US Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade), By Region (West, Midwest, South, North, Northeast) ... Read more

|

Major Players

|

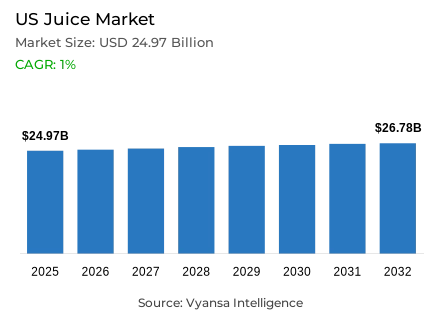

US Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in US was estimated at USD 24.97 billion in 2025.

- The market size is expected to grow to USD 26.78 billion by 2032.

- Market to register a CAGR of around 1% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 45%.

- Competition

- More than 20 companies are actively engaged in producing juice in US.

- Top 5 companies acquired around 40% of the market share.

- Vita Coco Inc, Naked Juice Co, Campbell's Co The, Coca-Cola Co The, Tropicana Products Inc etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 75% of the market.

US Juice Market Outlook

The U.S juice market is at a crossroads and is facing long-term changes in health perception and major production challenges. The market is estimated to be USD 24.97 billion in 2025 and USD 26.78 billion in 2032 with a CAGR of about 1% between 2026 and 2032. This small increase is indicative of an existential crisis of traditional juice as people are starting to perceive it as a luxury item instead of a necessity because of the high sugar content and the risk of obesity.

Federal isolationist policies and environmental issues, including the citrus greening disease in Florida, which has driven orange production to an 88-year low, have placed a lot of pressure on domestic supply chains. In the U.S. juice market, the brands are reacting by switching to juice blends, using other fruits, and offering smaller packaging sizes to deal with pricing sensitivity and lessen sticker shock among end users. Meanwhile, technological innovation, especially Artificial Intelligence, offers a lifeline. The Coca-Cola Co. and PepsiCo, the industry leaders, are using AI to predictive maintenance in their manufacturing, optimise their logistics, and use generative algorithms to simulate and test thousands of possible flavour formulations before launch.

Although the larger category is experiencing structural headwinds, coconut water and other plant-based hydration drinks are becoming vibrant growth drivers in the U.S. juice market ecosystem. With a powerful end user interest in self-optimisation and wellness, hydration has ceased to be a sports-oriented necessity and become a daily lifestyle concern. Companies such as Vita Coco are taking advantage of this trend and are marketing coconut water as a natural, low-calorie, electrolyte-rich beverage, which is effectively targeting younger audiences who are abandoning high-sugar juices in favor of functional, healthier hydration options.

Although the consumption trends have changed, the distribution environment is relatively stable throughout the U.S. juice market. The Off-Trade channel remains the dominant channel, with supermarkets as the main point of purchase because of the infrastructure that they have, the large shelf space, and the strong cold-chain facilities. Despite the rapid expansion of e-commerce, which is being fueled by omnichannel retailers like Walmart and Kroger, the expense of transporting heavy liquid goods and the logistical challenge of refrigerated delivery means that the brick-and-mortar retail will continue to play a central role in category sales in the next few years.

US Juice Market Growth Driver

Sugar Scrutiny Reshapes Beverage Choices

The health issues of sugar and weight maintenance keep the juice under the microscope, and end users prefer drinks that focus on functionality and hydration. The brands react by emphasizing no added sugar claims, but many end users continue to view juice as high-sugar and thus reduce the number of purchases. This ongoing pressure drives reformulation and portfolio choices across the category, creating a structural shift to functional and naturally positioned beverage alternatives.

This pressure is maintained at a high level by the scale of weight-related risk in the United States. According to CDC obesity maps, by 2024, all U.S. states and territories have an adult obesity prevalence of at least 25%. Once a significant percentage of adults are obese, end users and policymakers still pay attention to the amount of sugar in their diets, which supports the transition to non-traditional juice in favor of beverages that are viewed as healthier by default. This public-health setting creates structural demand headwinds to traditional juice and at the same time creates favourable conditions to low-sugar, functional, and plant-based beverage formats in line with preventive health behaviours and end user wellness priorities during the forecast period.

