Italy Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

Italy Juice Market Statistics and Insights, 2026

- Market Size Statistics

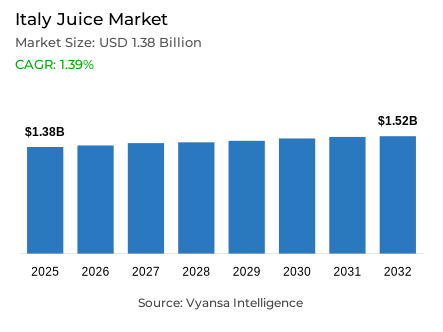

- Juice market size in Italy was estimated at USD 1.38 billion in 2025.

- The market size is expected to grow to USD 1.52 billion by 2032.

- Market to register a CAGR of around 1.39% during 2026-32.

- Category Shares

- Nectars grabbed market share of 60%.

- Competition

- More than 20 companies are actively engaged in producing juice in Italy.

- Top 5 companies acquired around 45% of the market share.

- CONAD – Consorzio Nazionale Dettaglianti Scrl, Acqua Minerale San Benedetto SpA, Esselunga SpA, Conserve Italia scarl, Zuegg SpA etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 75% of the market.

Italy Juice Market Outlook

The Italy juice market is in a difficult phase characterized by the changing end user health concerns and economic demands. The market is estimated to be US USD 1.38 billion in 2025 and is expected to decline to US USD 1.52 billion in 2032 with a negative CAGR of about 1.39% in the 2026–32 period. This decline is mainly caused by the drastic rise in prices and the increasing concern about sugar content, which has made many people turn their backs on the traditional juice in favour of flavoured water, tea, and plant-based beverages.

The largest volume segments are the most affected by the decline. Nectars, with 60% market share, and reconstituted 100% juices are not doing well because end users feel that they are too processed and sweet. In retaliation, manufacturers are hastily re-packaging portfolios to emphasize no added sugar claims. Although the overall trend is downward, there are areas of strength premium Not From Concentrate (NFC) 100% juice and functional juice beverages are gaining popularity among end users who are prepared to pay a premium price to get natural ingredients and health benefits.

The innovation is emerging as the major defence strategy in the industry. Brands like San Benedetto and Fonti di Vinadio are also introducing products that combine juice with functional value, like energy-enhancing caffeine or taurine, to reclaim end users who are moving to energy drinks. Moreover, the sustainability issue is also a priority, as such market leaders as Conserve Italia have launched environmentally friendly packaging made of recycled materials to attract environmentally conscious end users.

The sales channels are still very much rooted in physical retail with off-trade channels controlling 75% of the market. Supermarkets maintain the top spot through intensive promotions and large product lines to counter discounters. Nevertheless, retail e-commerce has become the most vibrant channel due to the need to be convenient and the so-called stock-up behaviour of busy urban families.

Italy Juice Market Growth DriverHealth-First Consumer Mindset Accelerating Low-Sugar Reformulation and Clean-Label Demand

Rising health consciousness among end users in Italy is driving closer scrutiny of juice products, particularly regarding sugar content and the extent of processing involved. According to the National Institute of Health, four out of ten adults aged between 18 and 69 years of age have excess weight with three being overweight and one obese. This medical context significantly increases the importance of better-for-you product cues and creates a demand of beverages that are perceived as lighter and more nutritionally credible. Health consciousness among end users has long-term reformulation and clear nutrition communication pressure.

Brands, in turn, reposition products strategically and focus on a clear no added sugar positioning, thus maintaining the consumption occasions of juice even as traditional nectars lose their popularity. Premium 100% not-from-concentrate and plant-based versions are appealing as they are closer to the trend of natural ingredients and preservation of nutrients. High-pressure processing technologies become one of the most popular techniques that can be used to preserve nutrients and make cleaner label claims. This health-based reformulation trend essentially redefines the product development priorities and competitive positioning throughout the Italy juice category.

Italy Juice Market ChallengeInflationary Pressures and Sugar Skepticism Suppressing Mainstream Juice Consumption

Escalating unit prices are constraining juice sales, as financially pressured households reassess discretionary spending and increasingly compare the caloric value of beverage alternatives. According to ISTAT, in March 2025, the all-items end user price index in Italy increased 2.0% year-on-year, and the prices of grocery and unprocessed-food increased 2.1% year-on-year. This long-term price inflation limits discretionary expenditure on beverages and promotes value-based buying behaviour. The structural headwinds are economic pressures that constrain the expansion potential of the category.

At the same time, sugar-and-processing issues affect mainstream choices, especially nectars and reconstituted 100% juice. As substitutes like mineral water, ready-to-drink tea, flavoured water are readily available, increased shelf prices and reduced health perceptions work together to dampen volumes significantly. The economic constraint and health scepticism are converging and putting a two-fold pressure on the traditional juice categories. This tough climate requires repositioning and re-formulation to stay relevant in the face of price-sensitive, health-conscious end users who are moving through the crowded beverage markets with growing low-calorie options.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Italy Juice Market TrendShift Toward No-Added-Sugar and Functional Formulations Redefining Category Innovation

Health and wellness positioning is emerging as a defining direction in juice innovation, prompting brands to reduce sugar content and articulate clearer, function-focused benefits in their product offerings. A formal AGENAS evaluation, organized by the Italy Ministry of Health, gives a prevalence of diabetes of 7.7% in the population aged 20 to 79 years in 2024, which corresponds to about five million people; the overall expenditure on diabetes in Italy is about 8 billion euros per year with indirect costs. This high disease burden supports end user interest in sugar reduction and metabolic health concerns.

