Global Dog Food Packaging Market Report: Trends, Growth and Forecast (2026-2032)

By Material Type (Plastic, Paper & Paperboard, Metal, Aluminum, Bio-Based Materials, Others), By Packaging Type (Bags & Pouches, Metal Cans, Folding Cartons, Containers & Tubs, Sachets, Stick Packs, Others), By Dog Food Type (Dry Dog Food, Wet Dog Food, Treats & Snacks, Frozen Dog Food, Functional/Premium Nutrition, Others), By Closure Type (Zipper Packaging, Vacuum Packaging, Heat-Sealed Packaging, Tear Notch, Spouted Packaging, Others), By Printing Type (Digital Printing, Flexographic Printing, Rotogravure Printing, Offset Printing, Others), By End User (Pet Food Manufacturers, Veterinary Nutrition Companies, Premium Pet Food Brands, Private Label Manufacturers, Others), By Region Type (North America, South America, Europe, Middle East & Africa, Asia-Pacific) ... Read more

|

Major Players

|

Global Dog Food Packaging Market Statistics and Insights, 2026

- Market Size Statistics

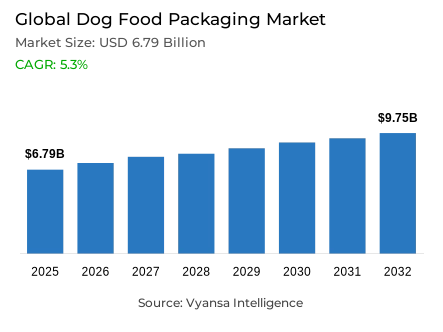

- Dog food packaging market size in Global was valued at USD 6.79 billion in 2025 and is estimated at USD 7.15 billion in 2026.

- The market size is expected to grow to USD 9.75 billion by 2032.

- Market to register a CAGR of around 5.3% during 2026-32.

- Packaging Type Shares

- Bags & pouches grabbed market share of 55%.

- Competition

- More than 30 companies are actively engaged in producing dog food packaging.

- Top 10 companies acquired the maximum share of the market.

- Constantia Flexibles, Sealed Air, ProAmpac, Amcor, Mondi Group etc., are few of the top companies.

- Material Type

- Plastic grabbed 60% of the market.

- Region

- North America leads with a 40% share of the global market.

Global Dog Food Packaging Market Outlook

The Global dog food packaging market was valued at USD 6.79 billion in 2025 and is projected to advance from USD 7.15 billion in 2026 to USD 9.75 billion by 2032, registering a CAGR of 5.3% across the forecast period. This measured and formulation-driven expansion reflects a commercially dependable growth environment within the Global dog food packaging market, where rising demand for dry dog food packaging, wet food formats, functional treats, veterinary diets, and fresh-style nutrition is collectively elevating packaging from a passive containment function toward an active system of barrier protection, regulatory communication, and brand differentiation that suppliers must engineer with increasing technical precision across moisture control, oxygen management, seal integrity, and food-contact safety simultaneously.

Bags and pouches command 55% of the packaging type segment, anchored in their structural alignment with the product diversity, size variability, and channel demands of modern dog food retail, where a single flexible packaging family must perform across 100 g treat pouches, 1 kg trial packs, 5 kg mid-range bags, and large-volume bulk formats without compromising freshness, printability, or handling durability. As per data published by the FDA, pet food must be safe, produced under sanitary conditions, contain no harmful substances, and be truthfully labeled, confirming that packaging carries both a food-protection mandate and a regulatory communication obligation that flexible formats serve more efficiently than most rigid alternatives across the full breadth of product categories active in this market.

Plastic dog food packaging holds 60% of the material type segment, sustained by the performance depth of laminated films, barrier laminates, sealant layers, and zipper-compatible structures that protect fat-rich kibble, aroma-sensitive treats, and moisture-dependent wet food products against the oxidation, moisture ingress, and grease migration that shorten shelf life and degrade palatability across long distribution chains. Regulatory pressure is simultaneously reshaping this material leadership, as Regulation EU 2025/40, which entered into force on February 11, 2025 and applies from August 12, 2026, introduces mandatory recyclability performance classes, packaging waste reduction targets, and recycled content requirements that directly challenge multi-layer flexible structures dominant across the dog food bags and pouch segment.

