UK Pet Care Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Pet Food (Dry Food, Wet Food, Treats & Mixers), Pet Products (Cat Litter, Pet Healthcare (Veterinary Diets, Probiotics and Supplements, Tele-health Services)), Services (Veterinary Clinics, Pet Insurance, Boarding, Day-Care, and Training), Grooming and Hygiene (Shampoos and Conditioners, Brushes and Combs, Clippers and Scissors)), By Pet Type (Dog, Cat, Others), By Sales Channel (Retail Offline, Retail E-Commerce, Veterinary Clinics) ... Read more

|

Major Players

|

UK Pet Care Market Statistics and Insights, 2026

- Market Size Statistics

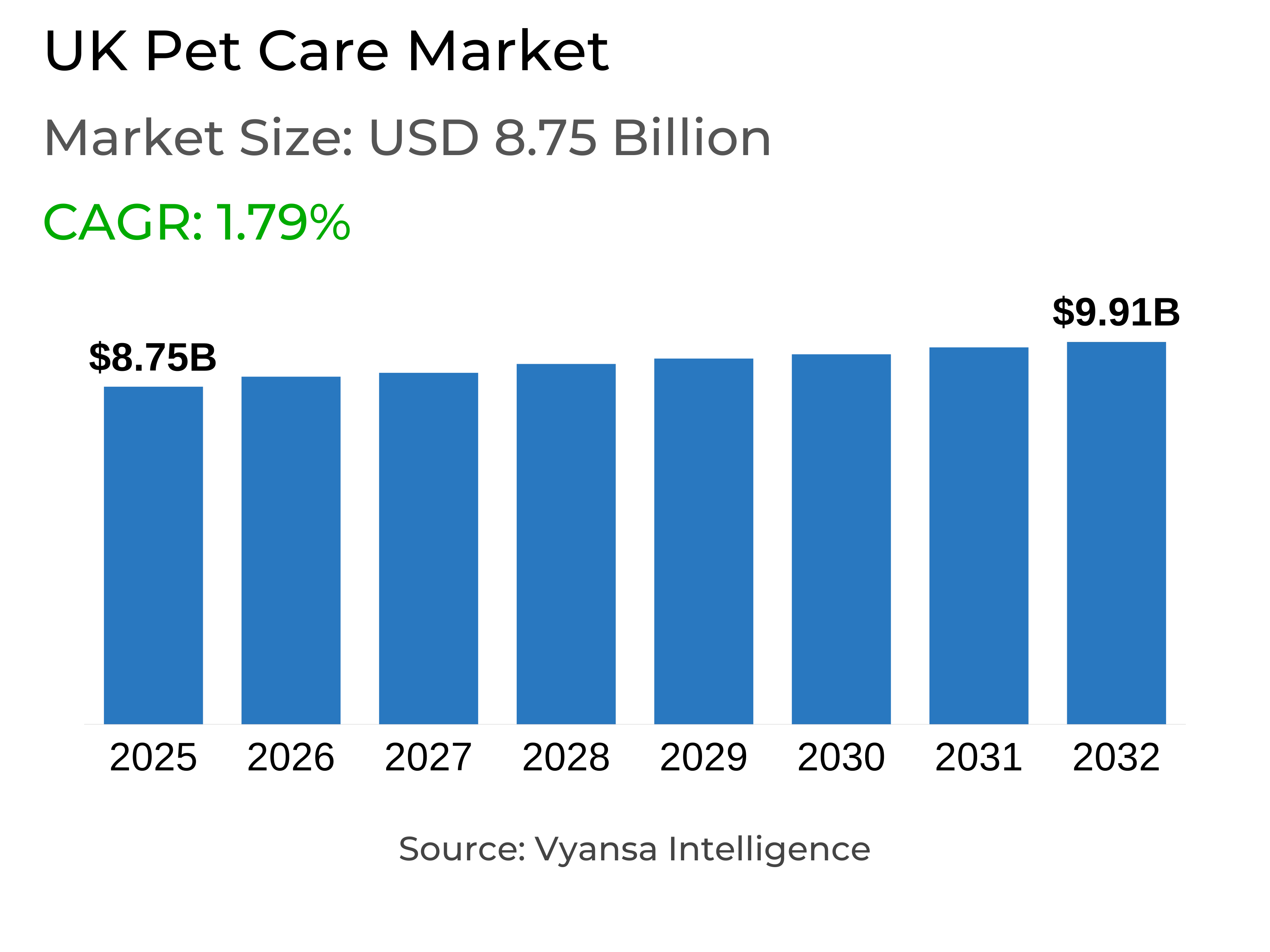

- Pet Care in UK is estimated at $ 8.75 Billion.

- The market size is expected to grow to $ 9.91 Billion by 2032.

- Market to register a CAGR of around 1.79% during 2026-32.

- Product Shares

- Pet Food grabbed market share of 75%.

