Israel Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

Israel Juice Market Statistics and Insights, 2026

- Market Size Statistics

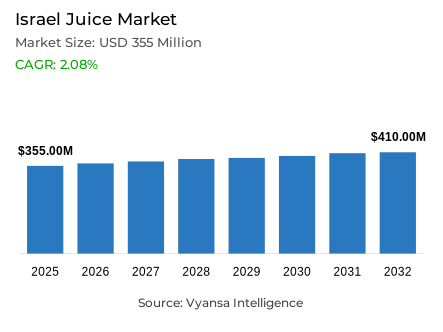

- Juice market size in Israel was estimated at USD 355 million in 2025.

- The market size is expected to grow to USD 410 million by 2032.

- Market to register a CAGR of around 2.08% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 52%.

- Competition

- More than 10 companies are actively engaged in producing juice in Israel.

- Top 5 companies acquired around 90% of the market share.

- Greenfield Foods Ltd, Naturafood Ltd, Tomer Import & Export Ltd, Gat Food Canneries Ltd, Ganir Ltd etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 80% of the market.

Israel Juice Market Outlook

The Israel juice market is experiencing a gradual recovery with the retail volume sales resuming growth in 2025. The recovery is mainly fuelled by the reduction of inflationary pressures, which have increased end user confidence and reduced the rate of price increases. The market is estimated to be at 355 million dollars in 2025 and 410 million dollars in 2032, with a CAGR of about 2.08% in the forecast period. The increasing population and a changing preference towards beverages that are seen as natural and wholesome also support demand.

The major driver of the industry is health-consciousness. Although 100% Juice has a leading market share of 52%, end users are becoming more sensitive to sugar content and artificial additives. This has given rise to a hybrid attitude towards individual categories "Not from Concentrate" (NFC) 100% juice is becoming the star performer because of its better nutritional profile, and nectars and reconstituted juices will experience steady declines. Innovations, like the orange juice with less sugar that Priniv has created with the help of BlueTree Technologies, will gain more visibility as brands seek to escape the red warning labels of the Ministry of Health.

Jafora-Tabori is the market leader and enjoys a solid market position in juice drinks and nectars, but is under mounting pressure due to health trends. The most active player is Ganir Ltd (Primor brand), which is taking advantage of the high demand of high quality 100% juices. To stay competitive, key players are repackaging the current products using natural sweeteners like stevia and erythritol to retain flavour but significantly lower sugar content.

The shopping habits in Israel are still value-based with off-trade channels taking 80% of the market. Discounters remain the best retail store since they provide low prices to end users who are struggling with high living expenses. But more hectic urban living is driving the increase in convenience stores and vending machines to buy on the spur of the moment. E-commerce is also emerging as an active channel, with more digital investments by large grocery chains and a end user preference to the variety and price offers offered online.

Israel Juice Market Growth DriverCooling Inflation and Demographic Expansion Strengthening Baseline Juice Demand Fundamentals

Easing inflationary pressures is strengthening end-user confidence and supporting discretionary expenditure on beverage products. According to the Bank of Israel, the consumer Price Index in November 2025 decreased by 0.5%, and the annual inflation was 2.4%. This moderation reduces the rate of increase in the prices of grocery baskets and helps to buy juice more often, especially when the brands underpin new introductions with promotional backing and improved retail presence. Macro-economic stabilisation provides good conditions of category expansion and end user trial.

Increasing end user bases also increase the level of demand. According to the Central Bureau of Statistics of Israel, the population stood at 10.178 million at the end of 2025, which indicates a consistent demographic growth. As more households grow and the shopping is conducted in large grocery chains, the category enjoys greater sales-channel penetration and growing interest in beverages with natural and wholesome images. The combination of population growth and inflation moderation creates favorable market fundamentals to support the development and volume growth of the juice-category.

Israel Juice Market ChallengeElevated Household Food Insecurity Constraining Premiumisation and Trading-Up Potential

Heightened price sensitivity among end users constrains demand, as juice is often perceived as a relatively high-cost option when purchasing priorities shift toward essential goods. According to the National Insurance Institute, 27.1% of households were food insecure in 2024 because of economic factors, which translates to about 968,000 households and 2.8 million individuals, including about one million children. This high level of food insecurity is why most end users are actively pursuing cheaper prices and offers in discounter channels, limiting the growth of the premium-segment.

Here, the premium juices containing more real fruits and vegetables are in a difficult market position, and the cheaper soft drinks may be preferred in the process of regular shopping events. Although inflation is subsiding, cautious spending keeps demand weak and forces brands to protect volume by using smaller packs, discounts, and competitive prices. The economic susceptibility of large household groups poses structural obstacles to premiumisation plans and constrains the readiness to pay more to obtain higher-quality formulations despite increasing health awareness.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Israel Juice Market TrendMandatory Front-of-Pack Sugar Labelling Accelerating Reformulation and Health-Led Innovation

Heightened health awareness is increasingly shaping end user preferences in the juice category, with sugar content emerging as a decisive purchase consideration. The Ministry of Health in Israel needs front-warning labels on drinks with more than 5 grams of sugar per 100 millilitres. This regulation causes the sugar level to be very visible at the shelf and compels brands to re-engineer recipes and communication tactics to remain attractive to health-conscious end users. Compulsory labeling establishes open information spaces that radically transform the priorities of product-development.

