UK Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade), By Region (England, Wales, Scotland, Northern Ireland) ... Read more

|

Major Players

|

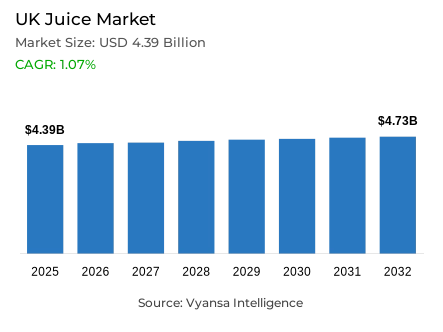

UK Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in UK was estimated at USD 4.39 billion in 2025.

- The market size is expected to grow to USD 4.73 billion by 2032.

- Market to register a CAGR of around 1.07% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 60%.

- Competition

- More than 20 companies are actively engaged in producing juice in UK.

- Top 5 companies acquired around 35% of the market share.

- J Sainsbury Plc, Asda Group Ltd, Lucozade Ribena Suntory Ltd, Innocent Drinks Co Ltd, Tesco Plc etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 85% of the market.

UK Juice Market Outlook

The UK juice market is in the midst of a strategic repositioning phase as the industry is being redefined by increasing production costs and health conscious end user trends. The market is projected to reach USD 4.39 billion in 2025 and USD 4.73 billion in 2032 with a CAGR of about 1.07% in the 2026-32 period. Although inflation has increased retail prices, making juice a luxury many households can only afford on weekends, value growth is maintained through a transition to higher-end, nutrient-dense innovations like juice shots and cold-pressed blends.

The main drivers of the forecast period are health and functionality. end users are also shifting towards low-sugar products and towards vegetable juices and functional shots that focus on immunity, energy, and gut health. Plenish and Moju are among the brands that are taking the lead in this direction with superfood-enhanced products with ginger, turmeric, and camu berry. Moreover, the future advertising ban on less healthy products in 2026 is making giants like Tropicana and Innocent speed up sugar cuts and increase their Fresh and Light or functional protein brands.

End user trust is also becoming dependent on sustainability and ingredient transparency. The emergence of clean-labeled products and cold-pressed items that use excess produce and little processing attracts eco-friendly end users. Also, the sector is experiencing a surge in wellness-based collections, with AG Barr acquiring The Turmeric Co. Aggressive digital marketing and influencer-led campaigns that target younger, trend-driven audiences on platforms like TikTok support this trend.

Although the volume sales might be under pressure because of price sensitivity, the Off-Trade channel still prevails. Hypermarkets and supermarkets are the key points of sale, as they can use meal offers and increased shelf space on functional juice drinks to make impulse purchases. In the meantime, retail e-commerce is becoming a vibrant growth driver, with subscription options and the availability of niche health products that appeal to the contemporary, convenience-driven British end user.

UK Juice Market Growth DriverFunctional Wellness Drives Premium Innovation

The UK juice brands are still forced to update recipes and formats due to health-and-wellness priorities. According to the Office for Health Improvement and Disparities, in England, it is estimated that 64.5% of adults will be overweight or living with obesity in the period 2023-2024, and 26.5% will be living with obesity. This health context reinforces the need to have products that seem lighter, less sugar, and more purpose-based, including immunity and energy blends that explicitly communicate functional value.

In response, brands invest in functional juice shots and fortified blends with more than orange and apple to control costs. The trend to vegetable bases, ginger, turmeric, and other functional ingredients follows the end user search of nutrient-rich products, and the plant waters are framed by the hydration and low-sugar attributes. Innovation thus helps in the growth of retail values even when the shoppers buy less juice. Functional positioning allows brands to support high prices with proven health advantages, establishing defensible market positions in the UK health-conscious, price-sensitive beverage market, which is defined by increasing end user sophistication in terms of nutritional assertions.

UK Juice Market ChallengeFood Inflation Reduces Purchase Frequency

The main threat that limits volume performance in the UK juice category is price pressure. According to the Office for National Statistics, the prices of food and non-alcoholic drinks increased 4.5% during the year ending in December 2025. With the cost of basic needs still high, end users cut back on non-essential purchases and grow more discriminating of more expensive beverages, repositioning juice as a luxury, not a daily necessity, in many households.

This dynamic is reflected in a reduction in the number of purchase occasions and a change to weekend-only consumption of juice, especially of the more expensive 100% juice formats. The cost of inputs is increasing and producers are transferring the costs to end users, pushing them to consume less expensive soft drinks or lighter forms of juice. At the same time, the issues of sugar content also give additional reasons to decrease the frequency of purchases, which makes the volume protection by promotional strategies alone more and more inadequate. Cost inflation poses two problems: rising production prices and falling end user purchasing power. This continued pressure requires strategic responses in terms of format innovation, ingredient differentiation and value communication that proves clear functional advantages to justify higher prices in limited household budgets.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Juice Market TrendOnline Retail and Digital Campaigns Gain Importance

The UK, juice is finding a new path to purchase and product discovery through digital engagement. According to the Office for National Statistics, the value of online sales increased by 11.1% in December 2025 relative to December 2024, and the share of all retail sales made online was 28.3% in December 2025. This fast digital adoption shows how fast shoppers switch between mobile browsing and home delivery making e-commerce a mainstream and not a supplementary channel.

