greater breed variation, and higher serving requirements generate stronger pack consumption, larger purchase quantities, and more diverse life-stage formula segmentation than any other companion animal category. As per data published by Agriculture and Agri-Food Canada, dog food accounted for 66.4% of Canada's pet food sector in 2024 while dry dog food represented 71.5% of dog food sales within a total dry dog food category reaching CAD 3.2 billion, confirming that the structural dominance of dry dog food within developed market pet food consumption aligns closely with the global animal type leadership pattern reflected in the market's segment composition.

Extruded kibble anchors the product type segment with approximately 75% share, establishing the extrusion manufacturing platform as the dominant commercial format within the Global dry pet food market through its unmatched combination of large-scale production scalability, precise nutrient blending capability, long shelf-life performance, wide retail distribution compatibility, and the formula flexibility that allows manufacturers to serve puppy, adult, senior, weight-management, digestive-health, dental-care, and breed-specific nutrition requirements from a single industrial process. As per data published by Agriculture and Agri-Food Canada, premium dry dog food reached CAD 2.1 billion in Canada in 2024 against a mid-priced segment of CAD 980.7 million and an economy segment of CAD 78.6 million, confirming that extruded kibble is simultaneously the category's highest-volume and highest-value format across the full premium-to-economy pricing spectrum.

North America anchors the dry pet food market with the strongest regional demand base, supported by large-scale pet food manufacturing infrastructure, high recurring pet care expenditure, mature premium nutrition adoption, advanced e-commerce retail penetration, and substantial cross-border trade flows that collectively confirm the region's structural leadership across production, consumption, and export dimensions. As per data published by USDA FAS, U.S. dog and cat food exports reached USD 2.44 billion in 2025 with total export volume of 813,281 metric tons and Canada as the single largest destination at USD 1.19 billion, while FRED data confirms U.S. consumer units spent USD 880 on pets in 2024, establishing the financial depth and trade scale that sustain North America's position as the most commercially significant geography within the global dry pet food industry.

Global Dry Pet Food Market Growth Driver

Convenient Complete Nutrition Demand and Functional Segmentation Are Building a Structurally Durable Category Growth Base

The foundational demand driver within the Global dry pet food market is the structural role of complete and balanced pet food as a daily feeding product that pet owners depend on for consistent, convenient, portion-controllable, and nutritionally verified nutrition across every feeding occasion without requiring cold-chain handling, preparation, or supplementation. As per data published by the FDA, when a dog or cat food carries a complete and balanced nutritional adequacy statement the product is intended to be fed as the pet's sole diet and must be nutritionally balanced through meeting established nutrient profiles or passing recognised feeding trials, confirming that the regulatory credibility framework underpinning dry dog food daily feeding adoption is both institutionally established and consumer-facing in ways that sustain purchase confidence across premium, mid-range, and value-oriented kibble buyers.

Ingredient scrutiny, label compliance complexity, and competition from alternative fresh, wet, and raw-positioned formats are simultaneously creating the most commercially demanding challenge within the premium dry pet food market, while the accelerating shift toward functional dry pet food life-stage segmentation and e-commerce subscription replenishment is simultaneously creating the strongest growth opportunity for manufacturers capable of combining transparent labelling, verified nutrition claims, and recurring digital sales models. Evidence drawn from public data released by the U.S. Census Bureau confirms that U.S. e-commerce sales reached USD 1,233.7 billion in 2025 reflecting 5.4% growth from 2024 and accounting for 16.4% of total retail sales, while Agriculture and Agri-Food Canada confirms that premium dry dog food already commands CAD 2.1 billion of Canada's CAD 3.2 billion dry dog food category, collectively establishing that the digital replenishment infrastructure and premium value base sustaining subscription-oriented dry pet food growth are both structurally mature and commercially expanding.

Global Dry Pet Food Market Challenge

Ingredient Scrutiny and Label Compliance Obligations Are Elevating Trust and Differentiation Requirements

The most commercially consequential structural challenge within the Global dry pet food market is the rising consumer and regulatory scrutiny around ingredient quality, processing transparency, nutritional adequacy claims, and label accuracy that is progressively raising the evidentiary standard dry pet food brands must meet to retain premium buyer confidence in a competitive landscape where fresh, wet, freeze-dried, and raw-positioned alternatives actively market processing minimisation and ingredient naturalness as differentiating advantages. Based on data from the FDA, pet food must be safe to eat, produced under sanitary conditions, contain no harmful substances, and be truthfully labelled, while animal food ingredient labels must list all components by common or usual name in descending order of predominance by weight, confirming that the labelling discipline required for premium dog kibble and cat kibble positioning extends from physical packaging into digital product pages, subscription portals, marketplace listings, and promotional materials where regulatory boundaries around health claims and ingredient communication apply equally.

