UK Field Service Management Market Report: Trends, Growth and Forecast (2026-2032)

By Component (Solution, Services, Others), By Deployment Mode (Cloud, On-Premises, Hybrid), By Enterprise Size (Large Enterprises, Small and Medium Enterprises, Others), By Industry Vertical (IT & Telecom, Utilities, Healthcare, Construction, Manufacturing, Transportation & Logistics, Retail, Oil & Gas, Others) ... Read more

|

Major Players

|

UK Field Service Management Market Statistics and Insights, 2026

- Market Size Statistics

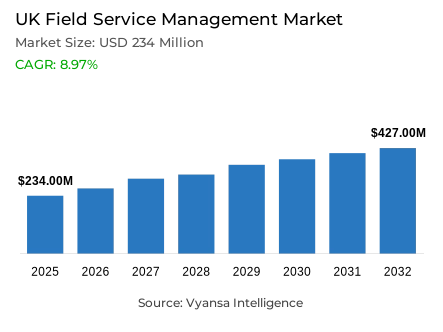

- Field service management market size in UK was valued at USD 234 million in 2025 and is estimated at USD 262 million in 2026.

- The market size is expected to grow to USD 427 million by 2032.

- Market to register a CAGR of around 8.97% during 2026-32.

- Component Shares

- Solution grabbed market share of 65%.

- Competition

- More than 10 companies are actively engaged in producing field service management in UK.

- Top 5 companies acquired around 30% of the market share in 2026.

- Oracle Corporation UK Ltd (Oracle Fusion Field Service), SAP SE (SAP Field Service Management), PTC Inc. (ServiceMax), Salesforce UK Limited, Microsoft Corporation (Dynamics 365 Field Service) etc., are few of the top companies.

- Deployment Mode

- Cloud grabbed 70% of the market.

UK Field Service Management Market Outlook

The UK field service management market is expanding as utilities, telecom providers, facilities operators, healthcare equipment firms, HVAC contractors, and industrial service teams need tighter control over work orders, dispatching, routes, parts, assets, mobile technicians, and customer updates. The market size was valued at USD 234 million in 2025 and is projected to grow from USD 262 million in 2026 to USD 427 million by 2032, registering a CAGR of 8.97% during the forecast period.

Solution holds the leading 65% share because buyers need a daily operating platform, not only implementation support. Microsoft says Dynamics 365 Field Service supports work orders, technician mobile guidance, Copilot work-order summaries, asset management, customer equipment tracking, and service history. ServiceNow also highlights automated work planning and dispatch, matching jobs to the right technician, tools, and parts. This explains why UK field service software captures the largest value pool: dispatchers and technicians use the platform daily to coordinate jobs, routes, assets, skills, parts, and customer records.

Cloud holds 70% share because field work happens across offices, vans, customer sites, substations, exchanges, hospitals, factories, and facilities, where live access matters more than local server ownership. ONS reported that 69% of UK firms used cloud-based computing systems and applications in 2023, while 61% used specialised software. This directly supports the UK FSM market, because cloud field service management combines remote access with specialist workflow control for scheduling, dispatch, mobile forms, contractor visibility, CRM, ERP, and asset-system integration.

Country demand is supported by field-service intensity, not only digital readiness. Ofgem states that ED3 will run from 1 April 2028 to 31 March 2033 for electricity distribution networks, creating a longer cycle of network investment, reinforcement, maintenance, and contractor coordination. Ofcom’s Connected Nations 2025 reports gigabit-capable broadband availability at 87% of UK residential premises and full fibre availability at 78%, expanding the installed telecom base that needs surveys, installs, repairs, and service assurance.

UK Field Service Management Market Growth Driver

Technician Coordination Pressure Accelerates Workflow Digitization

Technician coordination pressure is the core driver because UK service work is distributed across customer homes, business sites, utility assets, telecom cabinets, healthcare equipment, factories, and managed facilities. ONS reported 69% cloud adoption and 61% specialised software adoption among UK firms in 2023, proving that the digital base is already in place. The demand now is for platforms that convert digital readiness into service efficiency, including work order management, dispatch boards, technician scheduling, route optimization, spare-parts visibility, SLA tracking, and customer communication.