North America anchors the market with 40% of global demand, supported by mature pet ownership depth, premium nutrition adoption, organised specialty retail, veterinary diet distribution, and a rapidly expanding e-commerce subscription channel that collectively require packaging to perform across shelf display, clinical communication, parcel delivery, and repeated home-use scenarios simultaneously. The market's trajectory through 2032 is shaped by the progressive convergence of shelf-life protection, resealable packaging innovation, recyclable material transition, and premium positioning demands that reward suppliers capable of delivering barrier performance and circularity compliance within the same engineered structure.

Global Dog Food Packaging Market Growth Driver

Shelf-Life Protection and Premium Product Complexity Are Creating a Structurally Durable Demand Foundation

Shelf-life protection is the most commercially significant demand driver within the Global dog food packaging market, compelling suppliers to engineer increasingly sophisticated barrier systems across dry dog food bags, wet dog food packaging, treat pouches, and veterinary diet packs where fat oxidation, moisture ingress, aroma loss, and microbial exposure directly degrade nutritional quality, palatability, and brand trust across distribution timelines that can span months. As per data published by the FDA, pet food must be safe, sanitary, free from harmful substances, and carry truthful labeling covering ingredient statements, guaranteed analysis, feeding instructions, nutritional adequacy statements, and manufacturer details, confirming that packaging is simultaneously a food-protection system and a regulatory communication surface whose performance requirements intensify as product formulations become more specialised, claim-heavy, and ingredient-sensitive across the premium and functional nutrition segments driving category growth.

Premiumisation reinforces this driver by elevating both the technical and commercial expectations that packaging must meet across high-protein recipes, grain-free formulas, digestive-support diets, joint-care treats, and fresh-style meals where consumer trust is built directly through packaging clarity, freshness signals, and claim presentation. Evidence drawn from public data released by the FDA confirms that pet food labels communicate product identity, ingredient composition, nutritional adequacy, and feeding guidance that are especially critical for functional and veterinary-positioned products whose purchase decisions depend on packaging legibility and clinical credibility, creating sustained demand for high-barrier pet food packaging with premium graphics, resealable closures, and food-contact-safe structures that protect both product integrity and brand equity across the full retail and e-commerce distribution environment.

Global Dog Food Packaging Market Challenge

Multi-Layer Plastic Recyclability Gaps and Regulatory Compliance Complexity Are Creating Structural Material Pressure

The most commercially consequential structural challenge within the dog food packaging market is the technical incompatibility between the multi-layer plastic structures that currently deliver the barrier, seal, and mechanical performance that dog food packaging demands and the recyclability performance thresholds that Regulation EU 2025/40 requires from packaging placed on the European market from August 2026 onward. Based on data from the European Commission, Regulation EU 2025/40 establishes recyclability performance classes where Grade A represents at least 95% recyclability by weight, Grade B at least 80%, and Grade C at least 70%, with packaging below the 70% threshold classified as technically non-recyclable, directly challenging laminated films, metallized treat packs, and mixed-material zipper bags that combine oxygen barrier, moisture resistance, grease control, and mechanical strength through material combinations that do not separate cleanly within standard recycling streams.

Compliance cost compounds this technical challenge by raising the development, testing, and approval investment that brands must absorb before recyclable reformulations can be validated against shelf-life, seal, migration, and transport performance requirements. As indicated by authoritative sources at the U.S. EPA, plastic containers and packaging have historically achieved lower recovery rates than paper, paperboard, metal, and glass packaging across municipal solid waste systems, confirming that flexible packaging recycling challenges are systemic rather than market-specific and that suppliers redesigning mono-material pet food pouches, recyclable closure systems, and downgauged film structures for circularity compliance must simultaneously demonstrate that reformulated structures meet oxygen transmission, moisture vapor transmission, puncture strength, and food-contact safety specifications across the full range of dog food formats they are designed to protect.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Dog Food Packaging Market Trend

Resealable and Recyclable Flexible Structures Are Emerging as the Commercial Standard for Dog Food Packaging Innovation

A well-defined and commercially consequential structural trend is reshaping product development priorities across the Global dog food packaging market, as the simultaneous pressure of consumer convenience expectations and regulatory circularity obligations is compelling suppliers to upgrade flexible packaging formats from single-performance structures toward integrated architectures that combine resealable dog food bags, mono-material packaging recyclability, premium graphics, and food-grade barrier performance within a single engineered solution that neither sacrifices freshness protection nor concedes shelf appeal. Validated reports from the European Commission confirm that Regulation EU 2025/40 requires the empty-space ratio in grouped, transport, and e-commerce packaging to not exceed 50% from January 2030, directly affecting the secondary packaging design decisions of dog food brands whose online subscription and parcel delivery operations currently depend on oversized cartons, void fill, and protective inserts that will need to be replaced by primary packaging capable of absorbing distribution stress independently.