Cost pressures compound this compliance challenge by creating a structural tension between ingredient quality investment and retail price competitiveness that is most acute in the premium segment where buyer expectations are highest. As indicated by authoritative sources at Agriculture and Agri-Food Canada, Canada's dry dog food market encompasses a CAD 2.1 billion premium segment alongside CAD 980.7 million in mid-priced products and CAD 78.6 million in economy formats, confirming that the premium tier dominates value but also carries the highest expectation burden around claims substantiation, ingredient sourcing transparency, digestibility evidence, and veterinary nutrition credibility that manufacturers must continuously invest in to prevent premium share erosion toward fresh-format or subscription-meal competitors.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Dry Pet Food Market Trend

Functional Life-Stage Kibble and E-Commerce Subscription Models Are Reshaping Category Value Creation

A well-defined and commercially consequential structural trend is reshaping product strategy and revenue model priorities across the Global dry pet food market, as manufacturers progressively transform extruded kibble from a generic daily staple into a differentiated wellness platform by developing formulas for puppies, adult dogs, senior pets, weight management, digestive health, dental support, skin and coat improvement, breed-specific nutrition, and sensitive-stomach feeding that collectively make functional pet nutrition claims the primary basis of premium product differentiation. As per data published by Agriculture and Agri-Food Canada, adult dry dog food was purchased most often within its category at 26.7% in 2024, followed by senior dry at 20.8% and puppy dry at 12.3%, confirming that life-stage segmentation is already commercially embedded in developed market buying behaviour and that each formula category addresses meaningfully distinct nutritional requirements that justify separate product development investment and distinct pricing positioning.

The e-commerce subscription opportunity is simultaneously creating a separately significant commercial growth dimension for the Global dry pet food market that extends beyond life-stage formula differentiation into customer retention, lifetime value maximisation, and personalised feeding service delivery. Validated reports from Agriculture and Agri-Food Canada confirm that premium dry dog food commands CAD 2.1 billion within Canada's total dry dog food category, while U.S. Census Bureau data confirms e-commerce reaching 16.4% of total U.S. retail sales in 2025, collectively establishing that the high-value premium formula base and the mature digital retail infrastructure needed to support profitable subscription pet food delivery and auto-replenishment models for large-format dog kibble are both commercially present and structurally growing across the North American market that anchors global dry pet food demand.

Global Dry Pet Food Market Opportunity

E-Commerce Subscriptions Unlock Recurring Revenue

E-commerce subscriptions create a strong opportunity because dry pet food is a daily-use, repeat-purchase product with predictable replenishment cycles. Consumers buy kibble regularly based on pet size, feeding frequency, pack weight, and number of pets at home, making auto-refill models highly suitable for this category. According to the U.S. Census Bureau, total U.S. e-commerce sales reached USD 1,233.7 billion in 2025, rising 5.4% from 2024, while e-commerce accounted for 16.4% of total retail sales. This digital retail expansion supports online dry pet food sales through marketplace subscriptions, brand-owned websites, personalized feeding plans, and scheduled bulk-pack deliveries.

This opportunity is especially strong because dry pet food does not require cold-chain logistics and can be shipped through standard retail fulfillment networks. Brands can improve retention through scheduled deliveries, breed-size formulas, puppy-to-senior life-stage plans, digestive-care kibble, dental-care formulas, and personalized pack recommendations. FDA labeling guidance also supports digital product education, as animal food labels should describe the product and include details needed for safe and effective use. This allows online platforms to clearly present ingredient lists, feeding directions, nutritional claims, and formula suitability, helping dry pet food brands build trust while increasing repeat revenue.