- Pet Food to witness a volume CAGR of around 0.53%.

- Competition

- More than 20 companies are actively engaged in producing Pet Care in UK.

- Top 5 companies acquired 60% of the market share.

- MPM Products Ltd, Tesco Plc, Inspired Pet Nutrition Ltd, Nestlé Purina Ltd, Mars Petcare UK Ltd etc., are few of the top companies.

- Sales Channel

- Retail Offline grabbed 60% of the market.

UK Pet Care Market Outlook

UK pet care market, which stands at approximately USD 8.75 billion today, is expected to grow to USD 9.91 billion by 2032. Growth will be consistent with robust trends in premiumisation and humanisation as end users continue to splurge on high-quality products for their pets. While spending has eased because of earlier inflationary pressures, consumer interest in pet wellbeing guarantees stable demand, especially in the dog and cat food segments.

Pet food will continue to be the market driver, with volume CAGR of approximately 0.53%. High-quality dog and cat food and functional treats will lead value growth as owners become more inclined to buy healthier and sustainable products. Fresh food innovations, supplementation, toppings, and cultivated or plant-based alternatives will increase their share, indicating a trend towards nutrition, sustainability, and ethics.

Retail channels will also impact market performance. retail Offline trends to account for approximately 60% of sales, backed by supermarkets, hypermarkets, and specialist pet stores, which remain vital for in-person experiences like grooming and veterinary guidance. Yet, trends to grow rapidly in Retail E-commerce will be fueled by convenience, subscription models, and digital interaction. Omnichannel approaches, such as app-based buying and rapid delivery partnerships, will close gaps between online and offline experiences.

Forward, pet population stability, especially dogs and cats, will be the foundation of future value growth. Millennials will remain a significant consumer group and demonstrate increased readiness to spend on health-driven and premium products. Sustainability, innovation, and tailored pet care solutions will continue to sit at the core of development, making the UK pet care market endure stable progress up to

UK Pet Care Market Growth Driver

Increased Interest in Pet Health and Wellbeing Among Millennials

Millennials are on track to become the leading consumer demographic in the pet care market, and their high interest in the health and wellbeing of animals is leading to growth in the market. This age group indicates a higher inclination to spend on premium, high-end products that guarantee improved nutrition and overall treatment for their pets. The fact that they prefer health-oriented products leads brands to adapt their approach to premiumisation to ensure products appeal to this change in demand.

Private label and economy brands are suffering at the same time. Price reductions no longer guarantee consumer loyalty because most millennials are willing to trade up for quality. This trend indicates a sharp change in which quality supersedes quantity, thus reinforcing the status of millennials as a propeller of the expanding premium segment within the pet care market.

UK Pet Care Market Trend

Innovation Fuelling Pet Care Growth

Innovation is transforming the UK pet care market, with a keen emphasis on health, sustainability, and overall well-being of pets. With eco-packaging going mainstream, the transition shifts towards sustainable and eco-packaging ingredients. Advances like cultivated pet meat, such as Meatly's cultivated chicken chews for canines, make the way for kinder and greener food options. Plant-based substitutes, such as HOWND Superfood, also find attention, indicating growing interest in diversified protein sources.

Meanwhile, businesses continue to spend on product extension to address specialized requirements. These include functional treats, nutritional supplements, and toppers that help promote pet health and wellbeing. These advances show just how innovation continues to play the key role in propelling growth, as well as enhancing customer loyalty through new offerings that resonate with changing consumer value

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Pet Care Market Opportunity

Broadening of Retail Retail E-commerce Channels

Retail E-commerce is expected to be a big opportunity for the pet care market because convenience, competitive prices, and product assortment will continue to pull End users in. Top sites such as Amazon will take advantage of their capacity to provide a large assortment of goods, especially heavy ones, and facilitate price comparisons. Pet retailers will amplify their online presence by means of omnichannel strategies, like Pets at Home's enhanced app, which will serve to integrate online and offline purchasing seamlessly. Subscription services will also feed into this growth by offering end users with routine deliveries of necessary products, with social media facilitating sales, particularly for the younger clientele.

Concurrently, there will be opportunities for retailers to marry online and offline strengths. Pets at Home's concept stores will offer retail, grooming, and vet services, making them a single-stop shop. Food retailers, like Tesco, will grow premium ranges and modify store formats, mirroring increasing demand for higher-quality products and driving growth in both Retail E-commerce and Retail offline channels.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Pet Care Market Segmentation Analysis

By Product

- Pet Food

- Pet Products

- Services

- Grooming and Hygiene

The most dominant segment under the product category is pet food, taking close to 75% of the UK Pet Care Market. This is due to increasing consumer emphasis on quality, health, and premiumisation, as dog and cat owners increasingly consider pets part of their family. This has driven demand for functional health products, premium wet food, and human-grade-inspired innovative treats.