The commercial implications of this trend extend beyond regulatory compliance into the competitive architecture of the broader flexible packaging supply base, where brands increasingly evaluate suppliers on their ability to deliver resealable packaging with functional closure systems zipper quality, slider performance, press-to-close reliability that preserve aroma, protect texture, and maintain product palatability across the repeated opening cycles that training treats, functional snacks, and portion-fed premium products demand from consumers who use resealability as a direct proxy for packaging quality and brand investment. In line with findings from the U.S. EPA on containers and packaging waste, the structural gap between plastic packaging's market dominance and its comparatively lower recycling recovery rates confirms that sustainable dog food packaging development is not a niche premium positioning choice but a commercially unavoidable reformulation trajectory that suppliers with advanced mono-material coatings, compatible closure systems, and recyclability-validated barrier technology are best placed to lead.

Global Dog Food Packaging Market Opportunity

Premium and Functional Nutrition Formats Are Creating High-Value Packaging Demand Across Multiple Product and Channel Tiers

The most commercially significant and structurally recurring growth opportunity within the Global dog food packaging market lies in the premium and functional nutrition segment, where veterinary diets, high-protein recipes, digestive health formulas, dental treats, joint-support snacks, senior dog products, and fresh-style meals collectively require premium dog food packaging architectures that protect sensitive ingredient systems, communicate functional claims with clinical clarity, and support the higher price positioning that consumers validate through packaging quality, freshness visibility, and labeling precision. As per official figures from the FDA, pet food labels must communicate product identity, ingredient lists, guaranteed analysis, nutritional adequacy statements, and feeding directions, confirming that the regulatory labeling obligation alone creates sustained demand for flexible structures with large, clearly readable printable surfaces, sufficient panel space for multi-claim communication, and food-contact-safe inks and coatings that maintain both compliance and premium aesthetics across the full retail distribution environment.

Pack-size diversification extends this opportunity into a separately significant demand layer, where trial packs, portion packs, single-serve wet food formats, and variety multipacks increase packaging intensity per kilogram of product and create recurring converter revenue from formats that generate higher value density than large bulk bags. Data compiled from internationally recognised public authorities at the FDA confirms that e-commerce-ready packaging for pet food must meet safe handling, labeling, and product-integrity standards across parcel distribution channels that impose compression, vibration, drop, and temperature exposure on packaging structures designed primarily for retail shelf performance, positioning suppliers capable of delivering subscription pet food packaging with reinforced seams, high-integrity heat seals, and secondary packaging compatibility as structurally advantaged partners for the premium and functional dog food brands whose online subscription and direct-to-consumer channels are expanding the addressable base for high-specification flexible packaging fastest.

Global Dog Food Packaging Market Regional Analysis

By Region Type

- North America

- South America

- Europe

- Middle East & Africa

- Asia-Pacific

North America leads the Global dog food packaging market with 40% of global demand, a concentration that reflects the region's exceptional convergence of mature pet ownership depth, premium dog food adoption, organised specialty and mass retail infrastructure, veterinary diet distribution networks, and a rapidly expanding e-commerce subscription channel that collectively create both the volume base and the packaging sophistication requirements that reward suppliers capable of serving multiple distinct channel specifications within a single regional market. As per data published by the FDA, pet food placed on the U.S. market must be safe, produced under sanitary conditions, contain no harmful substances, and carry truthful labeling across product identity, ingredients, guaranteed analysis, and feeding guidance, confirming that the North America dog food packaging market operates within a compliance environment that structurally favours converters with food-contact certification, labeling expertise, and the technical service capability to support brands managing simultaneous retail, veterinary, and e-commerce packaging programmes.

The region's structural advantage is further reinforced by the channel diversity that creates distinct and non-interchangeable packaging demands across mass retail, pet specialty, veterinary clinic, warehouse club, and direct-to-consumer delivery environments where premium dog food packaging must simultaneously deliver shelf visual impact, clinical communication credibility, shipping-grade durability, and subscription-ready resealability across formats serving products as diverse as therapeutic renal diets and grain-free training treats. Validated reports from the U.S. EPA on containers and packaging waste confirm that North American brands and converters are under increasing pressure to improve plastic packaging recovery performance and design-for-recycling credentials across the packaging-intensive pet food category, establishing the region as both the largest commercial demand centre for the market and the most consequential geography for sustainable packaging materials innovation as brand owners, retailers, and packaging suppliers align investment toward the recyclable flexible structures that will define the next competitive tier in dog food packaging development.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Global Dog Food Packaging Market Segmentation Analysis

