Global Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade), By Region (North America, South America, Europe, Middle East & Africa, Asia Pacific) ... Read more

|

Major Players

|

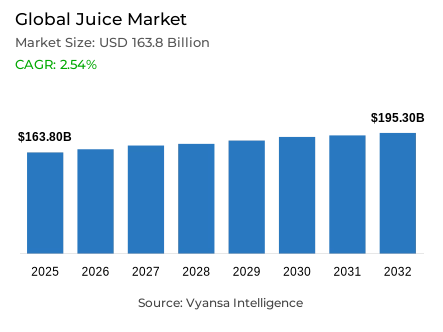

Global Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in Global was estimated at USD 163.8 billion in 2025.

- The market size is expected to grow to USD 195.3 billion by 2032.

- Market to register a CAGR of around 2.54% during 2026-32.

- Category Shares

- Juice drinks (up to 24% juice) grabbed market share of 35%.

- Competition

- More than 25 companies are actively engaged in producing juice.

- Top 5 companies acquired around 50% of the market share.

- Asahi Soft Drinks Co Ltd, Kirin Beverage Corp, Centros Comerciales Carrefour SA, Coca-Cola Co The, PepsiCo Inc etc., are few of the top companies.

- Packaging Type

- Pet bottles grabbed 45% of the market.

- Region

- Asia Pacific leads with a 40% share of the global market.

Global Juice Market Outlook

The Global juice market is going through a complicated period of regulatory stress and changing consumer preferences. The market is estimated to reach USD 163.8 billion in 2025, but is expected to reach USD 195.3 billion in 2032 with a CAGR of about 2.54% in the 2026-32 period. This is becoming more and more affected by the so-called health-value lenses, with the world taxation of sugary beverages currently in force in 114 countries, pushing consumers to choose the formulations that contain no added sugar and have clear ingredient labels.

The category is also being redefined by structural changes in dietary guidance. The 2025-2030 U.S. Dietary Guidelines now recommend restricting even 100 percent portions of juice or diluting it with water, and subject natural sugars to the same level of scrutiny as added sugars. In reaction, manufacturers are shifting to more sugar-reduction rewarding, tiered tax systems. This regulatory environment is biased towards brands that have strong reformulation abilities to retain taste and reduce the sugar concentration to lower their tax liability.

In addition to health, there is a huge economic potential in dealing with food loss in the world. Juice processing is an essential instrument to produce valorization of produce since the FAO reports that more than 25% of fruits and vegetables are wasted after harvest. Processors can minimize waste and enhance supply chain resilience by transforming surplus or cosmetically imperfect fruit into longer-life drinks. This circular economy model enables brands to reduce the cost of inputs and attract the increasing number of sustainability-conscious consumers.

The packaging environment and sales channel is still focused on accessibility and scale. PET bottles remain the market leaders, with 45% of the market share because of their lightweight, shatter-free properties and retail presence. Asia Pacific is leading regionally with a 40% share due to a huge population base and the high rate of urban lifestyle. With the market changing, localized innovation and the capacity to manoeuvre through the narrowing sugar laws will be the main factors of long-term success.

Global Juice Market Growth Driver

Policy-Driven Shift in Beverage Choices

Government intervention on sugary beverages in 2026 favors the demand of fruit-based drinks that are framed around less sugar and simple ingredients. As of July 2024, the World Health Organization lists 114 countries that impose excise taxes on sugar-sweetened carbonated drinks, showing that price-based health policies have become common in a wide range of regulatory settings. This international policy trend brings structural changes in beverage buying behaviour because consumers are more and more considering their choices in terms of health-value.

The tax toolkit is also wide: ad valorem excise taxes are applied in 50 countries and volume-based specific excises in 51 countries. This ongoing regulatory focus on sugar consumption pushes consumers to evaluate drinks based on perceived health benefit instead of taste alone, which provides a positive environment to juices with no added sugar and the ability to communicate clear ingredient labels. Policy-based demand change creates structural market benefits of naturally positioned, lower-sugar juice formulations. With tax systems becoming more geographically broad and narrower in structure, brands that can prove to be truly sugar-reduced and with clean ingredient disclosures are well-positioned to take advantage of regulatory tailwinds in the global consumer beverage preferences.

