Global Beverage Packaging Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Can, Bottle & Jar, Pouch, Carton, Others), By Packaging Material (Plastic, Glass, Metal, Others), By Application (Alcoholic Beverages, Bottled Water, Carbonated Soft Drinks, Juices, Dairy Beverages, Plant-Based Beverages, RTD Tea & Coffee, Energy & Sports Drinks, Functional Beverages, Others), By Region (North America, South America, Europe, Middle East & Africa, Asia Pacific) ... Read more

|

Major Players

|

Global Beverage Packaging Market Statistics and Insights, 2026

- Market Size Statistics

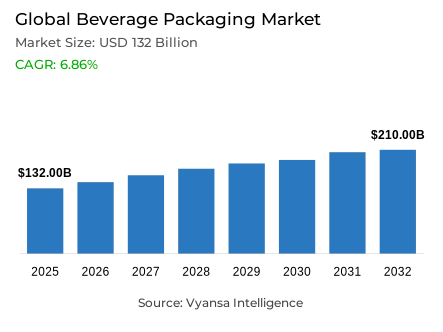

- Beverage packaging market size in Global was estimated at USD 132 billion in 2025.

- The market size is expected to grow to USD 210 billion by 2032.

- Market to register a CAGR of around 6.86% during 2026-32.

- Product Type Shares

- Bottle & jar grabbed market share of 40%.

- Competition

- Global beverage packaging market is currently being catered to by more than 25 companies.

- Top 5 companies acquired around 10% of the market share.

- Crown Holdings, Inc., Berry Global Inc., SIG Group AG, O-I Glass Inc., Tetra Pak (Tetra Laval International S.A.) etc., are few of the top companies.

- Packaging Material

- Plastic grabbed 40% of the market.

- Region

- Asia Pacific leads with a 40% share of the global market.

Global Beverage Packaging Market Outlook

The Global beverages packaging Market size was valued at USD 132 billion in 2025 and is projected to grow from USD 143 billion in 2026 to USD 210 billion by 2032, exhibiting a CAGR of 6.86% during the forecast period. Growth remains supported by structural regulatory mandates, engineering standardization, and sustained beverage production volumes across major economies, reinforcing long-term investment visibility across supply chains.

Sustainability regulation continues to act as a structural demand catalyst across beverages packaging supply chains. From 2025, PET beverage bottles placed on the EU market must contain at least 25% recycled plastic content, and by 2026 multinational brand owners are aligning global pack specifications to meet this threshold uniformly. This transition has turned recycled-content integration into a baseline procurement requirement. As a result, suppliers are scaling food-contact compliant recycling capacity, advanced contamination control, and traceability systems to secure long-term volumes.

Product design mandates are further reshaping engineering priorities, and beverages packaging formats are being standardized to avoid parallel tooling systems. Attached caps, mandatory in the EU since July 2024, are now widely adopted in 2026 to maintain consistent specifications across regions. Closure systems are being redesigned to protect torque consistency, carbonation performance, and high-speed filling compatibility. At the same time, aluminum prices rose to US$3,142 per metric ton in January 2026 compared with an average of US$2,419 in 2024, increasing cost pass-through pressure for cans and closures.

In 2025, bottles & jars captured 40% of product type share due to operational efficiency and branding flexibility, while plastic accounted for 40% of packaging material usage given its lightweight and logistics advantages. Asia Pacific led with a 40% share, supported by scale-driven beverage manufacturing and dense conversion infrastructure, reinforcing steady capacity expansion and compliance-focused investment through 2032.

Global Beverage Packaging Market Growth Driver

Regulatory-Driven Recycled Content Mandates Strengthening Compliance Investments

Sustainability regulation has become a structural driver of demand in the global beverages packaging market. The European Commission verifies that, starting from 2025, PET beverage bottles sold within the EU market are required to contain a minimum of 25% recycled plastic material under the Single-Use Plastics Directive. In 2026, global brand owners continue to harmonize global pack specifications to ensure compliance with this minimum standard, shifting the integration of recycled materials from a point of differentiation to a standard of procurement. This directly sustains a stable volume of orders for packaging meeting these specifications in high-volume beverage segments.