By Packaging Type

- Bags & Pouches

- Metal Cans

- Folding Cartons

- Containers & Tubs

- Sachets

- Stick Packs

- Others

Bags and pouches command the highest share within the packaging type category at 55%, reflecting the consistent and commercially embedded preference within the Global dog food packaging market for flexible formats that deliver large printable surfaces, strong resealable closure compatibility, lightweight logistics performance, and broad size scalability across the diverse product weight, channel, and formulation requirements that define modern dog food retail. Brands across dry kibble, treat, topper, semi-moist, and functional snack categories consistently select flexible packaging because a single bag or pouch family can be adapted across multiple SKUs, reformatted for premium or value tiers, fitted with zipper closures or carry handles, and resized from 100 g trial formats to multi-kilogram bulk packs without requiring separate packaging infrastructure or major filling-line reconfiguration.

The segment's commercial durability deepens as e-commerce dog food packaging performance requirements intensify across parcel delivery networks where dry dog food bags must absorb compression, vibration, and drop forces across fulfilment centre and last-mile handling that retail shelf packaging was never engineered to withstand. Evidence drawn from public data released by the FDA confirms that pet food labels must carry a regulated complement of product identity, ingredient, analysis, feeding, and manufacturer information that flexible formats accommodate more efficiently than most rigid alternatives, creating a functional advantage for bags and pouches that will sustain the segment's leadership as suppliers invest in recyclable mono-material structures, improved seal systems, and higher-barrier coatings that maintain freshness protection while advancing circularity compliance.

By Material Type

- Plastic

- Paper & Paperboard

- Metal

- Aluminum

- Bio-Based Materials

- Others

Plastic commands the highest share within the material type category at 60%, establishing laminated films, barrier laminates, polyethylene structures, and multi-layer sealant systems as the overwhelmingly dominant material platform within the Global dog food packaging market and reflecting the consistent and performance-driven preference among converters, brands, and retailers for material systems that deliver moisture resistance, oxygen barrier depth, grease control, puncture strength, seal integrity, zipper compatibility, and premium printability within a single material family that no current alternative matches across the full breadth of dry, wet, semi-moist, and treat packaging formats simultaneously. Brands consistently specify flexible plastic packaging because the fat-rich, aroma-sensitive, and moisture-dependent ingredient profiles of modern dog food formulations require barrier systems whose failure modes oxidation, moisture ingress, grease migration, seal failure are commercially and nutritionally consequential in ways that lower-barrier paper or uncoated alternatives cannot reliably prevent.

The segment's structural leadership within the Global dog food packaging market is simultaneously its most commercially scrutinised position, as regulatory pressure from Regulation EU 2025/40 and sustainability commitments from major retailers and brand owners are progressively redirecting converter investment toward recyclable pet food packaging in mono-material PE and PP structures, downgauged films, barrier-coated paper hybrids, and PCR-compatible formats that must demonstrate validated shelf-life, seal, migration, and transport performance before qualifying as credible replacements for the established laminated structures they are designed to succeed. As per data published by the U.S. EPA, plastic containers and packaging have historically underperformed paper and metal categories in recovery rates across municipal solid waste systems, confirming that the transition pressure shaping the material segment is both regulatory and systemic rewarding suppliers that invest in recyclability validation, food-contact-safe coating technology, and compatible closure engineering before competitors establish first-mover advantages in the emerging sustainable pet food packaging tier.

Market Players in Global Dog Food Packaging Market

These market players maintain a significant presence in the Global dog food packaging market sector and contribute to its ongoing evolution.

- Constantia Flexibles

- Sealed Air

- ProAmpac

- Amcor

- Mondi Group

- Sonoco Products Company

- Berry Global

- Huhtamaki

- Winpak

- Silgan Holdings

- Smurfit Westrock

- Coveris

- Printpack

- TC Transcontinental

- Crown Holdings

Market News & Updates

- Mondi Group, 2025:

Mondi launched recyclable packaging for Saga Nutrition’s dry pet food range in June 2025. The new pack replaces non-recyclable multi-material plastic with mono-material re/cycle FlexiBag packaging and protects products from moisture, fat, and odor. The update supports recyclable flexible packaging for dry dog and cat food formats

- ProAmpac, 2025:

