UAE Honey Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Table Honey/Consumer Honey, Industrial Honey/Ingredient Honey), By Nature (Organic, Conventional), By Source Type (Monofloral (Acacia Honey, Clover Honey, Manuka Honey, Others), Multifloral), By Processing Type (Raw, Filtered, Pasteurized, Ultra-filtered), By Form (Liquid, Creamed/Whipped, Comb, Crystallized/Granulated, Powdered), By Application (Food & Beverages, Pharmaceuticals, Nutraceuticals/Dietary Supplements, Personal Care & Cosmetics, Foodservice), By Distribution Channel (Retail Offline (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Pharmacies/Health Stores), Retail Online (E-commerce Platforms, Direct-to-Consumer)), By Packaging Type (Glass Jars, Plastic Bottles/Squeeze Bottles, Tubs, Sachets/Single-Serve Packs, Bulk Drums/Containers), By End User (Household Consumers, Food Manufacturers, Beverage Manufacturers, Pharmaceutical Companies, Cosmetic & Personal Care Companies, Foodservice Operators), By By Region (Dubai, Abu Dhabi, Sharjah, Northern Emirates) ... Read more

|

Major Players

|

UAE Honey Market Statistics and Insights, 2026

- Market Size Statistics

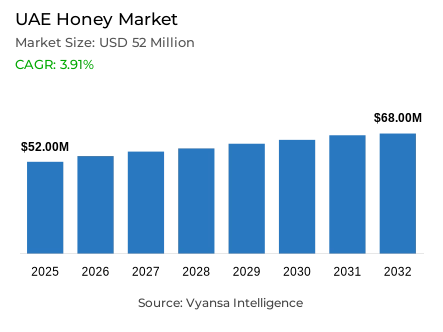

- Honey market size in UAE was valued at USD 52 million in 2025 and is estimated at USD 54 million in 2026.

- The market size is expected to grow to USD 68 million by 2032.

- Market to register a CAGR of around 3.91% during 2026-32.

- Product Type Shares

- Table honey/consumer honey grabbed market share of 65%.

- Competition

- More than 10 companies are actively engaged in producing honey in UAE.

- Top 5 companies acquired around 30% of the market share.

- Sharqawi & Partners Company, Wadi Abu Dhabi Trading Co., Abu Naif Honey, Al Shifa (Sunbulah Group), Al-Talib Trading Est. etc., are few of the top companies.

- Packaging Type

- Glass jars grabbed 55% of the market.

UAE Honey Market Outlook

The UAE honey market was valued at USD 52 million in 2025, establishing a commercially stable foundation within the country's expanding premium food and natural wellness consumption ecosystem. Projected to advance from USD 54 million in 2026 to USD 68 million by 2032, the sector registers a compound annual growth rate of 3.91% across the forecast horizon. Growth remains steady and well-supported driven by stable end user demand, wider product availability across mainstream and specialty retail channels, and rising consumer interest in packaged honey formats across both household consumption and premium gifting occasions. This measured expansion trajectory reflects a market whose commercial momentum is anchored in quality-led demand deepening rather than sharp volume acceleration.

The demand architecture sustaining this market's growth is anchored in the strength of everyday consumption categories and the enduring relevance of honey across daily household use, premium food positioning, and culturally significant gifting occasions. Table honey and consumer honey collectively command 65% of total product share the category's dominant segment confirming that regular retail demand continues to define category performance and sustain broad product visibility across the UAE's well-developed modern trade and specialty grocery channels. The Federal Competitiveness and Statistics Centre's documentation of the UAE population reaching 11.29 million in 2024, with real GDP growth at 4.0% and inflation contained at 1.66%, establishes a macroeconomic environment that supports consistent consumer purchasing power and enlarges the addressable base for packaged food products including honey.

Packaging dynamics within this market reflect the outsized role that visual quality signals and premium presentation credentials play in the UAE honey purchase decision. Glass jars command 55% of total packaging share the market's dominant format reflecting strong end user preference for transparent packaging that enables direct product quality assessment and communicates premium positioning through material quality and shelf presentation. In a consumer environment where purity perception, appearance quality, and gifting value carry meaningful purchase influence, glass jar packaging functions as a brand equity amplifier that shapes competitive positioning beyond functional containment. This packaging preference dynamic reinforces the category's premiumization trajectory and creates a structural advantage for brands that invest in premium glass packaging design and retail presentation quality.