US Juice Market Challenge

Citrus Supply Disruptions Elevate Costs

The juice manufacturers are faced with a difficult cost environment due to disruption of citrus supply by disease, extreme weather, and tightening trade conditions. Orange scarcity makes brands turn to imports, change blend ratios, or downsize packs, but high shelf prices continue to motivate end users to switch to own-label and other drinks. Supply-chain volatility generates a long-term pricing instability that compromises promotional planning and volume-management strategies.

The Florida production statistics indicate that the category is highly vulnerable to upstream supply. According to USDA NASS, Florida all-orange production in 2024-2025 dropped 32% to 12.2 million boxes, and total citrus production dropped 28% to 14.6 million boxes. As the domestic supply is highly constrained, further cost pressures due to logistics or tariffs quickly trickle down to retail prices, constraining volume demand and making it difficult to plan on the part of manufacturers and retailers. The structural supply fragility is formed by the convergence of disease pressure, weather disruption, and trade uncertainty. To deal with the ongoing input-cost volatility in the already challenged citrus-supply environment of the U.S. juice market, manufacturers need to establish holistic sourcing diversification, blend optimisation, and pricing strategies.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Juice Market Trend

AI Enhances Operations and Product Development

The use of artificial-intelligence is permeating beverage supply chains, helping manufacturers to enhance quality management, minimize spoilage, and streamline marketing and pricing choices. The technology in juice helps to conduct product tests faster and more targeted digital campaigns, which is essential as brands are competing with functional drinks and bottled-water replacement. The capabilities of AI are shifting to competitive differentiators to operational needs in the wider beverage-manufacturing environment.

Formal business statistics show an increasing adoption trend. According to the U.S. Census Bureau, the Business Trends and Outlook Survey estimates that 5.4% of businesses are currently using AI as of February 2024. According to the same Census update, 11% of businesses with 250 or more employees and 7% of businesses with one to four employees indicate that they use AI one year later. The more companies build these capabilities, the more AI can be used as an efficient and innovative tool in packaged beverages. The Coca-Cola Co. and PepsiCo, as industry leaders, are implementing AI to predictive manufacturing maintenance and generative algorithms that can simulate thousands of new flavour formulations, creating technological leadership as a sustainable competitive advantage in the changing U.S. juice market.

US Juice Market Opportunity

Omnichannel Retail Strengthens Category Relevance

The growth of e-commerce offers juice brands a chance to seize the intended purchases via retailer websites and applications, despite the decline in traditional juice consumption by shoppers. Powerful omnichannel grocers are able to package juice with grocery baskets, implement personalised offers, and use click-and-collect to minimize last-mile breakage and cold-chain risk. Digital-commerce features allow brands to stay visible to end users and compete with other functional beverages based on specific promotional tactics and demand-forecast accuracy.

Online shopping is growing in magnitude. According to the U.S. Census Bureau, retail e-commerce sales in the third quarter of 2025 were 16.4% of total retail sales. With the increasing number of end users moving their spending online, juice players can respond by focusing on ship-friendly packages, shelf-stable formats, and multipacks that can be picked up and delivered. This strategy retains brand presence with functional waters and ready-to-drink tea and enhances margins by providing better promotion targeting and demand-forecasting. The omnichannel opportunity allows brands to access digitally active end users via platforms facilitated by omnichannel giants, such as Walmart and Kroger, which build all-encompassing distribution ecosystems that support a variety of purchasing behaviours.

Unlock Market Intelligence

Explore the market potential with our data-driven report

US Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment that has the largest share in the category division is 100% Juice, which has a market share of 45%. Although this segment has been able to retain category leadership, it is experiencing a declining volume trend as end users grow cautious about naturally occurring fructose and perceived health links. Manufacturers react by abandoning the perception of ultra-processed and actively promoting the message of no added sugar to fit the modern wellness trend, rebranding 100% juice as a naturally wholesome and not a sugary beverage option.

