Kazakhstan Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

Kazakhstan Juice Market Statistics and Insights, 2026

- Market Size Statistics

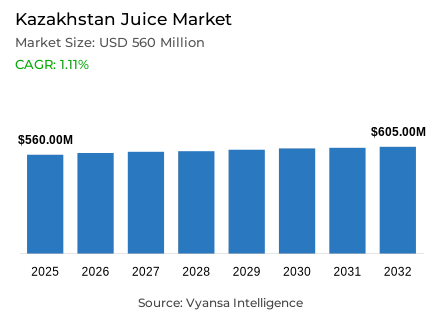

- Juice market size in Kazakhstan was estimated at USD 560 million in 2025.

- The market size is expected to grow to USD 605 million by 2032.

- Market to register a CAGR of around 1.11% during 2026-32.

- Category Shares

- Juice drinks (up to 24% juice) grabbed market share of 60%.

- Competition

- More than 10 companies are actively engaged in producing juice in Kazakhstan.

- Top 5 companies acquired around 65% of the market share.

- Lebedyanskiy OAO, Sady Pridonya OAO NPG, Wimm-Bill-Dann Produkty Pitania OAO, RG Brands AO, Coca-Cola Almaty Bottlers SP etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 90% of the market.

Kazakhstan Juice Market Outlook

The Kazakhstan juice market is entering a phase of stabilization and modest recovery. Estimated at USD 560 million in 2025, the market is projected to reach USD 605 million by 2032, growing at a CAGR of approximately 1.11% during the 2026–32 period. While this marks a positive shift from recent volume declines, growth remains tempered by persistent price sensitivity and a significant upcoming tax change. The planned increase in VAT from 12% to 16% starting January 1, 2026, is expected to heighten retail prices, compelling manufacturers to rely heavily on promotions and discounts to sustain demand.

Affordability is the primary driver of market dynamics, with Juice Drinks (up to 24% juice) grabbing a 60% market share. end users are increasingly gravitating toward these lower-juice-content products, viewing them as affordable refreshments and indulgent treats rather than strictly natural vitamin sources. This shift is particularly evident as sales of premium nectars and 100% reconstituted juices decline. In response, market leaders like RG Brands and Coca-Cola are focusing on innovative flavors—such as mojito and sparkling blends—and functional enhancements like immunity-boosting vitamins to differentiate their "budget-friendly" offerings.

Innovation within the industry is pivoting toward value-added benefits and flavor differentiation to combat the lack of premium growth. Major players are adding functional claims, such as the "Piko Immunity" and "Da Da" vitamin-enriched lines, to appeal to health-conscious shoppers without the high price tag of 100% juice. At the premium end, not-from-concentrate juice remains a niche category, though the emergence of cold-pressed juices and fruit purées is attracting affluent urban end users who prioritize quality and minimal processing.

The sales channel landscape is firmly anchored in retail, with Off-Trade channels grabbing 90% of the market. Small local grocers still lead in volume due to their dominance in rural areas, but modern formats like supermarkets and convenience stores are rapidly gaining ground. The "Digital Kazakhstan" program and partnerships between major retailers and e-commerce platforms like Kaspi.kz are accelerating the shift toward online shopping, which is currently the market's most dynamic channel. Additionally, rising tourist numbers are providing a slight boost to the smaller on-trade foodservice sector.

Kazakhstan Juice Market Growth DriverInflation-Driven Budget Constraints Sustaining Value-Led Juice Drink Demand

Persistently elevated inflation is reinforcing end user preference for affordable beverage options, positioning juice beverages as a cost-effective choice across many households. The Bureau of National Statistics reports that in October 2025, the annual inflation was 12.6%, which demonstrates the constant strain on everyday spending and the increased sensitivity to the price level on the shelf. This long-term inflationary context strengthens value-based buying behavior and constrained discretionary expenditure on high-end beverage segments, thus entrenching juice drinks as convenient refreshing options in tight household budgets.

The brands react by protecting entry-level prices and increasing flavour selections in the value segment, taking advantage of the fact that formulations can be changed easily without a significant rise in costs. This plan forms the basis of impulse buying in small, local grocers where speed and distance are the most important factors, helping the category to recover previous volume losses. Large competitors add vitamins and immunity indicators to make purchases without a premium price. Customers mainly purchase juice to have fun and to quench thirst and not as a nutritional supplement, which makes taste diversity an effective tool to maintain product appeal within constrained budgets. This value-based demand trend creates long-term volume opportunities of low-cost, flavour-differentiated juice formulations in the price-sensitive end user groups in the entire of Kazakhstan.

Kazakhstan Juice Market ChallengeVAT Increases and Cost Pass-Through Pressures Constraining Premium Portfolio Expansion

High indirect taxes and chronic inflation limit the ability to flex prices, thus limiting the ability of juice brands to grow premium lines at scale. According to the Office of the President of Kazakhstan, the current value-added tax rate is 16%, and the new Tax Code, which will take effect on 1 January 2026, increases the cost base of most retail goods. This tax increment adds to the already existing inflationary pressures and reduces the capacity of manufacturers to absorb the costs without passing them to end users.

Since the price sensitivity of end users is already high, further price pass-through induces a change towards less expensive juice products and undermines the demand of non-from-concentrate products. Manufacturers and retailers focus on discounts, multipacks, and promotional exposure to maintain volumes, which may erode margins and reduce investment in new formats. The pressure is heightened on nectars and reconstituted juices, where the perceived value is less strong, and they are enticed to easily switch to flavour-enhanced juice drinks that can provide indulgence at reduced prices. The cost increase through taxation poses structural barriers to the premiumisation strategies and limits the value addition potential of the category in the economically constrained end user market in Kazakhstan.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Kazakhstan Juice Market TrendAccelerating E-Commerce Penetration Reshaping Juice Distribution and Consumer Reach

The rapid growth of online grocery and marketplace shopping across Kazakhstan identifies e-commerce as a more visible market channel of juice brands. According to the information service of the Prime Minister, the volume of online sales reached about 2.7 trillion tenge in the first nine months of 2025, which is 14% higher than the same period of 2024. This intensive growth in digital commerce creates new distribution channels and end user touchpoints that are not limited to the physical stores.

