India Semiconductor Manufacturing Equipment Market Report: Trends, Growth and Forecast (2026-2032)

By Equipment Type (Wafer Fabrication Equipment (Lithography Equipment, Etching Equipment, Deposition & Epitaxy Equipment, Metrology, Inspection & Process Control Equipment, Others), Assembly & Packaging Equipment (Dicing & Singulation Equipment, Die Bonding Equipment, Wire Bonding & Flip-Chip Bonding Equipment, Molding, Encapsulation & Advanced Packaging Equipment, Others), Semiconductor Test Equipment (Wafer Probing Equipment, Automated Test Equipment, Burn-in & Reliability Test Equipment, Final Test & System-Level Test Equipment, Others)), By Wafer Size (300 mm, 200 mm, 150 mm, Others), By Technology Node (Leading-Edge Nodes (≤5 nm), Advanced Nodes (>5 nm to 14 nm), Mature Nodes (>14 nm to 90 nm), Legacy Nodes (>90 nm), Others), By Semiconductor Device Type (Logic & Micro component Devices, Memory Devices, Analog & Mixed-Signal ICs, Discrete, Power & Optoelectronic Devices, MEMS & Sensor Devices, Others), By End User (Foundries, Integrated Device Manufacturers, OSAT Companies, Research Institutes & Universities, Others), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Semiconductor Manufacturing Equipment Market Overview

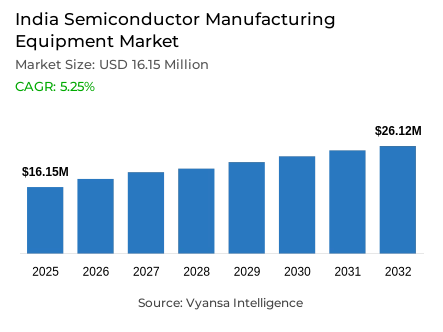

Semiconductor manufacturing equipment includes wafer fabrication tools, assembly and packaging systems, and semiconductor test equipment used to process wafers, form chips, package devices, inspect defects, and validate performance before commercial shipment. The industry in India is projected to expand at a CAGR of 5.25% during 2026-2032 as domestic semiconductor projects move from policy approval toward fabrication, OSAT, ATMP, compound semiconductor, and advanced packaging execution.

Key Highlights of the India Semiconductor Manufacturing Equipment Market

- India semiconductor manufacturing equipment market stood at USD 16.15 Million in 2025 and reached USD 19.21 Million in 2026, with value expected to reach USD 26.12 Million by 2032.

- The market is forecast to grow at a 5.25% CAGR during 2026-2032.

- Based on equipment type, assembly & packaging equipment leads the industry with 38% share in 2026.

- However, Wafer Fabrication Equipment is the fastest-growing equipment type, expanding at a 11.70% CAGR during 2026-2032.

- By end user, OSAT Companies lead the market with 37% share in 2026.

- Meanwhile, Foundries are the fastest-growing end-user segment, with a 11.58% CAGR during 2026-2032.

- Top-five company share is 62%, indicating that the industry remains consolidated around global wafer fab, packaging, inspection, and test equipment suppliers.

The market is gaining commercial significance as India moves from semiconductor design strength toward physical chip manufacturing capability. Equipment demand is linked to fab construction, ATMP lines, OSAT plants, compound semiconductor facilities, and semiconductor test capacity. Consequently, tools for lithography, etching, deposition, metrology, dicing, die bonding, wire bonding, molding, wafer probing, and final test are becoming critical for production readiness across India’s emerging semiconductor ecosystem.

Government policy provides the strongest structural support. PIB reported in 2026 that 12 semiconductor manufacturing projects had been approved with an investment pipeline of about ₹1.64 lakh crore, including one semiconductor fabrication unit, two compound semiconductor fabrication units, and nine packaging units. This directly supports demand for assembly equipment, packaging tools, process control systems, and wafer fabrication equipment.

Meanwhile, production-linked project execution is widening the installed base for equipment suppliers. PIB stated that Tata Electronics’ Gujarat fab has a planned capacity of around 50,000 wafer starts per month, while Tata Electronics’ Assam facility will use indigenous semiconductor packaging technologies with a capacity of 48 million units per day. These capacities strengthen demand for wafer tools, advanced packaging equipment, inspection systems, and test platforms.