To comply with these regulations, converters are ramping up capacity for food-contact compliant recycling lines, advanced contamination management systems, and SKU-level traceability documentation. On the basis of observed regulatory audits and validation cycles in multinational projects in 2026, suppliers are increasingly investing in line trials, clarity management, and barrier layer validation to ensure shelf life and brand appearance.

Global Beverage Packaging Market Challenge

Raw Material Price Volatility Intensifying Margin Pressures

Instability in input costs persists as a structural operational factor in 2026. Based on the World Bank’s Commodity Markets Outlook and Pink Sheet market data (January 2026 release), aluminum prices were recorded at US$3,142 per metric ton in January 2026, up from an average of US$2,419 per metric ton in 2024. These developments have a direct impact on beverage cans, closures, and transportation costs in the Global beverages packaging market.

The norm has become frequent repricing cycles, surcharge clauses, and reduced validity periods for quotes. From an operational perspective, converters are tightening inventory buffers and selectively hedging, but this is also raising administrative complexity and working capital needs. Such variability also leads to delays in tooling investments and lightweighting initiatives, as financial planning becomes more risk-averse. In 2026, margin pressure will remain high, especially for suppliers with large SKU bases and multi-regional exposure.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Beverage Packaging Market Trend

Standardization of Connected-Closure Engineering Across Markets

Product design regulations are also influencing packaging engineering strategies. The European Commission has confirmed that caps and lids on single-use plastic beverage packaging must be kept together from 3 July 2024 onwards, making tethered closures a mandatory requirement in the EU. By 2026, global beverage companies are embracing standardized cap-on designs across regions to prevent parallel tooling requirements, solidifying a strong engineering imperative in the Global beverages packaging market.

This evolution goes beyond mere compliance and into comprehensive production optimization. Closure systems are being re-engineered to provide consistent torque, carbonation, and pouring performance while also ensuring tether robustness. With 2026 validation cycles on high-speed lines, packaging professionals are accelerating cross-functional verification work, including ergonomics, cap retention force, and line speed compatibility. This is creating a paradigm shift towards standardized attached closure types, now considered the norm rather than the exception.

Global Beverage Packaging Market Opportunity

Collection-Oriented Design Creating System-Level Value

Changing collection targets are opening up new business opportunities for packaging material suppliers. The European Commission points out that there is a 90% separate collection target for plastic beverage bottles by 2029, and this is encouraging governments and industry groups to expand deposit return schemes and tracking networks. In 2026, end-users of beverages are increasingly looking for packaging solutions that can be seamlessly recovered, and this is driving the collection-optimized packaging market in the Global beverages packaging market.

Suppliers providing system-ready packaging solutions such as wash-off labels, contamination-reducing adhesives, and improved material identification functionality gain a competitive advantage in long-term contracts. In addition to packaging, reporting capability and recyclability documentation are now included in tender assessments. Based on procurement activities in 2026, brands are now preferring suppliers who can provide support for the generation of compliance data in addition to product delivery, making the alignment of recyclability a tangible revenue stream.

Global Beverage Packaging Market Regional Analysis

By Region

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

Asia Pacific leads the Global beverages packaging market with a 40% share, supported by its extensive beverage manufacturing base and large population scale. The region hosts dense conversion ecosystems, enabling faster turnaround times and competitive production economics. In 2026, beverage end users across Asia Pacific continue expanding product portfolios to address varied price tiers and consumption occasions, reinforcing sustained packaging demand across formats and materials.

The region’s scale advantage also strengthens localization strategies. Suppliers increasingly deploy dual-plant models to mitigate logistics risk and enhance service reliability. Expanding intra-Asia trade and modernization of retail infrastructure further encourage packaging specification harmonization for both domestic distribution and exports. Through 2026, Asia-Pacific remains the primary focus for capacity additions, supplier partnerships, and operational consolidation within the Global beverages packaging market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Beverage Packaging Market Segmentation Analysis

By Product Type

- Can

- Bottle & Jar

- Pouch

- Carton

- Others

Bottles & jars currently hold the largest market share of about 40% under the product type category of the Global beverages packaging market, which is a reflection of their packaging suitability for various beverage types. This packaging type is suitable for still beverages, carbonated beverages, and functional beverages and has high flexibility for branding purposes through customized shapes and labeling options. From an operational standpoint, bottles & jars packaging are highly compatible with standardized neck finishes, closures, and filling systems, which are less likely to cause conversion difficulties for beverage end-users introducing new SKUs or expanding production.