Global Dry Pet Food Market Regional Analysis

By Region Type

- North America

- South America

- Europe

- Middle East & Africa

- Asia-Pacific

North America commands the most commercially influential position within the Global dry pet food market with around 40%, underpinned by a structural convergence of high recurring pet care expenditure, mature premium dry dog food adoption, large-scale pet food manufacturing and export infrastructure, advanced e-commerce and subscription retail penetration, and a regulatory framework that institutionalises label transparency and nutritional adequacy validation in ways that sustain consumer confidence across premium and mass-market kibble categories. As per data published by Agriculture and Agri-Food Canada, Canada's pet food retail sales totalled CAD 6.7 billion in 2024 with dog and cat food representing 98.2% of that total, while dry dog food accounted for 71.5% of Canadian dog food sales and premium dry dog food alone reached CAD 2.1 billion, confirming that the North American market's structural alignment with the Global dry pet food market's two dominant segments, Dog at 55% and Extruded Kibble at 75%, reflects a genuine and commercially deep consumption pattern rather than simply a regional size advantage.

The region's trade infrastructure and household spending data further confirm North America's structural market leadership beyond domestic consumption boundaries. Validated reports from USDA FAS confirm that U.S. dog and cat food exports reached USD 2.44 billion in 2025 with Canada receiving USD 1.19 billion and Mexico USD 260.62 million, while FRED data confirms U.S. consumer units maintained USD 880 in pet spending in 2024 and U.S. Census Bureau data establishes e-commerce at 16.4% of total retail sales in 2025, collectively confirming that North America's leadership within the North America dry pet food market is sustained simultaneously by large domestic premium consumption, subscription-oriented digital retail infrastructure, and export-scale manufacturing capability that positions the region as both the primary value creation centre and the most commercially influential demand benchmark for the global dry pet food industry.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Dry Pet Food Market Segmentation Analysis

By Animal Type

- Dog

- Cat

- Others

Dog commands the highest share within the animal type category at approximately 55%, reflecting the consistent and volume-intensive feeding demand within the Global dry pet food market generated by dogs whose larger average body size, broader breed diversity, and higher daily serving requirements create stronger pack consumption, larger purchase frequencies, and more extensive life-stage formula segmentation than any other companion animal category. Manufacturers consistently prioritise dog-focused dry food innovation because the segment supports economy, mid-priced, premium, breed-specific, functional, and veterinary nutrition formula ranges simultaneously, allowing manufacturers to serve both value-seeking bulk buyers and premium-oriented owners seeking digestive health, dental care, weight management, joint support, or skin and coat benefit positioning within a single commercialised format architecture.

The segment's commercial depth within the Global dry pet food market is further reinforced by the premiumisation momentum that is continuously elevating per-unit value across the dog dry food category beyond what volume growth alone would generate. As per data published by Agriculture and Agri-Food Canada, premium dry dog food reached CAD 2.1 billion in 2024 representing the dominant value tier within a CAD 3.2 billion total dry dog food category, while adult, senior, and puppy life-stage formulas collectively represent the three most commercially active sub-segments confirming that dog dry food supports a structurally deep and continuously expandable premium segmentation landscape that sustains category value creation independently of broader pet ownership growth rates.

By Product Type

- Extruded Kibble

- Freeze-Dried

- Others

Extruded Kibble commands the highest share within the product type category at approximately 75%, establishing the extrusion manufacturing format as the overwhelmingly dominant commercial platform within the Global dry pet food market and reflecting the consistent and operationally embedded preference among manufacturers, retailers, and pet owners for kibble formats that combine production scalability, nutrient distribution precision, long shelf stability, wide distribution compatibility, and the ingredient and formula flexibility that supports complete nutrition delivery across puppy, adult, senior, weight-management, dental-care, and breed-specific product lines from a single industrial production process. Brands consistently invest in extruded kibble platforms because they enable both mass-market affordability through large-volume production economics and premium differentiation through high-protein recipes, digestive-support additives, dental texture engineering, and functional ingredient incorporation that justify elevated price positioning without departing from the convenient daily feeding format that consumers trust.

The segment's structural dominance within the Global dry pet food market is reinforced by the regulatory credibility that supports daily feeding confidence among informed pet owners who rely on nutritional adequacy statements. Evidence drawn from public data released by the FDA confirms that complete and balanced pet food must either meet dog or cat food nutrient profiles established by AAFCO or pass feeding trials using recognised procedures to carry a nutritional adequacy statement, while USDA FAS confirms U.S. dog and cat food exports reached 813,281 metric tons in 2025, collectively establishing that extruded kibble's combination of institutionally validated nutrition standards and global logistics compatibility makes it structurally better positioned than any competing dry format to sustain both domestic premium segmentation and international trade-driven volume growth across the categories served by the Global dry pet food market.