ProAmpac received multiple U.S. patents in March 2025 for recyclable and recycle-ready packaging technologies. The patented range includes R-2000 and R-2050 laminates for pet treats, R-1200 heat-resistant recyclable dry food packaging, and RT-4000 ultra-high-barrier retort pouches. The update expands sustainable flexible packaging options for pet food applications.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Global Dog Food Packaging Market Policies, Regulations, and Standards

- Global Dog Food Packaging Pricing Analysis 2022-2032

- Global Dog Food Packaging Pricing Trend (USD/ Pieces) 2022-2032

- Global Dog Food Packaging Pricing Trend (USD/ Pieces) By Regions 2022-2032

- North America

- South America

- Europe

- Middle East & Africa

- Asia Pacific

- Global Dog Food Packaging Pricing Trend (USD/ Pieces) By Packaging Type 2022-2032

- Bags & Pouches

- Metal Cans

- Folding Cartons

- Containers & Tubs

- Sachets

- Stick Packs

- Global Dog Food Packaging Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Global Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Flexible Plastic- Market Insights and Forecast 2022-2032, USD Million

- Rigid Plastic- Market Insights and Forecast 2022-2032, USD Million

- Paper & Paperboard- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Aluminum- Market Insights and Forecast 2022-2032, USD Million

- Bio-Based Materials- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE

- Bags & Pouches- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Folding Cartons- Market Insights and Forecast 2022-2032, USD Million

- Containers & Tubs- Market Insights and Forecast 2022-2032, USD Million

- Sachets- Market Insights and Forecast 2022-2032, USD Million

- Stick Packs- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE

- Dry Dog Food- Market Insights and Forecast 2022-2032, USD Million

- Wet Dog Food- Market Insights and Forecast 2022-2032, USD Million

- Treats & Snacks- Market Insights and Forecast 2022-2032, USD Million

- Frozen Dog Food- Market Insights and Forecast 2022-2032, USD Million

- Functional/Premium Nutrition- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE

- Zipper Packaging- Market Insights and Forecast 2022-2032, USD Million

- Vacuum Packaging- Market Insights and Forecast 2022-2032, USD Million

- Heat-Sealed Packaging- Market Insights and Forecast 2022-2032, USD Million

- Tear Notch- Market Insights and Forecast 2022-2032, USD Million

- Spouted Packaging- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE

- Digital Printing- Market Insights and Forecast 2022-2032, USD Million

- Flexographic Printing- Market Insights and Forecast 2022-2032, USD Million

- Rotogravure Printing- Market Insights and Forecast 2022-2032, USD Million

- Offset Printing- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- BY END USER

- Pet Food Manufacturers- Market Insights and Forecast 2022-2032, USD Million

- Veterinary Nutrition Companies- Market Insights and Forecast 2022-2032, USD Million

- Premium Pet Food Brands- Market Insights and Forecast 2022-2032, USD Million

- Private Label Manufacturers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- BY REGION Type

- North America

- South America

- Europe

- Middle East & Africa

- Asia-Pacific

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- BY MATERIAL TYPE

- Market Size & Growth Outlook

- North America Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- By Country

- The US

- Canada

- Mexico

- Rest of North America

- The US Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- South America Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Brazil

- Argentina

- Rest of South America

- Brazil Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Argentina Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Europe Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- By Country

- Germany

- The UK

- France

- Italy

- Spain

- Rest of Europe

- Germany Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The UK Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- France Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Middle East & Africa Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- By Country

- The UAE

- Saudi Arabia

- South Africa

- Egypt

- Rest of Middle East and Africa

- The UAE Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Saudi Arabia Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Africa Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Egypt Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Asia-Pacific Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- By Country

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Rest of Asia Pacific

- China Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- South Korea Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Australia Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Indonesia Dog Food Packaging Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- BY MATERIAL TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PACKAGING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY DOG FOOD TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY CLOSURE TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY PRINTING TYPE- Market Insights and Forecast 2022-2032, USD Million

- BY END USER- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Amcor

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mondi Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sonoco Products Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Berry Global

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Huhtamaki

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Constantia Flexibles

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sealed Air

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ProAmpac

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Winpak

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Silgan Holdings

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Smurfit Westrock

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coveris

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Printpack

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TC Transcontinental

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Crown Holdings

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Amcor

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| BY MATERIAL TYPE |

|

| BY PACKAGING TYPE |

|

| BY DOG FOOD TYPE |

|

| BY CLOSURE TYPE |

|

| BY PRINTING TYPE |

|

| BY END USER |

|

| BY REGION Type |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.