Kenya Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

Kenya Juice Market Statistics and Insights, 2026

- Market Size Statistics

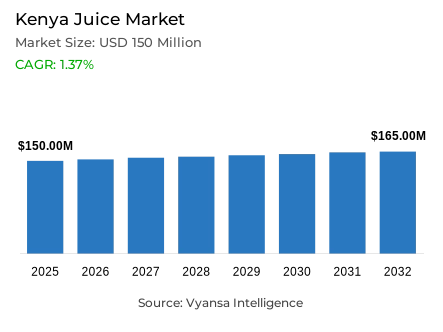

- Juice market size in Kenya was estimated at USD 150 million in 2025.

- The market size is expected to grow to USD 165 million by 2032.

- Market to register a CAGR of around 1.37% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 52%.

- Competition

- More than 5 companies are actively engaged in producing juice in Kenya.

- Top 5 companies acquired around 60% of the market share.

- Ceres Fruit Juices (Pty) Ltd, GlaxoSmithKline Ltd, Coca-Cola East & Central Africa Division, Kevian Kenya Ltd, Del Monte Kenya Ltd etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 95% of the market.

Kenya Juice Market Outlook

The Kenya juice market is in a stage of stable growth, which is fuelled by the high rate of urbanisation, population increase, and a massive change towards health-conscious consumption. The market is estimated to grow to USD 150 million in 2025 and to USD 165 million in 2032 with a CAGR of about 1.37% in the 2026–32 forecast period. As the market nears maturity, an increasing middle-income with increased disposable income is likely to continue the demand, especially in the premium and natural beverage products.

The balance between health and affordability is becoming a defining factor of category performance. At the moment, 100% Juice is dominating the market with a 52% market share due to the increased demand of organic and functional drinks. Nevertheless, nectars are becoming the most vibrant category because their combination of fruit, water, and sugar is a more acceptable and affordable substitute to pure juices. This adaptability in taste and cost allows the manufacturers to appeal to a wider end user market as well as catering to the demands of end users who want the convenience of ready-to-drink beverages in their hectic schedules.

Local production will be transformed by innovation and sustainability. The juice producers in Kenya are increasingly adopting effective technologies that minimize energy and water wastage and also developing value-added products out of the local fruits that are not sold like mangoes and pineapples. These programs help small-scale farmers and are consistent with the increasing end user demands of environmentally friendly practices. Players like Kevian Kenya strengthen their market leadership by emphasizing on local crops and healthier alternatives to industrial carbonates, both in quality and social impact.

Home consumption remains popular in sales channel, with 95% of the market being taken up by off-trade channels. The main touchpoint is still the supermarkets because of their large networks, competitive prices, and convenience of one-stop shopping. In the meantime, e-commerce has become the most vibrant sales channel, particularly among tech-savvy urban customers who appreciate the option of price and product comparison online. This online growth, combined with the development of contemporary grocery stores, offers a strong basis to the further upward trend of the market.

Kenya Juice Market Growth DriverRapid Population Growth and Urbanisation Expanding the Addressable Market for Packaged Juice

The end user base in Kenya is steadily rising and this has maintained the demand of packaged juice despite the fact that the growth in volumes is low. The Kenya National Bureau of Statistics estimates the population to be 53,330,978 as of mid-2025, thus increasing the household population that consumes ready-to-drink beverages. This continuous population growth provides bigger target markets of packaged juice to both urban and more accessible rural end user groups, which provides favourable structural conditions to the category development.

The increase in urbanisation and busier lifestyles makes convenience a priority and ready-to-drink juice and low-cost nectars are the best alternatives to purchase in supermarkets and online stores on a daily basis. This change is facilitated by digital access; the Communications Authority of Kenya estimates that by June 2025, smartphone penetration will reach 83.5%, allowing shoppers to browse, compare, and buy drinks effectively. The retailer promotions and quicker delivery are enabled by mobile connectivity, which strengthens repeat buying among time-conscious end users. With the growth of cities, the availability and visibility of juices in the contemporary retail stores through one-stop shopping and storage enhances the family consumption and daily on-the-go drinking events, which keeps the category moving.

Kenya Juice Market ChallengeFood-Led Input Cost Inflation Compressing Margins and Value-Segment Stability

Unstable input prices are the major obstacles, since the manufacturing of juice is based on fruit, sugar, packaging, and transportation that are highly sensitive to inflation. In December 2025, the Kenya National Bureau of Statistics reported end user price inflation of 4.5% annually, and the Food and Non-Alcoholic Beverages division experienced an increase of 7.8% per year. This disparity indicates that there is a greater pressure on the cost of ingredients that are most important in the production of juice, which puts significant margin pressures on manufacturers.

When the prices of raw materials vary, the brands find it difficult to keep the shelf prices constant without downsizing the packs or sacrificing the quality of taste. This is particularly challenging to value-based nectars, which appeal to shoppers with their low prices and more intense flavour profiles but cannot bear the increased costs. The input-cost pressure also limits the promotional budgets of supermarkets and slows down the processing technology and sustainability programs, keeping the competition in both the high-end and mass-market segments intense. Cost volatility poses a long-lasting operational difficulty, restricting price flexibility and strategic investment in innovation and quality improvement.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Kenya Juice Market TrendRising Non-Communicable Disease Awareness Accelerating Demand for Natural and Functional Juice Blends

Health and wellness offer a definite buying prism to beverages, forcing juice producers to focus on natural, organic, and functional options. In April 2025, the Ministry of Health in Kenya reported that non-communicable diseases are the leading causes of death (39%) and hospitalization (more than 50%) in Kenya. This high disease burden keeps nutrition messaging on the forefront and increases end user interest in the quality of the beverage and its health effects.