Direct product evidence strengthens the driver. Microsoft’s Dynamics 365 Field Service includes mobile technician guidance, schedule changes, service work, asset management, and Copilot summaries, while Salesforce describes field service platforms as combining scheduling, dispatching, mobile tools, and automation to improve frontline field work. These functions address the exact coordination problem faced by service teams: assigning the right technician to the right job with the right information before arrival. Better technician scheduling software improves first-time fix rate, dispatcher productivity, route discipline, and service accountability.

UK Field Service Management Market Challenge

Legacy Integration and Field Adoption Slow Automation Gains

Legacy integration and field adoption are the main barriers because FSM fails when companies digitize weak processes instead of redesigning them. ONS found that the most common barriers to AI adoption among UK firms were difficulty identifying activities or business use cases at 39%, cost at 21%, and AI expertise or skills at 16%. For field operations, the implication is direct: scheduling automation cannot work properly if asset records, technician skill profiles, parts catalogues, customer histories, contract rules, and SLA definitions are incomplete.

Labor conditions reinforce the barrier because successful deployment depends on trained dispatchers, supervisors, technicians, administrators, and integration teams. ONS estimated that UK vacancies decreased to 705,000 in February to April 2026, but this still represents a large hiring and capability base that employers must manage carefully. If technicians resist mobile field service apps or dispatchers continue parallel spreadsheets, platform value falls. Vendors must therefore support offline access, simple user interfaces, ERP and CRM integration, contractor portals, clean master data, and change management.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Field Service Management Market Trend

AI Scheduling and Predictive Service Move Beyond Job Tracking

AI-powered field service is moving FSM beyond job tracking into next-best-action support. UK government research found that, among businesses handling digital data, 72% analyse the data they work with either internally or externally. This matters because field service platforms depend on operational data streams such as asset condition, repair history, technician location, parts usage, route timing, customer complaints, and SLA breaches. Once analysed, this data can support predictive maintenance, appointment prioritization, technician matching, required-parts suggestions, and proactive customer updates.

AI adoption remains early but is expanding. ONS reported that 9% of UK firms had adopted AI in 2023 and projected adoption at 22% in 2024. Product development already reflects this shift: Microsoft provides Copilot work-order summaries in Dynamics 365 Field Service, while ServiceNow uses AI to generate insights, summaries, and notes for technicians. The market direction is clear: connected field service platforms are becoming intelligent workflow engines that improve remote diagnostics, reduce repeat visits, and help technicians arrive better prepared.

UK Field Service Management Market Opportunity

Utilities and Fibre Rollout Open High-Value Expansion

Utilities create the strongest opportunity because they combine regulated assets, emergency response, inspection cycles, contractor oversight, safety workflows, and customer communication. Ofgem states that ED3 is the next price control for Britain’s electricity distribution networks, running from 2028 to 2033, and its framework is designed around growing electricity demand and network investment requirements. This supports UK utilities field service, where operators need work orders, mobile safety forms, route planning, asset updates, outage records, and auditable proof of work across distributed field crews.

Telecom adds a second high-value vertical because fibre rollout creates installation, repair, activation, survey, and maintenance workloads. Ofcom reports that gigabit-capable networks reached 87% of UK residential premises and full fibre reached 78% in Connected Nations 2025. These figures signal a larger installed base that requires ongoing UK telecom field service, including appointment management, contractor dispatch, premises visits, cabinet work, route optimization, customer updates, and digital closeouts. FSM tools become commercially important when telecom providers must control service workflow automation across national field territories.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UK Field Service Management Market Segmentation Analysis

By Component

- Solution

- Services

- Others

The segment with the highest share under Component is Solution, holding around 65% of the market. This leadership reflects the platform-led nature of field operations. Buyers need field service software that controls work order intake, scheduling, dispatch management software, technician mobility, route planning, asset records, customer communication, inventory visibility, SLA tracking, and analytics. The 65% share is commercially meaningful because solutions are used every day by dispatchers, technicians, supervisors, and service operations teams, while professional services mainly support configuration, integration, training, and adoption.

Direct product evidence supports this dominance. Salesforce defines work order management as the structured process of creating, assigning, tracking, and completing field service requests, while Microsoft identifies work orders, scheduling, dispatch, mobile guidance, customer asset history, and Copilot summaries inside Dynamics 365 Field Service. ServiceNow adds technician matching, parts matching, mobile guidance, and AI-generated insights. These functions explain why solutions capture the largest value: productivity gains come from daily workflow control across jobs, assets, crews, customers, and performance metrics.