This 45% portion is further split into the old favourites and new functional blends. Although orange juice is still a staple of the segment, its leadership is threatened by supply shortages and increasing prices. In reaction, the segment is developing into hybrid drinks that combine 100% fruit juice with botanicals, probiotics, and adaptogens. This strategic shift is to regain younger, health-conscious end users who appreciate the natural nutritional value of fruit but need functional advantages to back up value creation in the face of volume pressure by charging a premium price based on scientifically supported health positioning.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The most significant segment in the sales-channel division is the Off-Trade, which has 75% of the total market sales. The dominance of this channel is fuelled by regional supermarket giants and hypermarkets that contribute a significant value of retail in the industry. These stores are specially designed to handle the logistical challenges of the juice category, such as the high weight of the product and the cold-chain conditions of the high-end, unpasteurised, and fresh-squeezed products. Physical retail infrastructure establishes the necessary distribution bases that cannot be easily duplicated by digital channels.

The 75% market share of the off-trade segment is further supported by the increasing private-label products by the retailers such as Costco and Trader Joe’s, which are able to shift the volume away of the branded players. Although third-party delivery apps like Instacart and DoorDash are introducing channel dynamism, they are not supplanting physical retail primacy, but rather complementing it. With the shift of juice to the higher-priced positioning, the physical retail space is the critical platform of product discovery and impulse buying. The integration of developed cold-chain infrastructure, competition on its own label, and integration of digital channels forms a complete off-trade ecosystem that facilitates various juice purchase occasions within the U.S. end user environment.

List of Companies Covered in US Juice Market

The companies listed below are highly influential in the US juice market, with a significant market share and a strong impact on industry developments.

- Vita Coco Inc

- Naked Juice Co

- Campbell's Co The

- Coca-Cola Co The

- Tropicana Products Inc

- Ocean Spray Cranberries Inc

- Kraft Heinz Co

- Keurig Dr Pepper Inc

- Florida's Natural Growers

- Bai Brands LLC

Competitive Landscape

US juice market is led by The Coca-Cola Co, whose Simply and Minute Maid brands anchor 100% juice and juice drinks, leveraging scale, distribution strength and portfolio breadth to offset category decline, although private label competition is intensifying amid price sensitivity. PepsiCo remains a secondary force through diversified beverage exposure rather than pure juice momentum. Vita Coco is the standout growth player, dominating coconut and plant waters by positioning around natural hydration, electrolytes and low calories, supported by innovation (sparkling, flavoured variants) and strategic backing from Keurig Dr Pepper. Private label players such as Costco, Kroger and Trader Joe’s are gaining share on value. Key differentiation opportunities lie in hybrid functional formulations, premium unpasteurised blends, and AI-enabled supply chain and flavour innovation to counter sugar stigma and input volatility.

Market News & Updates

- PepsiCo, 2025:

PepsiCo completed the acquisition of prebiotic soda brand Poppi for approximately USD 1.95 billion, marking a strategic expansion into the fast-growing functional beverage segment. This move reflects a broader shift among U.S. beverage companies away from traditional high-sugar juice products toward health-oriented and gut-health-focused drinks, aligning with evolving consumer preferences for low-calorie and functional beverages.

- Odwalla, 2025:

Backed by Grupo Jumex, Odwalla relaunched its product portfolio in the U.S. with a new lineup of smoothies (Mango, Strawberry-Banana, and Berries) and juices (Orange-Guava-Ginger, Green Juice, and Orange Juice). The beverages are made with real fruit, no added sugar, and natural ingredients, and are available in glass bottles and Tetra Prisma cartons, targeting health-conscious consumers seeking fresh and clean-label options.

- Suja Organic, 2024:

Suja Organic expanded beyond cold-pressed juices with the launch of ready-to-drink protein shakes, featuring 16g of plant-based protein (pea, rice, and hemp), essential vitamins and minerals, and acacia fiber. The 200-calorie beverages, made with almond milk and coconut cream, mark the brand’s entry into the fast-growing functional and protein beverage segment.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- US Juice Market Policies, Regulations, and Standards

- US Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- US Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Region

- West

- Midwest

- South

- North

- Northeast

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- US 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- US Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- US Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- US Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- US Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Coca-Cola Co The

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tropicana Products Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ocean Spray Cranberries Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kraft Heinz Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Keurig Dr Pepper Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vita Coco Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Naked Juice Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Campbell's Co The

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Florida's Natural Growers

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bai Brands LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coca-Cola Co The

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.