Global Juice Market Challenge

Portion and Sugar Limits Tighten Perceptions

Dietary advice in 2026 is adopting a more categorical approach to juice as a product that needs sugar control, even in 100% juice products. The U.S. Dietary Guidelines of Americans (2025-2030) recommend that 100 percent fruit or vegetable juice should be taken in small amounts or mixed with water. This governmental recommendation is indicative of the changing scientific opinion that even naturally occurring fruit sugars should be consumed in moderation, increasing the level of scrutiny of the entire juice category, and not just of added-sugar formulations.

The same recommendation puts stricter requirements on the added sugars, saying that no more than 10 gram of added sugars should be in one meal. Collectively, these messages elevate expectations of brand communication of sweetness, portioning and health value. Once the shoppers start to associate the term juice with sugar, premiumisation becomes more difficult and promotional strategies will have to operate without the use of excessively sweet taste profiles. The evolution of dietary guidelines poses structural perceptual issues to the whole juice category, forcing brands to create advanced portion messaging, clear nutrition communication, and reformulation strategies that would both respond to the added sugar issue and the natural sugar perception at the same time.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Juice Market Trend

Tax Designs Reward Sugar Reduction

Health taxes are becoming more and more design-heavy, where tax burdens are based on quantifiable beverage attributes instead of using flat rates. This change in regulatory design puts more emphasis on measurable characteristics- particularly sugar content- when governments create price signals to sugary beverages. Tiered tax architecture establishes strong financial incentives to manufacturers to focus on sugar reduction as a compliance measure and a business approach.

The World Health Organization demonstrates that 66% of the countries impose uniform excise taxes and 34% impose tiered systems (21% non-sugar-based levels and 13% sugar-based levels) on sugar-sweetened carbonated drinks. Also, 25% of the excise taxes of countries consider sugar content (28 of 114 countries). Consequently, sugar measurement, reformulation, and portion discipline become functional requirements in most markets, which directly affect pricing strategies. Tiered tax trend is an essential change in the design of fiscal policy, where brands are rewarded based on quantifiable nutritional change, instead of taxing categories equally. This generates long-term competitive advantages to manufacturers that have strong reformulation capabilities, accurate sugar monitoring, and responsive product development processes.

Global Juice Market Opportunity

Valorizing Produce to Cut Food Loss

Food loss is a structural gap that can be addressed by juice processing in 2026. In 2023, the Food and Agriculture Organization estimates that 13.3% of food is lost at post-harvest, transport, storage, wholesale, and processing stages worldwide, with fruits and vegetables contributing the largest share of 25.4% in 2023. This massive agricultural waste provides strong economic and sustainability arguments to transform perishable produce into longer-life juice products using effective processing facilities.

This rate of loss provides significant potential of value-added transformation of perishable produce into longer life beverages. By directing excess, cosmetically blemished, or time-sensitive fruits into juicing processes, processors can alleviate the pressure of spoilage without altering the occasions of consumption. The same channel facilitates investment in aggregation, sorting and high speed processing infrastructure- directly where the losses are being incurred and enhancing the reliability of supply. Produce valorisation opportunity allows manufacturers to meet sustainability requirements, lower input costs by using surplus fruit, and create resilience in the supply chain at the same time. Brands that can show genuine contributions to the circular economy by reducing waste and valorising agriculture can distinguish themselves with sustainability credentials and enhance the economic performance of operations in the global juice production environment.

Global Juice Market Regional Analysis

By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

Asia Pacific dominates the world juice market with a market share of 40%, which indicates a high level of production and consumption of fruit-based drinks. The high population base and fast urban lifestyles in the region support high demand of convenient, ready-to-drink products in the demographic segments. The variety of locally produced fruits contributes to the variety of flavour profiles and seasonal marketing opportunities, which contribute to keeping the category fresh and consumer interest in the product through localised product development.

The modern retail infrastructure and the development of cold-chain capacity increases the availability of branded juice beyond the large urban centres, allowing both branded and own-label products to reach a wider range of household segments. Increased health awareness promotes more explicit nutrition labeling and more emphasis on fruit content and reduced-sugar positioning, which influence the priorities of product development. The level of competition is also very high and the companies often win by localised flavour innovation and regular quality assurance instead of price competition. The demographic size, agricultural diversification, and modernising retail infrastructure in Asia Pacific create a sustainable market leadership that is sustained by further investment in sales channel development and health-based product innovation.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The category division with the largest share in the segment is Juice Drinks (up to 24% Juice), with a market share of 35%. This leadership is often associated with affordability and taste flexibility- these products offer familiar fruit flavours at a lower price point than 100 percent juice but still within mainstream sweetness expectations. The high accessibility to consumers and low prices make juice drinks the volume anchor in the global juice category in various market settings and income levels.