In the future, cat food will be the most dynamic subcategory, while innovation in health-oriented products keeps dog food ticking. Changes in consumer consciousness towards nutrition are fueling demand for fresh, wet, and mixed feeding forms, while mid-tier options experience strain. Regardless of these changes, the overall pet food market will continue to grow steadily, posting a volume CAGR of approximately 0.53% over the forecast period.

Top Companies in UK Pet Care Market

The top companies operating in the market include MPM Products Ltd, Tesco Plc, Inspired Pet Nutrition Ltd, Nestlé Purina Ltd, Mars Petcare UK Ltd, Crown Pet Foods Ltd, Spectrum Brands (UK) Ltd, Hill's Pet Nutrition Ltd, J Sainsbury Plc, Butcher's Pet Care Ltd, etc., are the top players operating in the UK Pet Care Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. UK Pet Care Market Policies, Regulations, and Standards

4. UK Pet Care Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. UK Pet Care Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product

5.2.1.1. Pet Food- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Dry Food- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Wet Food- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Treats & Mixers- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Pet Products- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Cat Litter- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Pet Healthcare- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.1. Veterinary Diets- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.2. Probiotics and Supplements- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.3. Tele-health Services- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Services- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Veterinary Clinics- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Pet Insurance- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Boarding, Day-Care, and Training- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Grooming and Hygiene- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4.1. Shampoos and Conditioners- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4.2. Brushes and Combs- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4.3. Clippers and Scissors- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Pet Type

5.2.2.1. Dog- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Cat- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Sales Channel

5.2.3.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Retail E-Commerce- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Veterinary Clinics- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. UK Pet Food Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.1.2.By Quantity Sold in Kilo Tons

6.2. Market Segmentation & Growth Outlook

6.2.1.By Product- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Pet Type- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. UK Pet Product Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Product- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Pet Type- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. UK Pet Care Service Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Services- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Pet Type- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. UK Grooming and Hygiene Pet Care Market Statistics, 2022-2032F

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in US$ Million

9.2. Market Segmentation & Growth Outlook

9.2.1.By Product- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Pet Type- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Competitive Outlook

10.1. Company Profiles

10.1.1. Nestlé Purina Ltd

10.1.1.1. Business Description

10.1.1.2. Product Portfolio

10.1.1.3. Collaborations & Alliances

10.1.1.4. Recent Developments

10.1.1.5. Financial Details

10.1.1.6. Others

10.1.2. Mars Petcare UK Ltd

10.1.2.1. Business Description

10.1.2.2. Product Portfolio

10.1.2.3. Collaborations & Alliances

10.1.2.4. Recent Developments

10.1.2.5. Financial Details

10.1.2.6. Others

10.1.3. Crown Pet Foods Ltd

10.1.3.1. Business Description

10.1.3.2. Product Portfolio

10.1.3.3. Collaborations & Alliances

10.1.3.4. Recent Developments

10.1.3.5. Financial Details

10.1.3.6. Others

10.1.4. Spectrum Brands (UK) Ltd

10.1.4.1. Business Description

10.1.4.2. Product Portfolio

10.1.4.3. Collaborations & Alliances

10.1.4.4. Recent Developments

10.1.4.5. Financial Details

10.1.4.6. Others

10.1.5. Tesco Plc

10.1.5.1. Business Description

10.1.5.2. Product Portfolio

10.1.5.3. Collaborations & Alliances

10.1.5.4. Recent Developments

10.1.5.5. Financial Details

10.1.5.6. Others

10.1.6. Hill's Pet Nutrition Ltd

10.1.6.1. Business Description

10.1.6.2. Product Portfolio

10.1.6.3. Collaborations & Alliances

10.1.6.4. Recent Developments

10.1.6.5. Financial Details

10.1.6.6. Others

10.1.7. MPM Products Ltd

10.1.7.1. Business Description

10.1.7.2. Product Portfolio

10.1.7.3. Collaborations & Alliances

10.1.7.4. Recent Developments

10.1.7.5. Financial Details

10.1.7.6. Others

10.1.8. Inspired Pet Nutrition Ltd

10.1.8.1. Business Description

10.1.8.2. Product Portfolio

10.1.8.3. Collaborations & Alliances

10.1.8.4. Recent Developments

10.1.8.5. Financial Details

10.1.8.6. Others

10.1.9. J Sainsbury Plc

10.1.9.1. Business Description

10.1.9.2. Product Portfolio

10.1.9.3. Collaborations & Alliances

10.1.9.4. Recent Developments

10.1.9.5. Financial Details

10.1.9.6. Others

10.1.10. Pets at Home Plc

10.1.10.1.Business Description

10.1.10.2.Product Portfolio

10.1.10.3.Collaborations & Alliances

10.1.10.4.Recent Developments

10.1.10.5.Financial Details

10.1.10.6.Others

11. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Pet Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.