US Childrenswear Market Report: Trends, Growth and Forecast (2026-2032)

Product Type (Apparel (Baby and Toddler Wear, Boys Apparel, Girls Apparel), Footwear (Boys Footwear, Girls Footwear), Accessories (Boys Accessories, Girls Accessories), Others), Age Group (Infant/Toddler (Below 2 years), Kids/Children (2 - 14 years)), Price Category (Mass, Premium), Sales Channel (Retail Offline, Retail Online) ... Read more

|

Major Players

|

US Childrenswear Market Statistics and Insights, 2026

- Market Size Statistics

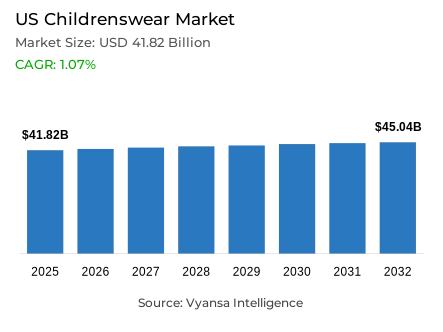

- Childrenswear in US is estimated at USD 41.82 billion in 2025.

- The market size is expected to grow to USD 45.04 billion by 2032.

- Market to register a cagr of around 1.07% during 2026-32.

- Product Type Shares

- Apparel grabbed market share of 70%.

- Competition

- More than 20 companies are actively engaged in producing childrenswear in US.

- Top 5 companies acquired around 25% of the market share.

- SHEIN Distribution Corp; Children's Place Retail Stores Inc, The; Fruit of the Loom Inc; Carter's Inc; Gap Inc etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 80% of the market.

US Childrenswear Market Outlook

The US childrenswear market was valued at USD 41.82 billion in 2025 and is expected to reach approximately USD 45.04 billion by 2032, registering a CAGR of about 1.07% during the forecast period of 2026-2032. The market has started showing signs of recovery from its inflation-induced slowing pace in 2022-2023 due to easing prices and improved end users confidence. However, demand is still not that robust due to shrinking birth rates and cautious spending among lower-income households. Whereas apparel accounts for around 70% of the total market share, its growth is stable as parents continue to purchase such wear as essential clothing for school and wear along.

Girls' apparel still leads the category, capturing the largest share of current value sales, but boys' apparel is growing at a faster rate because social media is increasingly influential in both parents' and children's fashion decisions. Parents strive for affordability without sacrificing style, which has forced brands like Carter's, Old Navy, and Walmart to keep prices low while investing heavily in omnichannel development. In a bid to balance value with convenience, many retailers have frozen prices, while some offer flexible delivery options, such as same-day fulfillment partnerships during peak seasons.

The secondhand is a key trend, as parents embrace affordable and sustainable shopping through digital channels such as ThredUp and Facebook Marketplace. In response, brands like Hanna Andersson launch resale programs that work toward circularity in fashion with end users trust because of quality assurance. This shift indicates how price-conscious parents are reshaping the childrenswear market by mixing affordability with sustainability.

Meanwhile, inclusivity and adaptability are turning out to be defining features of market innovation. Leading brands are introducing gender-neutral, size-diverse, and adaptive collections to meet the increasing diversity of children's needs. Nike's introduction of an "added width" range and unifying Kids Fit sizing further speaks to this transformation. While retail offline channels contribute about 80% of the total sales, physical stores continue to lead the way, supported by increasing e-commerce and social commerce adoption. Put together, these forces position the US childrenswear market for steady, inclusive, and value-driven growth

US Childrenswear Market Growth Driver

The stability of the market is supported both by the economic recovery and increased spending by parents.

The US childrenswear market reflects restored optimism on the back of easing inflation and increased spending by parents, reinforcing overall stability. According to the Bureau of Labor Statistics, US, inflation slipped below 3.5% at the beginning of 2024, restoring confidence among end userss and persuading families to spend more on categories such as apparel. Several middle-income families have extended their budgets for clothes, inspired by wage increase and stable employment conditions. This recovery is reflected in an upsurge in sales of both value and mid-tier childrenswear brands, reflecting improvement in the buying sentiment of parents.

According to the US Census Bureau, retail e-commerce sales were up more than 7% year-over-year in early 2024, a sign that online purchasing continues to gain momentum. This trend plays to the benefit of brands that can implement omnichannel strategies in service to parents seeking both convenience and affordability. The stable macroeconomic environment and pragmatic spending motivations, such as replacement needs, continue to support steady demand for childrenswear despite the demographic challenges.

US Childrenswear Market Challenge

Declining Birth Rate and Cost Sensitivity Will Limit Long-Term Growth

A major factor affecting the US childrenswear market is the drop in the national birth rate, which decreases the long-term potential end-user base for baby and toddler apparel. According to the Centers for Disease Control and Prevention (CDC), in 2024, the US birth rate remains below 12 per 1,000 population, one of the lowest levels on record during the past century. Although there was a slight recovery in 2021, the ongoing downward trend still holds back natural growth in many product categories.

Besides, household financial pressures remain tight, especially at lower-income levels. According to the Federal Reserve, 37% of US adults in 2024 could not afford an unexpected expense of $400, indicating continued end users budget sensitivity. This has caused families to delay or decrease purchases of childrenswear, opting for fewer but versatile and durable clothes rather than updating their wardrobes as regularly. These economic and demographic factors together temper sales growth, especially in baby and toddler categories.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Childrenswear Market Trend

Inclusion, body positivity, and gender-neutral design are redefining apparel choices

Evolving social attitudes and inclusivity are reshaping the US childrenswear market as brands adapt to the diverse needs of modern families. According to the National Institutes of Health (NIH), around 20% of US children aged 6-11 are affected by obesity, driving higher demand for flexible fits and adaptive sizing. Major brands like Nike and Carter’s have responded by introducing gender-neutral and extended-size collections that promote comfort, accessibility, and confidence among children of all body types.