This change is in line with market trends where end users are demanding juices that are more like real fruit but offer extra value that fits their hectic schedules. In response, brands offer cleaner ingredient lists, functional blends, and convenient ready-to-drink formats that compete with industrial carbonates on health credentials. With the proliferation of modern shelves and online product listings by retailers, products with a clear sense of wellness become visible and become points of reference in terms of innovation. The underlying concept of this health-related trend is that it is redefining product-development priorities, marketing-communication approaches, and competitive positioning in the changing beverage environment of Kenya, which is becoming more and more characterized by preventive health consciousness and functional nutrition expectations.

Kenya Juice Market OpportunityHigh Smartphone Penetration Enabling Scalable E-Commerce and Direct Consumer Engagement

Juice is scalable through online retailing because customers can easily compare flavours and prices. There is a high level of digital readiness; the Communications Authority of Kenya reports that smartphone penetration is 83.5% by June 2025 and total data subscriptions are 58.5 million as of 30 June 2025. This connectivity helps e-commerce grow, as large platforms are stocked with complete lines of soft-drinks and juice can be seen as part of the regular basket construction that fits into busy urban schedules.

In the case of juice producers, online shelves help launch organic and functional lines, create a trial with bundled offers, and reach time-conscious end users with repeat offers. Local sourcing of fruits and environmentally friendly practices can be used as a differentiating factor by brands. With the growth of supermarkets and marketplaces in delivery and pickup services, digital execution can boost the frequency of purchases even with limited in-store promotions. The development of e-commerce channels allows effective testing of the market, direct interaction with end users, and personalisation strategies based on data that can be used to expand categories beyond the limits of traditional retail in the fast-digitising end user environment of Kenya

Unlock Market Intelligence

Explore the market potential with our data-driven report

Kenya Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the Kenya juice market, where 100% Juice grabbed a market share of 52%. This segment remains the preferred choice for a growing number of health-conscious end users who prioritize natural and organic ingredients. The market's shift toward functional beverages has bolstered this category, as shoppers increasingly seek juices that offer specific health benefits without the addition of preservatives or industrial sugars.

Despite the dominance of 100% juice, the nectar category is seeing the most rapid growth due to its superior affordability and diverse flavor profiles. Nectars are particularly popular for acidic or pulpy fruits, offering a thicker, sweeter experience that many Kenya end users prefer. Moving forward, manufacturers are expected to innovate within both segments by introducing "drinkable salads" and vitamin-fortified blends to cater to the diverse preferences of the expanding middle class.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 95% of the market. This overwhelming majority highlights the central role of retail in the daily lives of Kenya end users. Supermarkets lead this sector, utilizing their widespread physical presence and frequent promotional campaigns to attract budget-conscious shoppers. These retailers provide the essential convenience of allowing end users to buy juice alongside other household staples, solidifying their position as the primary sales channel hub.

While physical stores dominate, the landscape is being reshaped by the rapid rise of e-commerce. Online platforms are currently the most dynamic channel, offering unmatched convenience for time-pressed urban residents. This digital shift allows for easier product comparison and bulk purchasing, which is becoming increasingly attractive as the market matures. As modern grocery networks continue to expand into new urban centers, the off-trade channel is expected to maintain its commanding lead over the on-trade foodservice sector.

List of Companies Covered in Kenya Juice Market

The companies listed below are highly influential in the Kenya juice market, with a significant market share and a strong impact on industry developments.

- Ceres Fruit Juices (Pty) Ltd

- GlaxoSmithKline Ltd

- Coca-Cola East & Central Africa Division

- Kevian Kenya Ltd

- Del Monte Kenya Ltd

- Sameer Agriculture & Livestock Ltd

- Excel Chemicals Ltd

Competitive Landscape

Kenya’s juice market in 2025 is led by Kevian Kenya Ltd, which maintains a clear leadership position through its diversified portfolio of locally sourced fruit juices, strong farmer partnerships, and modern production capabilities, reinforcing both quality and sustainability credentials. Kevian is also the most dynamic player, supported by recent investment that has expanded operational capacity and distribution reach. Nectars represent the fastest growing category, competing primarily on affordability and flavour variety, while 100% and organic juices target an emerging middle class seeking premium and health oriented options. Indirect competition from carbonates and other soft drinks remains relevant, particularly on price. Key differentiation opportunities lie in functional and organic innovation, sustainable sourcing, value added processing of surplus fruit, and deeper penetration of modern retail and e-commerce channels.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Kenya Juice Market Policies, Regulations, and Standards

- Kenya Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Kenya Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Kenya 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kenya Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Kevian Kenya Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Del Monte Kenya Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sameer Agriculture & Livestock Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coca-Cola East & Central Africa Division

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Excel Chemicals Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ceres Fruit Juices (Pty) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GlaxoSmithKline Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kevian Kenya Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.