This channel shift facilitates the emergence of niche functional products like juice shots, plant waters, and clean-label blends, which have the advantage of targeted digital marketing. Social media, influencers, and retail media are used by the brands to create awareness and trial, and online grocery and specialist platforms are used to make new launches reach health-conscious end user segments. Single-serve formats also expand in vending, which supports convenience-driven purchasing and e-commerce platforms. The digital trend is a paradigm shift in end user-brand interaction, with content-based discovery, personalised targeting, and purchase integration being the key elements. The strong digital performance and the network of influencers put brands in a strategic position to attract health-conscious end users via platforms like Tik Tok in the UK digitally developed retail landscape.

UK Juice Market OpportunityLow-Sugar Reformulation Gains Regulatory Advantage

Stricter nutrition marketing policy opens up significant opportunities to brands that reformulate and communicate health credentials effectively. The UK government guidance confirms that the Advertising Less-Healthy Food Definitions and Exemptions Regulations 2024, which will come into force on 5 January 2026, will restrict paid advertising of identifiable less-healthy products online and restrict television placement before the watershed. This regulation enhances the commercial worth of products that do not fit the less-healthy definition, which provides competitive advantages to compliant formulations.

At the same time, end users are still struggling to achieve healthy diet goals. According to the Office for Health Improvement and Disparities, in England, 2023-2024, just 31.3% of adults indicate that they consume at least five portions of fruit and vegetables each day. The juice manufacturers that create low-sugar, vegetable-based, and clean-label blends with clear front-of-pack labels are in a better position to gain shelf space and online presence under more stringent regulations. The regulatory opportunity allows the brands to balance commercial goals with policy compliance, attracting end user groups that actively pursue healthier choices promoted by the government. Compliance early investment creates defensible market positions and marketing flexibility that less-healthy competitors do not have.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment that controls the largest portion of the category division is 100% Juice which has a market share of 60%. This segment is the industry backbone even though it experiences the highest volume losses owing to the high prices of raw materials to produce orange and apple crops. Its large portion is maintained by its long-standing connections with breakfast traditions and a natural product image that many end users still prefer to highly processed substitutes. The leadership of 100% juice categories is supported by cultural and habitual consumption patterns despite the presence of major economic headwinds.

In order to defend this 60% market share, the dominant brands are shifting towards functional premiumisation. Instead of price wars, other players like Innocent and Tropicana are launching fortified 100% juices and mini packs with portions that are health conscious. The 100% juice category is effectively re-connecting with wellness-conscious end users who are more interested in nutritional content than the quantity of juice. Premiumisation strategy allows protection of revenue in the face of volume loss, category value by increased per-unit pricing backed by plausible functional positioning and sourcing of premium ingredients.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment that dominates the largest portion of the sales channel division is the Off-Trade, which controls 85% of the total market sales. This hegemony is supported by supermarkets and hypermarkets that offer the cold-chain infrastructure that is required by the ever-growing cold-pressed and functional categories. These retailers have been able to strategically increase shelf space on on-the-go formats and functional shots, which allow brands like Vita Coco and Moju to access wider audiences with high-visibility chillers and promotional meal deals. Physical retail infrastructure establishes the necessary distribution base of both mass-market and high-end juice segments.

In addition to the conventional aisles, the off-trade market is supported by the fast retail e-commerce and specialised vending development. Online stores like Ocado have become crucial in introducing niche innovations, and subscription services enable health-conscious end users to have functional juices delivered to their homes. The off-trade channel has preserved its 85% market share by adapting to the bifurcated demand of both value-based and premium wellness products by combining the massive physical store reach with online shopping convenience. This physical-digital model allows full coverage of end users, as it allows both impulse buying with high-footfall retail formats and premeditated, subscription-based buying with digital platforms.

List of Companies Covered in UK Juice Market

The companies listed below are highly influential in the UK juice market, with a significant market share and a strong impact on industry developments.

- J Sainsbury Plc

- Asda Group Ltd

- Lucozade Ribena Suntory Ltd

- Innocent Drinks Co Ltd

- Tesco Plc

- Tropicana UK Ltd

- Coca-Cola Enterprises Ltd

- Britvic Soft Drinks Ltd

- Naked Juice Co

- Euro Food Brands Ltd

Competitive Landscape

UK juice market is led by Innocent Drinks, positioned around clean-label smoothies and health-led propositions, while Tropicana is the most dynamic large player, defending relevance via portfolio rationalisation and targeted innovation (Fresh & Light, Mini Packs, Naked Protein, Naked Fire, Sparkling Cans). High-growth challengers cluster in functionality: Vita Coco dominates coconut water with low-sugar hydration cues and multipacks, Moju leads juice shots with immunity messaging and heavy digital spend, and Plenish competes with plant-based detox and balance shots; The Turmeric Co (now backed by AG Barr) signals mainstream capital flowing into wellness. Private label competes on price but lacks differentiation. Key opportunities are credible sugar reduction, nutrient-dense vegetable blends, clearer compliance-ready labelling ahead of Jan 2026 ad restrictions, and scalable omnichannel execution across supermarkets, e-commerce, and vending.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- UK Juice Market Policies, Regulations, and Standards

- UK Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- UK Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Region

- England

- Wales

- Scotland

- Northern Ireland

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- UK 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UK Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Innocent Drinks Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tropicana UK Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tesco Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coca-Cola Enterprises Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Britvic Soft Drinks Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- J Sainsbury Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Asda Group Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lucozade Ribena Suntory Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Naked Juice Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Euro Food Brands Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Innocent Drinks Co Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.