The market dominance of this category is also attributed to its adaptability to various shelf life and distribution needs. Bottles & jars packaging are highly stackable, resistant to transportation stress, and provide excellent retail visibility. In 2026, suppliers continue to focus on this category due to the well-developed global supply chain and compatibility with high-speed production lines. Although other packaging types are still relevant in niche markets, bottles & jars are structurally superior in terms of balancing cost efficiency, operational familiarity, and marketing flexibility.

By Packaging Material

- Plastic

- Glass

- Metal

- Others

Plastic has a 40% market share under the packaging material category in the Global beverages packaging market and has retained its lead position due to its lightweight properties and efficiency. End-use consumers of beverages prefer plastic packaging due to its compatibility with high-speed filling lines, non-breakable properties, and lighter transportation weight. In the large-scale distribution channels studied in 2026, plastic packaging maintains a significant total delivered cost advantage over heavier packaging alternatives.

The market share of the segment is also sustained by its flexible design properties and adjustable barrier properties. This allows manufacturers to vary clarity, strength, and oxygen barrier properties without major line changes, thus maintaining production continuity. In addition, plastic packaging is less prone to breakage and easier to manage in logistics. Although other materials are increasingly scrutinized for sustainability concerns, plastic packaging maintains its material relevance in applications where scalability, safe handling, and efficient manufacturing processes continue to be the key drivers for beverage end-use consumers.

Market Players in Global Beverage Packaging Market

These market players maintain a significant presence in the Global beverage packaging market sector and contribute to its ongoing evolution.

- Crown Holdings, Inc.

- Berry Global Inc.

- SIG Group AG

- O-I Glass Inc.

- Tetra Pak (Tetra Laval International S.A.)

- Ball Corporation

- Ardagh Group S.A.

- Amcor plc

- Verallia SA

- Smurfit Westrock

- Mondi plc

- Sonoco Products Company

- Toyo Seikan Group Holdings Ltd.

- Silgan Holdings Inc.

- CANPACK S.A.

Market News & Updates

- Ball Corporation, 2026:

Ball’s February 3, 2026 results release showed beverage packaging demand normalization translating into stronger segment economics: its Beverage packaging, North & Central America unit delivered $772m comparable operating earnings on $6.29B sales for full-year 2025, with management explicitly attributing performance to higher volume and favorable price/mix (including contractual aluminum pass-through), underscoring how scale metal can producers can protect margins and sustain capacity utilization as brand owners keep prioritizing lightweight, high-recycling-rate beverage formats globally.

- Amcor plc, 2026:

Amcor’s FY2026 Q2 earnings release (Feb 2026) emphasized the enlarged global beverages-adjacent packaging footprint and integration economics from the Berry acquisition: for the six months ended Dec 31, 2025 it reported $11,194m net sales and reaffirmed FY2026 guidance of $4.00–$4.15 adjusted EPS while citing acquisition-driven scale and synergy delivery, a combination that materially raises competitive pressure in global beverage packaging (rigid + flexible) by expanding Amcor’s ability to bundle formats, optimize pricing across materials, and fund sustainability-led redesigns at high volume.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Global Beverages Packaging Market Policies, Regulations, and Standards

4. Global Beverages Packaging Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Global Beverages Packaging Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Can- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Bottle & Jar- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Pouch- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Carton- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Packaging Material

5.2.2.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Application

5.2.3.1. Alcoholic Beverages- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Bottled Water- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Carbonated Soft Drinks- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Juices- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Dairy Beverages- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Plant-Based Beverages- Market Insights and Forecast 2022-2032, USD Million