This trend is further cemented through cultural awareness, where parents are more interested in brands that show diversity and corporate social responsibility. According to the Pew Research Center, 68% of parents in the US prefer companies that show ethical and inclusive branding. In response, many apparel labels now show diverse models and adaptive clothing lines, reinforcing inclusivity as a key brand value. This ongoing shift signifies a broader transformation toward apparel that celebrates individuality and reflects progressive social norms within Generation Alpha households.

US Childrenswear Market Opportunity

Second-hand retailing and circular fashion offer sustainable growth paths.

The development of more second-hand and circular fashion models in the near future also bodes well for the US childrenswear market. Parents are increasingly looking for more affordable and sustainable options, which underlines the rapid development of resale platforms like ThredUp and Facebook Marketplace. According to the US Environmental Protection Agency, the volume of textile waste reached almost 17 million tons in 2023, which has strongly heightened end users awareness about sustainability and waste reduction. This further coincides with the growing demand for used childrenswear as families balance costs with eco-consciousness.

Resale-integrated initiatives are further driving this transformation. For example, Hanna Andersson's "Hanna-Me-Downs" programme allows customers to resell used clothing through brand-supported channels, strengthening retention and brand loyalty. Indeed, the US Department of Commerce projects that second-hand fashion could represent more than 15% of total apparel sales by 2028 due to growing acceptance of circular retail models. This blending of affordability, environmental stewardship, and digital accessibility makes resale a key pillar in the future of US childrenswear.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Childrenswear Market Segmentation Analysis

By Product Type

- Apparel

- Footwear

- Accessories

- Others

The segment with highest market share under By product type, is apparel, which accounts for about 70% of the US childrenswear market. Parents are still very keen to purchase clothes for everyday use, as well as special events or occasions, especially girls' and boys' clothing. The continuous need to replace a child's wardrobe because of rapid growth further bolsters the strong and stable sales in this category.

While baby and toddler wear maintains steady demand, the apparel for older children, particularly girls, remains the core growth driver due to its association with fashion trends and social influence. Online content and social media also increasingly affect the choices made by parents in selecting clothing for their children, thus continuously pushing the sale of stylish and fashionable clothes across the country.

By Sales Channel

- Retail Offline

- Retail Online

The segment with highest market share underSales Channel is retail offline, representing nearly 80% of the US childrenswear market. Parents still do not show any signs of abandoning in-store purchases, and this is because a physical outlet lets them check the size, quality, and comfort before buying—very important factors for their kids when purchasing clothes. Retailers like Walmart, Target, and Carter's continue to benefit from this shopping behavior during back-to-school and holiday seasons.

Despite the rise of online shopping, offline channels remain critical touchpoints to drive impulse buying and special offers. Many brands are now using omnichannel marketing-blending physical retail with digital convenience-to ensure availability and remind parents of the brand while enjoying the sensory experience of in-store shopping.

List of Companies Covered in US Childrenswear Market

The companies listed below are highly influential in the US childrenswear market, with a significant market share and a strong impact on industry developments.

- SHEIN Distribution Corp

- Children's Place Retail Stores Inc, The

- Fruit of the Loom Inc

- Carter's Inc

- Gap Inc

- Walmart Inc

- Nike Inc

- Target Corp

- H&M Hennes & Mauritz (USA)

- Abercrombie & Fitch Co

Market News & Updates

- H&M, 2025:

H&M introduced its Back-to-School Kidswear collection, designed for children up to 14 years old. The collection places denim at the center of the design, featuring relaxed silhouettes with boho influences, retro varsity sport elements, and workwear-inspired styles. The lineup includes items such as wide-leg jeans, denim shirts, quilted denim jackets, fleece crewnecks, and overshirts in a palette of denim blues with neutral accents. The collection aims to combine comfort, durability, and contemporary fashion, making it suitable for everyday school wear.

- GAP Inc., 2025:

Gap Inc. announced a collaboration with New York–based designer Sandy Liang to launch a limited-edition capsule collection. The collection blends Gap’s classic American style with Liang’s playful and contemporary design aesthetic, featuring apparel for women along with coordinated mini styles for infants and toddlers. The collaboration targets modern families seeking expressive, fashion-forward everyday wear.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. US Childrenswear Market Policies, Regulations, and Standards

4. US Childrenswear Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. US Childrenswear Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Baby and Toddler Wear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Boys Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Girls Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Boys Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Girls Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Boys Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Girls Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Age Group

5.2.2.1. Infant/Toddler (Below 2 years)- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Kids/Children (2 - 14 years)- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Price Category

5.2.3.1. Mass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Sales Channel

5.2.4.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. US Apparel Childrenswear Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. US Footwear Childrenswear Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. US Accessories Childrenswear Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Carter’s Inc

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.The Gap Inc

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Walmart Inc

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Nike Inc

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Target Corp

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.SHEIN Distribution Corp

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.The Children’s Place Retail Stores Inc

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Fruit of the Loom Inc

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.H&M Hennes & Mauritz (USA)

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Abercrombie & Fitch Co

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Price Category |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.