The forward outlook through 2032 is defined by the interplay between import-dependent supply architecture, active domestic production development investment, and the progressive elevation of local-origin honey into a premium, provenance-authenticated specialty segment. The Abu Dhabi Agriculture and Food Safety Authority's development of the 11th generation of the indigenous Emirati bee strain improving adaptability and nectar-gathering efficiency under arid local conditions signals sustained institutional commitment to domestic production capability enhancement. The Ministry of Climate Change and Environment's establishment of the National Agriculture Centre in May 2025 and its June 2025 partnership with the Emirates Growth Fund create complementary policy and financial support frameworks that strengthen the broader agricultural ecosystem and provide honey producers and brands with structured pathways to invest in local sourcing, premium positioning, and export-oriented value creation through 2032.

UAE Honey Market Growth DriverMacroeconomic Stability and Population Growth Expand the Addressable Consumer Base

The UAE's combination of sustained economic growth, contained inflation, and continuous population expansion creates a structurally favorable macroeconomic demand environment for packaged food categories including honey supporting consistent consumer purchasing power across both everyday grocery and premium food consumption segments. A growing resident population with stable real income conditions enlarges the addressable buyer base for honey products and sustains regular retail purchase frequency without the demand volatility that inflationary pressure or economic uncertainty would introduce. This macroeconomic stability foundation creates a reliable commercial backdrop within which honey brands can invest in premium positioning and distribution expansion with confidence in sustained consumer purchasing capacity.

The quantitative parameters of this macroeconomic demand driver are documented with precision by the Federal Competitiveness and Statistics Centre. The UAE population reached 11.29 million in 2024, with real GDP growth standing at 4.0% and inflation remaining contained at 1.66% a combination of population scale, economic expansion, and price stability that simultaneously enlarges the addressable consumer universe and preserves the household budget capacity for premium food product investment. Complementing this macroeconomic foundation, the Ministry of Climate Change and Environment's establishment of the National Agriculture Centre in May 2025 specifically designed to support Emirati farmers, boost agricultural production, enhance product quality, and improve the competitiveness of UAE-grown food in local markets creates institutional policy support that strengthens the broader agricultural ecosystem and reinforces domestic honey production confidence through 2032.

UAE Honey Market ChallengeImport Dependence Creates Structural Supply Exposure and Pricing Vulnerability

The UAE honey market's heavy reliance on imported supply constitutes a critical structural challenge, creating persistent exposure to external pricing fluctuations, sourcing concentration risk, and supply chain disruption vulnerabilities that complicate retail pricing management and category availability consistency. In a market where product purity perception and consistent quality delivery are primary consumer trust determinants, supply chain instability whether driven by international commodity price movements, origin country production conditions, or logistics disruptions carries disproportionate commercial consequences for brands whose quality reputation is dependent on sourcing consistency they do not fully control.

The structural depth of this import dependence is quantified precisely by World Bank WITS data. The top exporters of natural honey to the UAE in 2024 are India at USD 15.51 million, Saudi Arabia at USD 6.86 million, the European Union at USD 6.43 million, New Zealand at USD 3.49 million, and Germany at USD 3.17 million a sourcing concentration pattern that reflects the UAE's near-total dependence on international supply across multiple geographic origins simultaneously. The structural dimension of this challenge is further illuminated by the Abu Dhabi Agriculture and Food Safety Authority's acknowledgment that environmental challenges continue to shape the UAE beekeeping sector requiring the development of the 11th generation indigenous Emirati bee strain to improve adaptability and nectar-gathering efficiency under local arid conditions. This domestic production constraint confirms that import dependence is not a transitional condition but a structural market characteristic that requires active supply chain risk management from all market participants through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Honey Market TrendPremium Local-Origin Positioning Elevates Emirati Honey Into a Specialty Category

The progressive elevation of locally produced Emirati honey into a premium, provenance-authenticated specialty segment represents a defining structural trend within the UAE honey market reflecting a broader consumer and institutional shift toward celebrating and commercially developing the country's indigenous agricultural heritage as a source of premium food product differentiation. This trend moves Emirati honey positioning beyond commodity competition with imported volume products into a distinct specialty category where origin authenticity, production science, beekeeping heritage, and quality certification collectively define the brand value proposition and justify premium pricing authority in both domestic retail and regional export channels.