Juice drinks also give manufacturers more room to deal with variability of raw materials since formulations are not based on individual fruit inputs and can be balanced with water, flavours and fortification where legal. This generally helps in increasing the ambient shelf life and predictable production runs. Brands are thus able to retain uniform sensory profiles regardless of changes in harvest quality, which facilitates repeat buying and wide retail acceptance across a range of price points. Flexibility in formulation and predictability in manufacturing generate operational benefits that allow juice drink producers to offer competitive prices and breadth of sales channels and provide consistent quality delivery in geographically diverse markets.

By Packaging Type

- PET Bottles

- Aseptic Packages (Cartons)

- Glass Bottles

- Metal Cans

- Disposable Cups & Pouches

The segment that holds the largest portion of the packaging type division is the PET Bottles, which has a market share of 45%. PET is popular because it is lightweight, shatter-resistant, and can be easily moved in the beverage aisles of fast-moving stores, minimizing breakage and logistics. These practical handling benefits translate into substantial operational cost savings in sales channel and retail management making PET the choice of packaging format among scale oriented juice manufacturers worldwide.

In the case of juice brands, PET facilitates good shelf presence and resealability, which is convenient in both single-serving and family-use consumption situations. The format supports high-speed filling lines and a variety of shapes and label designs, allowing product differentiation without altering the formulation. With the growth of recycling infrastructure in markets, the existing collection streams of PET allow companies to make packaging decisions that are more aligned with the objectives of the circular economy. All these benefits of operational efficiency, consumer convenience, retail visibility, and enhancing sustainability credentials keep PET as the packaging of choice among manufacturers seeking volume scale and wide geographic sales channel in the competitive global juice market.

Market Players in Global Juice Market

These market players maintain a significant presence in the Global juice market sector and contribute to its ongoing evolution.

- Asahi Soft Drinks Co Ltd

- Kirin Beverage Corp

- Centros Comerciales Carrefour SA

- Coca-Cola Co The

- PepsiCo Inc

- Tesco Plc

- Keurig Dr Pepper Inc

- Kraft Heinz Co

- Orkla Foods Norge AS

- Almarai Co Ltd

- Suntory Beverage & Food Ltd

- BIM Birlesik Magazacilik AS

- Campbell's Co The

- Axfood AB

- DFI Retail Group

Market News & Updates

- Kirin Beverage Corp, 2026:

Kirin Beverage announced a new fruit-focused extension under its iMUSE (plasma lactic acid bacteria) functional drink bran “iMUSE Fruit Refresh” in two variants (Grapefruit Mix and Apple Mix) scheduled for nationwide launch in Japan on April 14, 2026, positioning the products as “drinkable refreshment” that combines fruit taste with immunity-support messaging and added nutrition cues (e.g., vitamin/iron fortification by variant), which is likely to intensify competition in the juice/fruit-drink aisle by pulling health-seeking consumers toward functional, low-juice fruit beverages and prompting rivals to answer with similar “better-for-you” fruit blends and claims-led line extensions.

- Asahi Soft Drinks Co Ltd, 2026:

Asahi Soft Drinks announced a limited-time seasonal product, “Mitsuya Sakura Lemonade,” launched nationwide in Japan starting February 17, 2026, featuring a sakura aroma with sweet-and-tart lemonade positioning and a production approach intended to enhance fruit character (with a small juice content), a strategy that typically boosts short-term category velocity through novelty and seasonality while reinforcing a “rotating flavors” playbook that can pressure mainstream juice and fruit-drink brands to refresh portfolios more frequently to defend shelf attention during key seasonal demand peaks

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Global Juice Market Policies, Regulations, and Standards

4. Global Juice Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Global Juice Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. 100% Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Reconstituted- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Juice Drinks (up to 24% juice)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Nectars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Metal Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.1. Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.2. Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.3. Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.4. Online Platforms- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Region

5.2.6.1. North America

5.2.6.2. South America

5.2.6.3. Europe

5.2.6.4. Middle East & Africa

5.2.6.5. Asia Pacific

5.2.7.By Competitors

5.2.7.1. Competition Characteristics

5.2.7.2. Market Share & Analysis

6. North America Juice Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Country

6.2.6.1. United States

6.2.6.2. Canada

6.2.6.3. Mexico

6.2.6.4. Rest of North America

6.3. United States Juice Market Statistics, 2022-2032F

6.3.1.Market Size & Growth Outlook

6.3.1.1. By Revenues in USD Million

6.3.1.2. By Quantity Sold in Million Litres

6.3.2.Market Segmentation & Growth Outlook

6.3.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

6.3.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

6.3.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.3.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.3.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.4. Canada Juice Market Statistics, 2022-2032F