With the expansion of delivery networks and the improvement of the efficiency of the last mile through the expansion of dark stores and pickup locations, juice will become more accessible, as well as daily staples, not limited to regular supermarket visits. This shift promotes wider experimentation with new flavours and functional options, with digital shelves bringing niche products and offers to the forefront in a short period of time. Retailers with a mix of large store presence and online collaborations such as marketplace alignments and dedicated e-grocery services will increasingly determine visibility, pricing, and repeat-purchase behaviour of mainstream juice drinks in large cities. The expansion of the e-commerce channel enables brands to reach digitally oriented end users, experiment innovations effectively, and build direct relationships, which form the basis of long-term category development.

Kazakhstan Juice Market OpportunityRising Urban Incomes Enabling Niche Growth for Premium Clean-Label Juice Formats

A growing premium niche is emerging around minimally processed juice formats, such as cold-pressed blends and fruit purée offerings, which are increasingly positioned to convey superior quality and enhanced value perception among end users. This premiumisation trend is supported by increased urban purchasing power, with the Bureau of National Statistics showing average monthly wages of 448,620 tenge in the second quarter of 2025, an increase of 11.3% per annum. The increasing income of urban end users in the shopping market provides segments that can be addressed by offering high-quality products and positioning them as healthy.

Wealthy customers who are more concerned with natural ingredients are more willing to pay a higher price to not-from-concentrate products, especially when the brands relate them to wellness and clean-label qualities. This situation offers a chance of targeted premium portfolios in contemporary retail, cafes, and selective online platforms instead of mass growth. By integrating quality signals with convenient delivery and attractive in-store narratives, companies can develop repeat buying without necessarily competing on price. Premium lines strengthen brand image and create greater margins in contemporary channels, which allow strategic differentiation and margin improvement in the changing urban beverage market in Kazakhstan.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Kazakhstan Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category for the Kazakhstan juice market, where Juice Drinks (up to 24% juice) grabbed a market share of 60%. This dominance is rooted in the segment's superior affordability compared to 100% juices and nectars, making it the go-to choice for price-sensitive households. Rather than seeking pure fruit content, end users increasingly prioritize these drinks for their refreshing qualities and variety of trendy flavors, such as "Piko Boost" or specialized vitamin-enriched blends from brands like Da Da.

Innovation within this segment is highly flexible, allowing companies to quickly adjust formulations to meet evolving tastes. While 100% juices remain a niche product for affluent urban end users, juice drinks are expected to maintain their lead by capturing the mass market. As economic pressures like high inflation and the 2026 VAT hike take hold, the competitive pricing of this segment will be essential in preventing a total volume decline in the broader juice category.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 90% of the market. Retail remains the undisputed leader in sales channel, primarily through small local grocers that serve as vital hubs for rural and remote communities. However, there is a clear trend toward modern retail expansion, with supermarkets and hypermarkets slowly consolidating their value share through broader product ranges and frequent promotional activities.

The off-trade sector is also being reshaped by a rapid rise in convenience stores and e-commerce. As urban end users prioritize speed and proximity, "dark stores" and last-mile logistics improvements have made online juice purchases more efficient. Although the on-trade (foodservice) channel contributes a sizeable portion of volume—supported by rising tourism—the convenience and bulk-buying opportunities found in off-trade channels continue to secure the vast majority of end user spending in Kazakhstan.

List of Companies Covered in Kazakhstan Juice Market

The companies listed below are highly influential in the Kazakhstan juice market, with a significant market share and a strong impact on industry developments.

- Lebedyanskiy OAO

- Sady Pridonya OAO NPG

- Wimm-Bill-Dann Produkty Pitania OAO

- RG Brands AO

- Coca-Cola Almaty Bottlers SP

- Raimbek Bottlers TOO

- Caspian Beverage Holding AO

- Galanz Bottlers AO

- Multon AO

- Marmariss TOO

Competitive Landscape

Kazakhstan’s juice market in 2025 is led by RG Brands, which holds nearly a quarter of volume share through a tiered portfolio including Da Da, Gracio, and Solnechny, covering mid tier, premium, and mass segments with strong distribution and brand familiarity. Coca Cola ranks second with Piko, Dobriy, and Rich, increasingly leveraging functional positioning such as immunity focused SKUs to defend share in juice drinks up to 24% juice. Galanz Bottlers is the fastest growing challenger, driven by its Garden brand positioned as affordable everyday quality with promotional intensity and larger pack formats. Indirect competition stems from other low cost soft drinks amid persistent inflation. Key differentiation opportunities lie in flavour innovation, functional vitamin fortification, affordable premiumisation in urban centres, and digital channel expansion through e commerce partnerships.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Kazakhstan Juice Market Policies, Regulations, and Standards

- Kazakhstan Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Kazakhstan Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Kazakhstan 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kazakhstan Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kazakhstan Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kazakhstan Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Kazakhstan Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- RG Brands AO

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coca-Cola Almaty Bottlers SP

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Raimbek Bottlers TOO

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Caspian Beverage Holding AO

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Galanz Bottlers AO

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lebedyanskiy OAO

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sady Pridonya OAO NPG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Wimm-Bill-Dann Produkty Pitania OAO

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Multon AO

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Marmariss TOO

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- RG Brands AO

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.