US Wearable Electronics Market Report: Trends, Growth and Forecast (2025-2030)

By Product (Activity Wearables, Smart Wearables), By Application (Healthcare, Entertainment, Industrial, Others), By Sales Channel (Offline, Online) ... Read more

|

Major Players

|

US Wearable Electronics Market Statistics, 2025

- Market Size Statistics

- Wearable Electronics in US is estimated at $ 10.94 Billion.

- The market size is expected to grow to $ 12.09 Billion by 2030.

- Market to register a CAGR of around 1.68% during 2025-30.

- Product Shares

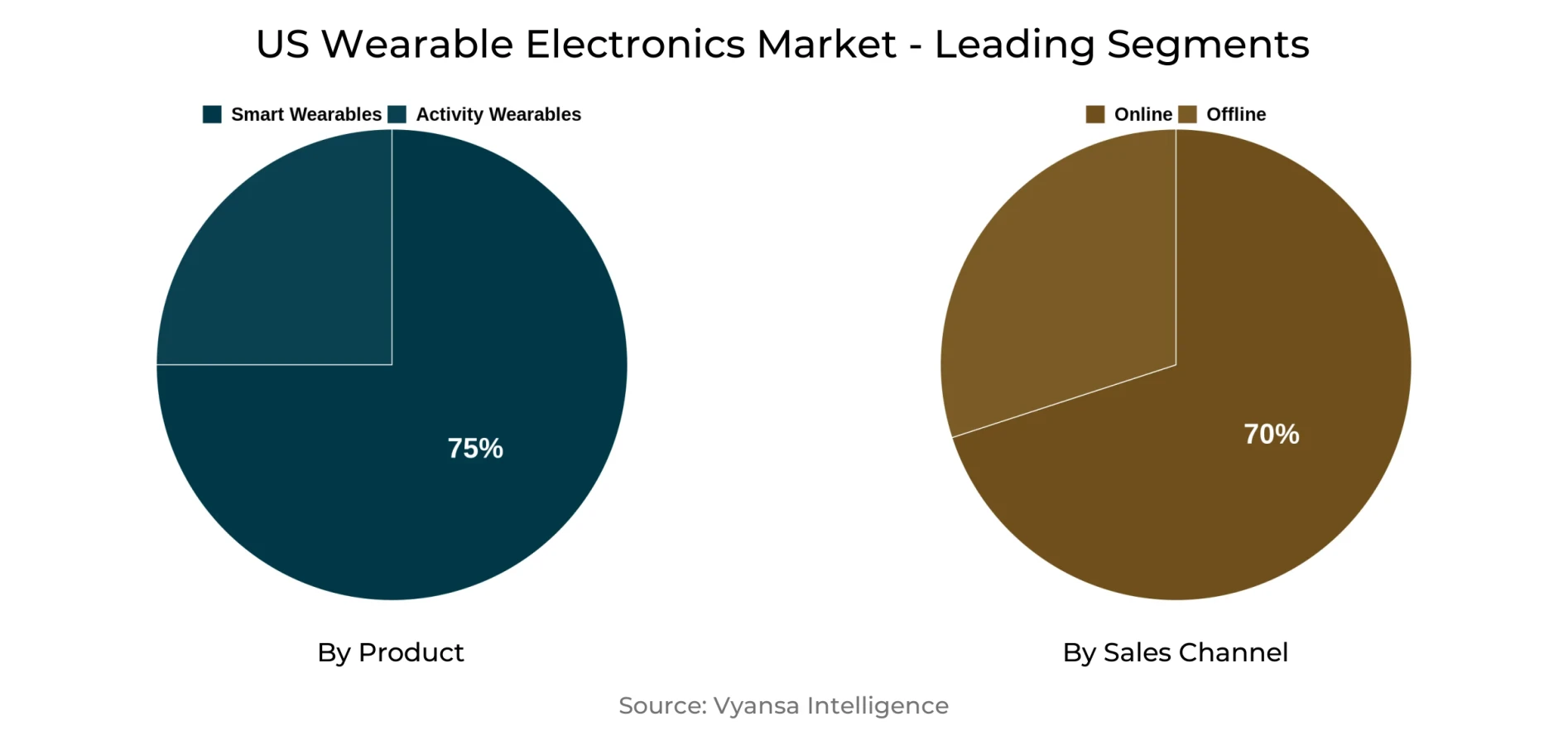

- Smart Wearables grabbed market share of 75%.