In reaction, juice companies are increasingly seeking no added sugar formulations and introducing lines with functional claims like energy or digestive support to compete with soft drinks with performance claims. High-pressure processing, as well as other advanced processing techniques, become prominent as they assist in preserving nutrients and brands modify recipes and reinforce label claims. Functional innovation facilitates differentiation of the traditional juice attributes. This shift to health-optimised formulations with clear functional advantages is a strategic development that responds to regulatory forces as well as end user wellness concerns in the competitive Italy beverage environment.

Italy Juice Market OpportunityExpanding E-Commerce Adoption Unlocking Premium and Functional Juice Scalability

Retail e-commerce provides a faster channel to access time-bound end users in need of convenient and quality drinks. According to ISTAT, online retail sales increased by 7.3% in September 2025 compared to September 2024, and non-store retail sales increased by 1.9%. This online channel expansion presents significant potentials of premium juice positioning and end user targeting. The growth of e-commerce allows brands to circumvent the traditional retailing restrictions and reach digitally active end user segments directly.

To manufacturers, this channel enables curated multi-packs, targeted promotions, and overall product education on functional ingredients—communication strategies that are more difficult to implement on crowded physical shelves. With more and more shoppers ordering groceries to be delivered to their homes, brands that establish a high search presence and compelling product pages will be able to tap into the demand of high-quality 100% not-from-concentrate and no-added-sugar lines. Digital platforms facilitate premium positioning by providing better storytelling, open ingredient information, and convenience-based formats. This online business opportunity allows brands to build direct end user relationships and differentiate with digital-first marketing approaches in line with changing shopping behaviours.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Italy Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category for the Italy juice market, where Nectars grabbed a market share of 60%. Despite this commanding position, the segment is currently the primary drag on the industry's overall performance. Nectars are facing a severe contraction in volume as Italy end users increasingly view them as unhealthy due to their high sugar content and perceived lack of nutritional value compared to fresh alternatives.

To mitigate these losses, major players like Conserve Italia are reformulating their nectar lines—such as the Yoga brand—to feature higher fruit content and reduced sugar. However, the shift in end user preference remains distinct, with many shoppers trading these traditional products for "no added sugar" juice drinks or functional waters. Consequently, while nectars remain the volume leader, their dominance is eroding as the market pivots toward lighter, more natural-profile beverages.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 75% of the market. This channel's stability is largely supported by supermarkets, which continue to lead sales channel through diverse premium assortments and multi-buy promotional strategies that offer perceived value amidst rising prices. Discounters also play a crucial role, attracting budget-conscious end users who are prioritizing affordability over brand loyalty during economic inflation.

While traditional grocery retailers dominate volume, the landscape is evolving. Retail e-commerce has become the most dynamic sub-channel, driving growth through the convenience of home delivery. As busy lifestyles limit time for physical shopping, end users are increasingly turning to digital platforms to purchase bulky juice products, incentivized by transparent pricing and the ease of comparing sustainable and healthy options online.

List of Companies Covered in Italy Juice Market

The companies listed below are highly influential in the Italy juice market, with a significant market share and a strong impact on industry developments.

- CONAD – Consorzio Nazionale Dettaglianti Scrl

- Acqua Minerale San Benedetto SpA

- Esselunga SpA

- Conserve Italia scarl

- Zuegg SpA

- Parmalat SpA

- Rauch Italia Srl

- Coop Italia scarl

- CoGeDi International SpA

- Carrefour Italia GS SpA

Competitive Landscape

Italy’s juice market in 2025 is led by Conserve Italia, which strengthened share through reformulation of its Yoga brand, zero sugar extensions such as Derby Blue Zero, and sustainability focused packaging, positioning itself at the intersection of health and environmental awareness. CoGeDi is the fastest growing competitor, expanding via Elisir di Rocchetta in juice drinks, while Fonti di Vinadio and San Benedetto are reshaping competition through no added sugar launches and functional propositions such as energy infused juice formats. Nectars and reconstituted 100% juice are under structural pressure from sugar concerns and limited innovation. Indirect competition from RTD tea, flavoured water, plant based drinks, and energy drinks intensifies substitution. Differentiation opportunities centre on no added sugar reformulation, High Pressure Processing, functional energy claims, and premium natural positioning.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Italy Juice Market Policies, Regulations, and Standards

- Italy Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Italy Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Italy 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Italy Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Conserve Italia Consorzio Cooperative Conserve Italia scarl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zuegg SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Parmalat SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rauch Italia Srl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coop Italia scarl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CONAD Consorzio Nazionale Dettaglianti Scrl

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Acqua Minerale San Benedetto SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Esselunga SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CoGeDi International SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Carrefour Italia GS SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Conserve Italia Consorzio Cooperative Conserve Italia scarl

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.