Innovation is therefore focused on products that are located as least processed and as near to natural ingredients, particularly not-from-concentrate products. To defend demand in mature categories, manufacturers re-package existing lines and launch lower-sugar versions, and marketing focuses on cleaner labels and fewer additives that respond to end user concerns. Joint innovations like the Priniv orange juice with reduced sugar content created with BlueTree Technologies are examples of strategic reactions to regulatory demands and changing end user tastes towards healthier formulations.

Israel Juice Market OpportunityImproving Monetary and Currency Conditions Enabling Strategic Investment and Premium Portfolio Expansion

The stabilization of inflation creates favorable conditions for brands to expand investments in innovation that closely aligns with the growing shift toward healthier preferences among end users. The Bank of Israel reports that the Monetary Committee reduced the policy interest rate to 4% on 5 January 2026, and that the shekel had appreciated by 12.5% against the US dollar in 2025. Reduced funding expenses and a robust currency favour investment choices related to the modernisation of packaging, sourcing materials and increasing marketing support, which provide favourable circumstances to strategic initiatives.

This underpins the prospects in high-end, naturally positioned juices like not-from-concentrate formulations, and reduced-sugar lines that respond to wellness concerns. It reinforces the argument of enhancing accessibility in contemporary grocery stores and convenience-based points of sale, where impulse buying increases with the speed of lifestyle and shoppers prefer fast and reliable solutions. Improved operating conditions allow brands to seek innovation, channel growth, and premium positioning approaches that take advantage of health trends and remain competitive in accessibility through diversified retail relationships.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Israel Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category for the Israel juice market, where 100% Juice grabbed a market share of 52%. This segment’s leadership is anchored by the Not from Concentrate (NFC) variety, which resonates with health-conscious israels seeking minimally processed, additive-free options. Trusted brands like Primor (Ganir Ltd) have successfully positioned 100% juice as a premium health choice, despite its higher price point, by emphasizing its high vitamin and mineral retention compared to reconstituted alternatives.

As end users move away from "sweetened" labels, 100% juice is undergoing further refinement through food-tech collaborations that remove naturally occurring sugars without sacrificing taste. While other categories like nectars face a steady decline due to their high sugar reputation, the 100% juice segment is expected to remain the market's primary pillar. Its growth is sustained by continuous advertising and a loyal end user base that views pure fruit juice as a necessary component of a wholesome daily diet.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 80% of the market. This dominance is largely credited to the strength of discounters, which have expanded their presence in both major urban centers and smaller cities. Israels increasingly prefer off-trade purchases to find value-for-money deals and private label alternatives. This channel is also benefiting from a surge in impulse buying through vending machines and convenience stores, which cater to the "on-the-go" needs of a population with increasingly busy professional lives.

While store-based retail remains the backbone of juice sales channel, e-commerce is the most dynamic sub-channel. Retailers are investing heavily in digital marketing and streamlined delivery services, making online grocery shopping a preferred choice for end users seeking bulk discounts and specialty health juices. This robust off-trade infrastructure ensures that juice remains highly accessible, whether for planned family breakfasts at home or quick, functional refreshment throughout the day.

List of Companies Covered in Israel Juice Market

The companies listed below are highly influential in the Israel juice market, with a significant market share and a strong impact on industry developments.

- Greenfield Foods Ltd

- Naturafood Ltd

- Tomer Import & Export Ltd

- Gat Food Canneries Ltd

- Ganir Ltd

- Jafora-Tabori Ltd

- Priniv Ltd

- Tempo Beverages Ltd

- Adir RY Trade Ltd

- Kibbutz Neot Semadar

Competitive Landscape

Israel’s juice market in 2025 is led by Jafora Tabori, which maintains overall volume leadership through strong positions in nectars and juice drinks under brands such as Spring and Tapuzina, supported by wide distribution and ongoing reformulation to reduce sugar. However, its exposure to slower declining categories has pressured share. Ganir Ltd is the most dynamic competitor, driven by its dominance in not from concentrate 100% juice via the premium positioned Primor brand, capitalising on health and naturalness trends. Priniv is emerging through reduced sugar innovation enabled by foodtech partnerships. Indirect competition from other soft drinks and heightened sugar scrutiny constrain growth in reconstituted juice and nectars. Key differentiation opportunities lie in clean label reformulation, sugar reduction technologies, and premium natural positioning aligned with wellness demand.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Israel Juice Market Policies, Regulations, and Standards

- Israel Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Israel Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Israel 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Israel Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Israel Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Israel Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Israel Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Gat Food Canneries Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ganir Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Jafora-Tabori Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Priniv Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tempo Beverages Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Greenfield Foods Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Naturafood Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tomer Import & Export Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Adir RY Trade Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kibbutz Neot Semadar

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gat Food Canneries Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.