6.4.1.Market Size & Growth Outlook

6.4.1.1. By Revenues in USD Million

6.4.1.2. By Quantity Sold in Million Litres

6.4.2.Market Segmentation & Growth Outlook

6.4.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

6.4.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

6.4.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.4.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.4.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.5. Mexico Juice Market Statistics, 2022-2032F

6.5.1.Market Size & Growth Outlook

6.5.1.1. By Revenues in USD Million

6.5.1.2. By Quantity Sold in Million Litres

6.5.2.Market Segmentation & Growth Outlook

6.5.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

6.5.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

6.5.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.5.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.5.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. South America Juice Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Country

7.2.6.1. Brazil

7.2.6.2. Argentina

7.2.6.3. Colombia

7.2.6.4. Chile

7.2.6.5. Peru

7.2.6.6. Rest of South America

7.3. Brazil Juice Market Statistics, 2022-2032F

7.3.1.Market Size & Growth Outlook

7.3.1.1. By Revenues in USD Million

7.3.1.2. By Quantity Sold in Million Litres

7.3.2.Market Segmentation & Growth Outlook

7.3.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

7.3.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

7.3.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.3.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.3.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.4. Argentina Juice Market Statistics, 2022-2032F

7.4.1.Market Size & Growth Outlook

7.4.1.1. By Revenues in USD Million

7.4.1.2. By Quantity Sold in Million Litres

7.4.2.Market Segmentation & Growth Outlook

7.4.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

7.4.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

7.4.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.4.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.4.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.5. Colombia Juice Market Statistics, 2022-2032F

7.5.1.Market Size & Growth Outlook

7.5.1.1. By Revenues in USD Million

7.5.1.2. By Quantity Sold in Million Litres

7.5.2.Market Segmentation & Growth Outlook

7.5.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

7.5.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

7.5.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.5.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.5.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.6. Chile Juice Market Statistics, 2022-2032F

7.6.1.Market Size & Growth Outlook

7.6.1.1. By Revenues in USD Million

7.6.1.2. By Quantity Sold in Million Litres

7.6.2.Market Segmentation & Growth Outlook

7.6.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

7.6.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

7.6.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.6.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.6.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.7. Peru Juice Market Statistics, 2022-2032F

7.7.1.Market Size & Growth Outlook

7.7.1.1. By Revenues in USD Million

7.7.1.2. By Quantity Sold in Million Litres

7.7.2.Market Segmentation & Growth Outlook

7.7.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

7.7.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

7.7.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.7.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.7.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Europe Juice Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Country

8.2.6.1. Germany

8.2.6.2. United Kingdom

8.2.6.3. Italy

8.2.6.4. France

8.2.6.5. Spain

8.2.6.6. Netherlands

8.2.6.7. Poland

8.2.6.8. Belgium

8.2.6.9. Sweden

8.2.6.10. Rest of Europe

8.3. Germany Juice Market Statistics, 2022-2032F

8.3.1.Market Size & Growth Outlook

8.3.1.1. By Revenues in USD Million

8.3.1.2. By Quantity Sold in Million Litres

8.3.2.Market Segmentation & Growth Outlook

8.3.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

8.3.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

8.3.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.3.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.3.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.4. United Kingdom Juice Market Statistics, 2022-2032F

8.4.1.Market Size & Growth Outlook

8.4.1.1. By Revenues in USD Million

8.4.1.2. By Quantity Sold in Million Litres

8.4.2.Market Segmentation & Growth Outlook

8.4.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

8.4.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

8.4.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.4.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.4.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.5. Italy Juice Market Statistics, 2022-2032F

8.5.1.Market Size & Growth Outlook

8.5.1.1. By Revenues in USD Million

8.5.1.2. By Quantity Sold in Million Litres

8.5.2.Market Segmentation & Growth Outlook

8.5.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

8.5.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

8.5.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.5.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.5.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.6. France Juice Market Statistics, 2022-2032F