- Smart Wearables to witness a volume CAGR of around 4.47%.

- Competition

- More than 10 companies are actively engaged in producing Wearable Electronics in US.

- Top 5 companies acquired 70% of the market share.

- Huawei USA, Nike Inc, Sony Corp of America, Apple Inc, Fitbit Inc etc., are few of the top companies.

- Sales Channel or something else

- Retail E-Commerce grabbed 70% of the market.

US Wearable Electronics Market Outlook

The US wearable electronics market is poised to register steady retail volume expansion in 2025–30, thanks mainly to the sustained appeal of smart wearables. Companies like Garmin and Apple will probably maintain strong positions, with innovations such as Garmin's Venu 3 smartwatch providing inclusive functionalities like wheelchair user tracking, and Apple's growing lineup with the Apple Watch Series 10 and Ultra 3. These innovations reflect an increasing emphasis on accessibility, health monitoring, and longer battery life—attributes that will attract a wide consumer base.

While smartwatches will remain at the top in terms of volume, the emergence of smart rings will further shake up the category. Devices such as the Oura Ring are acquiring popularity with their minimalist design, sophisticated sleep and wellness monitoring, and smooth connectivity with fitness applications. Smart rings' popularity is likely to surge strongly, as these products address consumer needs for unobtrusive yet practical wearables, sucking attention away from conventional smartwatches and activity bands.

During the forecast period, advanced features like ECG-based health monitoring and safety features like crash detection will fuel smartwatch innovation. Advanced features will assist brands in keeping consumers interested with increased competition from future wearables. Though popular, smartwatches can expect only relatively modest volume growth because alternative wearables are gaining popularity.

Meanwhile, activity wearables like fitness bands and electronic activity watches are expected to fall as consumers embrace multifunction smart wearables. While analogue activity watches can hold on to a niche audience that craves minimalist designs, they will fail to counteract the general downtrend. Overall, the trend indicates a market more obsessed with smart, integrated, and lifestyle-driven wearable solutions.

US Wearable Electronics Market Challenge

The future period is expected to witness a drop in volume sales of activity bands and digital activity watches in the US. The consumer is shifting towards cheaper and more functional products like smartwatches and smart wearables like the Oura Ring. They do much more than activity tracking—they have music control, messaging notifications, and contactless payments, so they are an attractive option for consumers who want convenience and versatility in one product.

Although analogue activity watches will continue to have some demand because of their simplicity and vintage charm, their basic functionality is not going to be sufficient to offset the decline in other activity wearables. The broader trend points to an increased preference for smart wearables that offer broader utility, and this represents a major challenge to the growth of conventional activity wearables over the next few years.

US Wearable Electronics Market Trend

In spite of the surging popularity of innovative smart wearable technologies such as smart rings, smartwatches are poised to stay in the market in the years ahead. Companies are distinguishing their products actively by launching specialized features with regard to customers' increasing health and safety demands. A feature that is finding increasing popularity is ECG-based smartwatches for monitoring the heart. These devices enable individuals to monitor their heart rhythms and identify signs of potential cardiac complications early on, and take preventive measures on time to preserve their health.

In addition to health monitoring, smartwatches are also incorporating safety-focused features to make them more appealing. One such example is Apple's car accident detection feature, which applies motion sensors and connectivity features to identify accidents and automatically summon emergency services when necessary. These technologies demonstrate how smartwatches are becoming multi-purpose devices, consolidating their position in the face of growing competition from other smart wearable technology.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Wearable Electronics Market Opportunity

The increasing popularity of the Oura Ring in the US has created an opportunity for other brands of smart rings such as RingConn Smart Ring and Evie Ring to gain popularity. These products appeal to customers who like their smart devices to be sleek, subtle, and fashion-conscious compared to the larger size and calling functions of smartwatches. Their looks are appealing to customers who desire wearable technology that harmonizes with their lifestyle and fashion sense.