5.2.3.7. RTD Tea & Coffee- Market Insights and Forecast 2022-2032, USD Million

5.2.3.8. Energy & Sports Drinks- Market Insights and Forecast 2022-2032, USD Million

5.2.3.9. Functional Beverages- Market Insights and Forecast 2022-2032, USD Million

5.2.3.10. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Region

5.2.4.1. North America

5.2.4.2. South America

5.2.4.3. Europe

5.2.4.4. Middle East & Africa

5.2.4.5. Asia Pacific

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. North America Beverages Packaging Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Product Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Application- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Country

6.2.4.1. US

6.2.4.2. Canada

6.2.4.3. Mexico

6.2.4.4. Rest of North America

6.3. US Beverages Packaging Market Statistics, 2022-2032F

6.3.1.Market Size & Growth Outlook

6.3.1.1. By Revenues in USD Million

6.3.2.Market Segmentation & Growth Outlook

6.3.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

6.3.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.3.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

6.4. Canada Beverages Packaging Market Statistics, 2022-2032F

6.4.1.Market Size & Growth Outlook

6.4.1.1. By Revenues in USD Million

6.4.2.Market Segmentation & Growth Outlook

6.4.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

6.4.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.4.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

6.5. Mexico Beverages Packaging Market Statistics, 2022-2032F

6.5.1.Market Size & Growth Outlook

6.5.1.1. By Revenues in USD Million

6.5.2.Market Segmentation & Growth Outlook

6.5.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

6.5.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.5.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

7. South America Beverages Packaging Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Product Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Application- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Country

7.2.4.1. Brazil

7.2.4.2. Argentina

7.2.4.3. Rest of South America

7.3. Brazil Beverages Packaging Market Statistics, 2022-2032F

7.3.1.Market Size & Growth Outlook

7.3.1.1. By Revenues in USD Million

7.3.2.Market Segmentation & Growth Outlook

7.3.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

7.3.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.3.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

7.4. Argentina Beverages Packaging Market Statistics, 2022-2032F

7.4.1.Market Size & Growth Outlook

7.4.1.1. By Revenues in USD Million

7.4.2.Market Segmentation & Growth Outlook

7.4.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

7.4.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.4.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

8. Europe Beverages Packaging Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Product Type- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Application- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Country

8.2.4.1. Germany

8.2.4.2. UK

8.2.4.3. France

8.2.4.4. Italy

8.2.4.5. Spain

8.2.4.6. Rest of Europe

8.3. Germany Beverages Packaging Market Statistics, 2022-2032F

8.3.1.Market Size & Growth Outlook

8.3.1.1. By Revenues in USD Million

8.3.2.Market Segmentation & Growth Outlook

8.3.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

8.3.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.3.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

8.4. UK Beverages Packaging Market Statistics, 2022-2032F

8.4.1.Market Size & Growth Outlook

8.4.1.1. By Revenues in USD Million

8.4.2.Market Segmentation & Growth Outlook

8.4.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

8.4.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.4.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

8.5. France Beverages Packaging Market Statistics, 2022-2032F

8.5.1.Market Size & Growth Outlook

8.5.1.1. By Revenues in USD Million

8.5.2.Market Segmentation & Growth Outlook

8.5.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

8.5.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.5.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

8.6. Italy Beverages Packaging Market Statistics, 2022-2032F

8.6.1.Market Size & Growth Outlook

8.6.1.1. By Revenues in USD Million

8.6.2.Market Segmentation & Growth Outlook

8.6.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

8.6.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.6.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

8.7. Spain Beverages Packaging Market Statistics, 2022-2032F

8.7.1.Market Size & Growth Outlook

8.7.1.1. By Revenues in USD Million

8.7.2.Market Segmentation & Growth Outlook

8.7.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

8.7.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.7.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

9. Middle East & Africa Beverages Packaging Market Statistics, 2022-2032F

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Product Type- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Application- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Country

9.2.4.1. Saudi Arabia

9.2.4.2. UAE

9.2.4.3. South Africa

9.2.4.4. Rest of Middle East & Africa

9.3. Saudi Arabia Beverages Packaging Market Statistics, 2022-2032F

9.3.1.Market Size & Growth Outlook

9.3.1.1. By Revenues in USD Million

9.3.2.Market Segmentation & Growth Outlook

9.3.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

9.3.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.3.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