8.6.1.Market Size & Growth Outlook

8.6.1.1. By Revenues in USD Million

8.6.1.2. By Quantity Sold in Million Litres

8.6.2.Market Segmentation & Growth Outlook

8.6.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

8.6.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

8.6.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.6.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.6.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.7. Spain Juice Market Statistics, 2022-2032F

8.7.1.Market Size & Growth Outlook

8.7.1.1. By Revenues in USD Million

8.7.1.2. By Quantity Sold in Million Litres

8.7.2.Market Segmentation & Growth Outlook

8.7.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

8.7.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

8.7.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.7.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.7.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.8. Netherlands Juice Market Statistics, 2022-2032F

8.8.1.Market Size & Growth Outlook

8.8.1.1. By Revenues in USD Million

8.8.1.2. By Quantity Sold in Million Litres

8.8.2.Market Segmentation & Growth Outlook

8.8.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

8.8.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

8.8.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.8.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.8.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.9. Poland Juice Market Statistics, 2022-2032F

8.9.1.Market Size & Growth Outlook

8.9.1.1. By Revenues in USD Million

8.9.1.2. By Quantity Sold in Million Litres

8.9.2.Market Segmentation & Growth Outlook

8.9.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

8.9.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

8.9.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.9.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.9.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.10. Belgium Juice Market Statistics, 2022-2032F

8.10.1. Market Size & Growth Outlook

8.10.1.1. By Revenues in USD Million

8.10.1.2. By Quantity Sold in Million Litres

8.10.2. Market Segmentation & Growth Outlook

8.10.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

8.10.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

8.10.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.10.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.10.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8.11. Sweden Juice Market Statistics, 2022-2032F

8.11.1. Market Size & Growth Outlook

8.11.1.1. By Revenues in USD Million

8.11.1.2. By Quantity Sold in Million Litres

8.11.2. Market Segmentation & Growth Outlook

8.11.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

8.11.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

8.11.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.11.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.11.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Middle East & Africa Juice Market Statistics, 2022-2032F

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Category- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.5.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.2.6.By Country

9.2.6.1. South Africa

9.2.6.2. Saudi Arabia

9.2.6.3. UAE

9.2.6.4. Nigeria

9.2.6.5. Egypt

9.2.6.6. Morocco

9.2.6.7. Turkey

9.2.6.8. Rest of Middle East and Africa

9.3. South Africa Juice Market Statistics, 2022-2032F

9.3.1.Market Size & Growth Outlook

9.3.1.1. By Revenues in USD Million

9.3.1.2. By Quantity Sold in Million Litres

9.3.2.Market Segmentation & Growth Outlook

9.3.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

9.3.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

9.3.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.3.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.3.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.4. Saudi Arabia Juice Market Statistics, 2022-2032F

9.4.1.Market Size & Growth Outlook

9.4.1.1. By Revenues in USD Million

9.4.1.2. By Quantity Sold in Million Litres

9.4.2.Market Segmentation & Growth Outlook

9.4.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

9.4.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

9.4.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.4.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.4.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.5. UAE Juice Market Statistics, 2022-2032F

9.5.1.Market Size & Growth Outlook

9.5.1.1. By Revenues in USD Million

9.5.1.2. By Quantity Sold in Million Litres

9.5.2.Market Segmentation & Growth Outlook

9.5.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

9.5.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

9.5.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.5.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.5.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.6. Nigeria Juice Market Statistics, 2022-2032F

9.6.1.Market Size & Growth Outlook

9.6.1.1. By Revenues in USD Million

9.6.1.2. By Quantity Sold in Million Litres

9.6.2.Market Segmentation & Growth Outlook

9.6.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

9.6.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

9.6.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.6.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.6.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.7. Egypt Juice Market Statistics, 2022-2032F

9.7.1.Market Size & Growth Outlook

9.7.1.1. By Revenues in USD Million

9.7.1.2. By Quantity Sold in Million Litres

9.7.2.Market Segmentation & Growth Outlook

9.7.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

9.7.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

9.7.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.7.2.4. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.7.2.5. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9.8. Morocco Juice Market Statistics, 2022-2032F

9.8.1.Market Size & Growth Outlook

9.8.1.1. By Revenues in USD Million

9.8.1.2. By Quantity Sold in Million Litres

9.8.2.Market Segmentation & Growth Outlook

9.8.2.1. By Category- Market Insights and Forecast 2022-2032, USD Million

9.8.2.2. By Nature- Market Insights and Forecast 2022-2032, USD Million

9.8.2.3. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.8.2.4. By Packaging Type- Market Insights and Fore

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.