The institutional evidence validating this trend's commercial momentum is documented across multiple official sources. The Ministry of Climate Change and Environment's Al Dhaid Agriculture Exhibition 2025 brought together over 40 agriculture and livestock companies and featured a dedicated section for Emirati beekeepers and premium-quality honey products creating a structured platform for domestic origin honey brand visibility and consumer education investment. The Abu Dhabi Agriculture and Food Safety Authority's participation in Apimondia 2025 in Copenhagen where the UAE delegation showcased Emirati honey through tasting sessions and global knowledge exchange on apiculture, product purity, and packaging innovations among participants from over 100 countries demonstrates the international positioning ambition and quality credentialing investment that are progressively building Emirati honey's global specialty category identity through 2032.

UAE Honey Market OpportunityExport and Re-Export Channels Create a Larger Commercial Growth Window

The UAE's established export and re-export trade infrastructure combined with active government investment in food sector commercial development creates a strategically compelling opportunity for UAE-based honey brands to scale their commercial reach beyond domestic shelves into regional GCC markets and broader international distribution channels. The UAE's geographic centrality as the Middle East's primary food trade hub, its world-class logistics infrastructure, and its established trading relationships across the GCC, South Asia, and East Africa create a distinctive re-export platform advantage that amplifies the commercial potential of investment in premium honey branding, local sourcing development, and value-added product innovation beyond what domestic market scale alone would justify.

The commercial evidence validating this export opportunity is documented with specificity by World Bank WITS. Top importers of natural honey from the UAE in 2024 include Saudi Arabia at USD 2.46 million, the United States at USD 517.82 thousand, Kuwait at USD 461.56 thousand, the Maldives at USD 411.41 thousand, and Bahrain at USD 234.35 thousand confirming that active export and re-export trade flows already exist across diverse and commercially significant destination markets. The Ministry of Climate Change and Environment's June 2025 partnership with the Emirates Growth Fund specifically designed to catalyze UAE-based companies in food, agriculture, and environmental resilience and unlock opportunities for businesses building a more self-sufficient national economy creates a structured financial support mechanism that enables honey SMEs to invest in branding, local sourcing authentication, premium packaging development, and value-added product formats capable of serving both domestic premium buyers and regional trade demand through 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Honey Market Segmentation Analysis

By Product Type

- Table Honey/Consumer Honey

- Industrial Honey/Ingredient Honey

The segment with highest market share under the Product Type is Table honey/Consumer honey, accounting for approximately 65% of the total market. This commanding position reflects the deep alignment between consumer honey formats and the everyday household consumption occasions including direct consumption, beverage sweetening, culinary use, and culturally embedded gifting practices that anchor the UAE honey category's repeat purchase foundation. With nearly two-thirds of total market value concentrated within a single product type, table honey defines the commercial priorities, retail shelf allocation strategies, and brand investment frameworks of the UAE honey industry. Its dominance confirms that honey's primary commercial relevance in the UAE remains rooted in accessible, familiar, daily-use consumption rather than specialty or industrial application contexts.

The structural leadership of table honey is sustained by its exceptional product versatility the ability to address a wider range of end user preferences and consumption occasions than more specialized honey formats, enabling brands to simultaneously target everyday value-conscious buyers and premium quality-seeking shoppers within the same product category. This versatility creates a commercially broad demand base that generates consistent baseline purchase velocity alongside seasonal gifting and premium occasion amplification. As the UAE's resident population continues its growth trajectory documented at 11.29 million in 2024 by the Federal Competitiveness and Statistics Centre and consumer food quality sophistication deepens, table honey's role as the category's primary volume contributor and retail identity anchor is expected to remain structurally intact through 2032.

By Packaging Type

- Glass Jars

- Plastic Bottles/Squeeze Bottles

- Tubs

- Sachets/Single-Serve Packs

- Bulk Drums/Containers

The segment with highest market share under the Packaging Type is Glass Jars, accounting for approximately 55% of the total market. This dominant position reflects the fundamental role that visual product assessment and premium presentation credentials play in UAE honey purchase decision-making a consumer environment where product appearance, perceived purity, and packaging quality function as primary quality proxies that directly influence brand selection and purchase conversion at the retail shelf. Glass jars' commanding share confirms that UAE honey consumers strongly prefer transparent packaging formats that enable direct color, texture, and clarity inspection quality evaluation behaviors that are particularly pronounced in a category where product authenticity and natural purity carry significant purchase motivation weight across both everyday and premium consumption segments.

The structural leadership of glass jars is reinforced by their dual commercial relevance across routine household use and the UAE's culturally important premium gifting occasions contexts in which packaging presentation quality directly determines perceived product value and brand differentiation. In gifting occasions specifically, glass jar honey products command substantially stronger premium positioning and higher unit value authorization than functionally equivalent products presented in alternative packaging formats. The reusable nature of glass further amplifies consumer appeal particularly in the UAE's premium retail environment where sustainability-adjacent product attributes increasingly inform purchase preference among quality-conscious shoppers. Glass jars' association with product integrity, natural authenticity, and premium shelf presence is expected to sustain and strengthen their packaging format leadership through 2032.