9.4. UAE Beverages Packaging Market Statistics, 2022-2032F

9.4.1.Market Size & Growth Outlook

9.4.1.1. By Revenues in USD Million

9.4.2.Market Segmentation & Growth Outlook

9.4.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

9.4.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.4.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

9.5. South Africa Beverages Packaging Market Statistics, 2022-2032F

9.5.1.Market Size & Growth Outlook

9.5.1.1. By Revenues in USD Million

9.5.2.Market Segmentation & Growth Outlook

9.5.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

9.5.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.5.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

10. Asia Pacific Beverages Packaging Market Statistics, 2022-2032F

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.2. Market Segmentation & Growth Outlook

10.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Country

10.2.4.1. China

10.2.4.2. Japan

10.2.4.3. India

10.2.4.4. South Korea

10.2.4.5. Australia

10.2.4.6. Rest of Asia Pacific

10.3. China Beverages Packaging Market Statistics, 2022-2032F

10.3.1. Market Size & Growth Outlook

10.3.1.1. By Revenues in USD Million

10.3.2. Market Segmentation & Growth Outlook

10.3.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

10.3.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.3.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

10.4. Japan Beverages Packaging Market Statistics, 2022-2032F

10.4.1. Market Size & Growth Outlook

10.4.1.1. By Revenues in USD Million

10.4.2. Market Segmentation & Growth Outlook

10.4.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

10.4.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.4.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

10.5. India Beverages Packaging Market Statistics, 2022-2032F

10.5.1. Market Size & Growth Outlook

10.5.1.1. By Revenues in USD Million

10.5.2. Market Segmentation & Growth Outlook

10.5.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

10.5.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.5.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

10.6. South Korea Beverages Packaging Market Statistics, 2022-2032F

10.6.1. Market Size & Growth Outlook

10.6.1.1. By Revenues in USD Million

10.6.2. Market Segmentation & Growth Outlook

10.6.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

10.6.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.6.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

10.7. Australia Beverages Packaging Market Statistics, 2022-2032F

10.7.1. Market Size & Growth Outlook

10.7.1.1. By Revenues in USD Million

10.7.2. Market Segmentation & Growth Outlook

10.7.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

10.7.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.7.2.3. By Application- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. O-I Glass Inc.

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Tetra Pak (Tetra Laval International S.A.)

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Ball Corporation

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Ardagh Group S.A.

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Amcor plc

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Crown Holdings, Inc.

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Berry Global Inc.

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. SIG Group AG

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Verallia SA

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. Smurfit Westrock

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

11.1.11. Mondi plc

11.1.11.1.Business Description

11.1.11.2.Product Portfolio

11.1.11.3.Collaborations & Alliances

11.1.11.4.Recent Developments

11.1.11.5.Financial Details

11.1.11.6.Others

11.1.12. Sonoco Products Company

11.1.12.1.Business Description

11.1.12.2.Product Portfolio

11.1.12.3.Collaborations & Alliances

11.1.12.4.Recent Developments

11.1.12.5.Financial Details

11.1.12.6.Others

11.1.13. Toyo Seikan Group Holdings Ltd.

11.1.13.1.Business Description

11.1.13.2.Product Portfolio

11.1.13.3.Collaborations & Alliances

11.1.13.4.Recent Developments

11.1.13.5.Financial Details

11.1.13.6.Others

11.1.14. Silgan Holdings Inc.

11.1.14.1.Business Description

11.1.14.2.Product Portfolio

11.1.14.3.Collaborations & Alliances

11.1.14.4.Recent Developments

11.1.14.5.Financial Details

11.1.14.6.Others

11.1.15. CANPACK S.A.

11.1.15.1.Business Description

11.1.15.2.Product Portfolio

11.1.15.3.Collaborations & Alliances

11.1.15.4.Recent Developments

11.1.15.5.Financial Details

11.1.15.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Packaging Material |

|

| By Application |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.