By Deployment Mode

- Cloud

- On-Premises

- Hybrid

The segment with the highest share under Deployment Mode is Cloud, holding around 70% of the market. This lead is practical because field technicians need live schedules, asset records, safety forms, inventory data, service history, customer notes, maps, and job updates while working away from offices. Cloud field service management lets dispatchers, supervisors, contractors, technicians, and customers work from one shared service record while jobs change during the day. It also supports multi-branch service networks through faster configuration, centralized visibility, and remote workforce management.

UK technology data supports this deployment pattern. ONS reported that cloud-based computing systems and applications were adopted by 69% of UK firms in 2023, making cloud the most widely adopted technology in its survey. Direct FSM product evidence shows why cloud is useful in the field: Oracle Field Service allows mobile workers to access routes, activities, inventory, communications, and offline synchronization when connectivity is unavailable. This supports SaaS field service software, mobile FSM platforms, and real-time tracking across distributed UK service operations.

List of Companies Covered in UK Field Service Management Market

The companies listed below are highly influential in the UK field service management market, with a significant market share and a strong impact on industry developments.

- Oracle Corporation UK Ltd (Oracle Fusion Field Service)

- SAP SE (SAP Field Service Management)

- PTC Inc. (ServiceMax)

- Salesforce UK Limited

- Microsoft Corporation (Dynamics 365 Field Service)

- Industrial and Financial Systems (IFS Cloud Field Service Management)

- TotalMobile Limited

- ServiceNow Inc.

- Tracer Management Systems Limited (Joblogic)

- BigChange Group Limited (BigChange)

Market News & Updates

- ServiceNow, 2026:

ServiceNow updated Field Service Management under its Australia release. The release includes field service manager mobile capabilities, scheduling and dispatch improvements, appointment booking updates, capacity management enhancements, and AI-powered workflow features. The update adds new operational tools for field service teams using ServiceNow FSM.

- Microsoft Corporation, 2026:

Microsoft published the Dynamics 365 Field Service 2026 release wave 1 plan. The release covers new Field Service capabilities scheduled from April 2026 to September 2026. The update adds planned product enhancements for field service operations, scheduling, service execution, and connected field workflows

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- The UK Field Service Management Market Policies, Regulations, and Standards

- The UK Field Service Management Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- The UK Field Service Management Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component

- Solution- Market Insights and Forecast 2022-2032, USD Million

- Services- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode

- Cloud- Market Insights and Forecast 2022-2032, USD Million

- On-Premises- Market Insights and Forecast 2022-2032, USD Million

- Hybrid- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size

- Large Enterprises- Market Insights and Forecast 2022-2032, USD Million

- Small and Medium Enterprises- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Industry Vertical

- IT & Telecom- Market Insights and Forecast 2022-2032, USD Million

- Utilities- Market Insights and Forecast 2022-2032, USD Million

- Healthcare- Market Insights and Forecast 2022-2032, USD Million

- Construction- Market Insights and Forecast 2022-2032, USD Million

- Manufacturing- Market Insights and Forecast 2022-2032, USD Million

- Transportation & Logistics- Market Insights and Forecast 2022-2032, USD Million

- Retail- Market Insights and Forecast 2022-2032, USD Million

- Oil & Gas- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Component

- Market Size & Growth Outlook

- The UK Solution Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By Industry Vertical- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The UK Services Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By Enterprise Size- Market Insights and Forecast 2022-2032, USD Million

- By Industry Vertical- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Salesforce UK Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Microsoft Corporation (Dynamics 365 Field Service)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Industrial and Financial Systems, IFS Aktiebolag (IFS Cloud Field Service Management)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TotalMobile Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ServiceNow, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Oracle Corporation UK Ltd (Oracle Fusion Field Service)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SAP SE (SAP Field Service Management)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PTC Inc. (ServiceMax)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tracer Management Systems Limited (Joblogic)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BigChange Group Limited (BigChange)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Salesforce UK Limited

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Component |

|

| By Deployment Mode |

|

| By Enterprise Size |

|

| By Industry Vertical |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.