List of Companies Covered in UAE Honey Market

The companies listed below are highly influential in the UAE honey market, with a significant market share and a strong impact on industry developments.

- Sharqawi & Partners Company

- Wadi Abu Dhabi Trading Co.

- Abu Naif Honey

- Al Shifa (Sunbulah Group)

- Al-Talib Trading Est.

- Mabrooka Group LLC

- National Honey Company Ltd.

- Riyadh Beekeeping Co.

- Wadi Al-Nahl

- Al-Hawaj

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- UAE Honey Market Policies, Regulations, and Standards

- UAE Honey Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- UAE Honey Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Table Honey/Consumer Honey- Market Insights and Forecast 2022-2032, USD Million

- Industrial Honey/Ingredient Honey- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Organic- Market Insights and Forecast 2022-2032, USD Million

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- By Source Type

- Monofloral- Market Insights and Forecast 2022-2032, USD Million

- Acacia Honey- Market Insights and Forecast 2022-2032, USD Million

- Clover Honey- Market Insights and Forecast 2022-2032, USD Million

- Manuka Honey- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Multifloral- Market Insights and Forecast 2022-2032, USD Million

- Monofloral- Market Insights and Forecast 2022-2032, USD Million

- By Processing Type

- Raw- Market Insights and Forecast 2022-2032, USD Million

- Filtered- Market Insights and Forecast 2022-2032, USD Million

- Pasteurized- Market Insights and Forecast 2022-2032, USD Million

- Ultra-filtered- Market Insights and Forecast 2022-2032, USD Million

- By Form

- Liquid- Market Insights and Forecast 2022-2032, USD Million

- Creamed/Whipped- Market Insights and Forecast 2022-2032, USD Million

- Comb- Market Insights and Forecast 2022-2032, USD Million

- Crystallized/Granulated- Market Insights and Forecast 2022-2032, USD Million

- Powdered- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Food & Beverages- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceuticals- Market Insights and Forecast 2022-2032, USD Million

- Nutraceuticals/Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Personal Care & Cosmetics- Market Insights and Forecast 2022-2032, USD Million

- Foodservice- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Supermarkets/Hypermarkets- Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Specialty Stores- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies/Health Stores- Market Insights and Forecast 2022-2032, USD Million

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- E-commerce Platforms- Market Insights and Forecast 2022-2032, USD Million

- Direct-to-Consumer- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- Glass Jars- Market Insights and Forecast 2022-2032, USD Million

- Plastic Bottles/Squeeze Bottles- Market Insights and Forecast 2022-2032, USD Million

- Tubs- Market Insights and Forecast 2022-2032, USD Million

- Sachets/Single-Serve Packs- Market Insights and Forecast 2022-2032, USD Million

- Bulk Drums/Containers- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Household Consumers- Market Insights and Forecast 2022-2032, USD Million

- Food Manufacturers- Market Insights and Forecast 2022-2032, USD Million

- Beverage Manufacturers- Market Insights and Forecast 2022-2032, USD Million

- Pharmaceutical Companies- Market Insights and Forecast 2022-2032, USD Million

- Cosmetic & Personal Care Companies- Market Insights and Forecast 2022-2032, USD Million

- Foodservice Operators- Market Insights and Forecast 2022-2032, USD Million

- By Region

- Dubai

- Abu Dhabi

- Sharjah

- Northern Emirates

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- UAE Table Honey/Consumer Honey Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Source Type- Market Insights and Forecast 2022-2032, USD Million

- By Processing Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Industrial Honey/Ingredient Honey Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Source Type- Market Insights and Forecast 2022-2032, USD Million

- By Processing Type- Market Insights and Forecast 2022-2032, USD Million

- By Form- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Distribution Channel- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Al Shifa (Sunbulah Group)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al-Talib Trading Est.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mabrooka Group LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- National Honey Company Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Riyadh Beekeeping Co.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sharqawi & Partners Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Wadi Abu Dhabi Trading Co.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Abu Naif Honey

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Wadi Al-Nahl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al-Hawaj

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Shifa (Sunbulah Group)

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Nature |

|

| By Source Type |

|

| By Processing Type |

|

| By Form |

|

| By Application |

|

| By Distribution Channel |

|

| By Packaging Type |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.