Market Players in Global Dry Pet Food Market

These market players maintain a significant presence in the Global dry pet food market sector and contribute to its ongoing evolution.

- Diamond Pet Foods

- United Petfood

- Champion Petfoods

- Mars Petcare Inc.

- Nestlé Purina PetCare

- Hill's Pet Nutrition

- General Mills

- The J.M. Smucker Company

- WellPet LLC

- Unicharm Corp

- Tiernahrung Deuerer GmbH

- Affinity Petcare SA

- Cargill

- Blue Buffalo Pet Products, Inc

- Simmons Pet Food

Market News & Updates

- General Mills, 2026:

General Mills introduced BLUE Tastefuls Irresistible Gravy Experience in March 2026 under the Blue Buffalo brand. The product uses a 2-in-1 dry cat food recipe that turns into gravy when mixed with water. The launch expands Blue Buffalo’s dry pet food portfolio with a customized meal format for cats.

- Mars Petcare, 2025:

Mars opened a USD 450 million Royal Canin dry pet food facility in Lewisburg, Ohio, in May 2025. The site can manufacture Royal Canin’s full regional dry kibble portfolio and is the brand’s largest dry pet food factory globally. The facility adds dry pet food production capacity for North American supply

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Global Dry Pet Food Market Policies, Regulations, and Standards

- Global Dry Pet Food Pricing Analysis 2022-2032

- Global Dry Pet Food Trend (USD/ Tons) 2022-2032

- Global Dry Pet Food Pricing Trend (USD/ Tons) By Regions 2022-2032

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

- Global Feed Probiotics Pricing Trend (USD/ Tons) By Animal Type 2022-2032

- Dog

- Cat

- Others

- Global Dry Pet Food Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Global Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Animal Type

- Dog- Market Insights and Forecast 2022-2032, USD Million

- Cat- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Product Type

- Extruded Kibble- Market Insights and Forecast 2022-2032, USD Million

- Freeze-Dried- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Ingredients Type

- PROTEIN- Market Insights and Forecast 2022-2032, USD Million

- Animal Derived- Market Insights and Forecast 2022-2032, USD Million

- Plant Derived- Market Insights and Forecast 2022-2032, USD Million

- Grain Based- Market Insights and Forecast 2022-2032, USD Million

- Natural- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- PROTEIN- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Specialized Pet Shops- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets- Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Veterinary Clinics- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- E-Commerce- Market Insights and Forecast 2022-2032, USD Million

- Websites- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type

- Household Owners- Market Insights and Forecast 2022-2032, USD Million

- Commercial Breeders- Market Insights and Forecast 2022-2032, USD Million

- Veterinary Clinics- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Serving Type

- Single-Serve Packaging

- Multi-Serve Packaging

- Others

- By Region Type

- North America

- South America

- Europe

- Middle East & Africa

- Asia-Pacific

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Animal Type

- Market Size & Growth Outlook

- Single-Serve Packaging Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- The US

- Canada

- Mexico

- Rest of North America

- The US Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Multi-Serve Packaging Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Brazil

- Argentina

- Rest of South America

- Brazil Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Argentina Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Others Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- The UK

- France

- Italy

- Spain

- Rest of Europe

- Germany Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The UK Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- The UAE

- Saudi Arabia

- South Africa

- Egypt

- Rest of Middle East and Africa

- The UAE Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Saudi Arabia Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Egypt Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- By Country

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Rest of Asia Pacific

- China Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Korea Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Indonesia Dry Pet Food Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY ANIMAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- By PRODUCT TYPE - Market Insights and Forecast 2022-2032, USD Million

- BY INGREIDENTS Type- Market Insights and Forecast 2022-2032, USD Million

- BY Sales Channel Type- Market Insights and Forecast 2022-2032, USD Million

- By End-User Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Mars Petcare Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nestlé Purina PetCare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hill's Pet Nutrition

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- General Mills

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The J.M. Smucker Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Diamond Pet Foods

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- United Petfood

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Champion Petfoods

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- WellPet LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Unicharm Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tiernahrung Deuerer GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Affinity Petcare SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cargill

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Blue Buffalo Pet Products, Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Simmons Pet Food

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mars Petcare Inc.

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Animal Type |

|

| By Product Type |

|

| By Ingredients Type |

|

| By Sales Channel |

|

| By End-User Type |

|

| By Serving Type |

|

| By Region Type |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.