This change in consumer demand towards fashionable and health-oriented devices will propel demand for smart rings during 2025-30. As more people become aware of their ability to track their health and wellness, smart rings are likely to emerge as a strong contender against mainstream wearables. Their combination of fashion and functionality makes them a prime opportunity in the changing US wearable electronics market.

| Report Coverage | Details |

|---|---|

| Market Forecast | 2025-30 |

| USD Value 2024 | $ 10.94 Billion |

| USD Value 2030 | $ 12.09 Billion |

| CAGR 2025-2030 | 1.68% |

| Largest Category | Smart Wearables segment leads with 75% market share |

| Top Challenges | Declining Demand for Activity Wearables Amid Shifting Preferences |

| Top Trends | Smartwatches Carving a Niche Amid Rising Competition from Smart Rings |

| Top Opportunities | Rising Popularity of Smart Rings to Offer Disruptive Growth Potential |

| Key Players | Huawei USA, Nike Inc, Sony Corp of America, Apple Inc, Fitbit Inc, Samsung Electronics, Garmin Ltd, Fossil Group Inc, Pebble Technology Corp, AliphCom Inc and Others. |

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Wearable Electronics Market Segmentation Analysis

The largest market segment in the US Wearable Electronics Market in 2025–30 is smart wearables, led by the strong market presence of brands such as Garmin and Apple. Garmin's Venu 3 smartwatch has been at the forefront in emphasizing inclusivity, providing wheelchair-friendly features, whereas Apple keeps finding buyers with its innovative series, comprising the Apple Watch Series 10, Ultra 3, and the third-generation SE. These latest models continue to expand the limits of what is possible with smartwatches, addressing the changing demands of users with different lifestyles.

Nonetheless, while smartwatches are anticipated to increase in retail size, the rate is apt to be moderate, evidencing a shift in consumer behavior. The surging popularity of smart rings—slim, discreet, and multi-functioning—has begun to shake up the smartwatch segment. This evolving perspective speaks volumes about the challenge for companies to harmonize sophisticated innovation with accessibility, and pace with fluid consumer expectations.

Top Companies in US Wearable Electronics Market

The top companies operating in the market include Huawei USA, Nike Inc, Sony Corp of America, Apple Inc, Fitbit Inc, Samsung Electronics, Garmin Ltd, Fossil Group Inc, Pebble Technology Corp, AliphCom Inc, etc., are the top players operating in the US Wearable Electronics Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. US Wearable Electronics Market Policies, Regulations, and Standards

4. US Wearable Electronics Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. US Wearable Electronics Market Statistics, 2020-2030F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.1.2.By Unit Sold (Thousand Units)

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product

5.2.1.1. Activity Wearables- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.1. Activity Bands- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.2. Activity Watch- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.2.1. Analogue- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.2.2. Digital- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2. Smart Wearables- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.1. Eye Wear- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2.2. Body Wear- Market Insights and Forecast 2020-2030, USD Million

5.2.2.By Application

5.2.2.1. Healthcare- Market Insights and Forecast 2020-2030, USD Million

5.2.2.2. Entertainment- Market Insights and Forecast 2020-2030, USD Million

5.2.2.3. Industrial- Market Insights and Forecast 2020-2030, USD Million

5.2.2.4. Others- Market Insights and Forecast 2020-2030, USD Million

5.2.3.By Sales Channel

5.2.3.1. Offline- Market Insights and Forecast 2020-2030, USD Million

5.2.3.2. Online- Market Insights and Forecast 2020-2030, USD Million

5.2.4.By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. US Activity Wearable Electronics Market Statistics, 2020-2030F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.1.2.By Unit Sold (Thousand Units)

6.2. Market Segmentation & Growth Outlook

6.2.1.By Product- Market Insights and Forecast 2020-2030, USD Million

6.2.2.By Application- Market Insights and Forecast 2020-2030, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

7. US Smart Wear Wearable Electronics Market Statistics, 2020-2030F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.1.2.By Unit Sold (Thousand Units)

7.2. Market Segmentation & Growth Outlook

7.2.1.By Product- Market Insights and Forecast 2020-2030, USD Million

7.2.2.By Application- Market Insights and Forecast 2020-2030, USD Million

7.2.3.By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Apple Inc

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Fitbit Inc

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.Samsung Electronics America Inc

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Garmin Ltd

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Fossil Group Inc

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Huawei USA

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.Nike Inc

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Sony Corp of America

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Pebble Technology Corp

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. AliphCom Inc

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Application |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.