Overall, the semiconductor manufacturing equipment industry in India is transitioning from a project-driven investment phase to a long-term capacity expansion cycle. Government-backed fabrication and packaging projects are establishing the country's manufacturing foundation, creating sustained demand for wafer processing, assembly, packaging, inspection, and testing equipment. As semiconductor production scales, equipment suppliers with strong local technical support, process expertise, and comprehensive lifecycle services will be best positioned to capitalize on India's evolving semiconductor manufacturing ecosystem.

India Semiconductor Manufacturing Equipment Market: Surveys and Key Insights

PIB reported that India’s semiconductor ecosystem had 12 approved projects with a cumulative investment of about USD 17.3 billion by 2026. These include one semiconductor fab, two compound semiconductor fabs, and nine packaging units, showing that the equipment opportunity is currently concentrated around OSAT, ATMP, compound semiconductors, and advanced packaging, while wafer fabrication demand expands as front-end projects mature.

PIB stated that the Electronics Component Manufacturing Scheme received 249 applications for components, base materials, and capital equipment such as PCBs, capacitors, and laminates. This matters for semiconductor equipment demand because capital equipment policy support strengthens domestic supply-chain localization, ancillary equipment procurement, component readiness, and supplier participation around cleanrooms, substrates, materials, and semiconductor manufacturing support infrastructure.

Government Policies Supporting Semiconductor Equipment Adoption

India’s semiconductor equipment demand is shaped by the Semicon India Programme, India Semiconductor Mission, and India Semiconductor Mission 2.0. PIB stated that the earlier mission used an incentive framework of USD 8.03 billion, offering fiscal support of up to 50% for silicon fabs, compound semiconductor facilities, assembly and testing units, and chip design. This improves project viability and strengthens supplier qualification for capital-intensive equipment procurement.

Meanwhile, ISM 2.0, announced in the Union Budget 2026-27 focuses on semiconductor equipment, materials, indigenous IP, and resilient supply chains. This policy direction is commercially important because equipment vendors need local application support, spare availability, process know-how, and India-based engineering relationships. Consequently, companies with global tool portfolios, local technical teams, and ecosystem partnerships are better positioned than suppliers relying only on remote sales coverage.

India Semiconductor Manufacturing Equipment Market Drivers

OSAT and ATMP Capacity Creation Driving Equipment Procurement

The India semiconductor manufacturing equipment Industry is primarily driven by the rapid expansion of OSAT and ATMP capacity, which is increasing demand for dicing systems, die bonding equipment, wire bonding equipment, flip-chip bonders, molding tools, encapsulation systems, inspection equipment, and semiconductor test platforms. OSAT operators require reliable, high-throughput equipment to convert semiconductor wafers into packaged devices efficiently. As a result, demand extends beyond initial equipment procurement to include process optimization, spare parts, consumables, maintenance, qualification services, and future capacity expansions.

PIB’s project data shows how this driver converts into demand. Tata Electronics’ Assam packaging facility targets 48 million units per day, CG Power’s facility targets around 15.07 million units per day, and Kaynes’ facility targets more than 6.33 million chips per day. These approved capacities directly require assembly, packaging, inspection, probing, burn-in, reliability test, and final-test equipment across high-volume OSAT and ATMP operations.

Limitations

High Capital Cost, Service Dependence, and Process Qualification Complexity

The significant limitation in the semiconductor manufacturing equipment market in India is high equipment cost and dependence on vendor-led process qualification. Semiconductor manufacturing tools require cleanroom-compatible installation, calibration, process recipes, uptime support, spare parts, trained engineers, and validation with customer wafers or packages. However, India’s ecosystem is still developing around fabs, OSAT lines, compound semiconductor facilities, and materials suppliers, which raises commissioning risk for operators that need production-grade yield before ramping commercial output.

This limitation is visible in India’s early-stage project base. PIB reported that 10 semiconductor units were under construction in April 2026, while commercial production had started from two plants, and two more were expected to begin production during the year. Early construction-stage activity increases equipment scheduling, installation, service, and qualification pressure because tools must be synchronized with cleanrooms, utilities, materials, and customer qualification timelines.

Recent Trends

OSAT-Led Equipment Demand Moves Ahead of Full Fab Scale

A major trend in the India semiconductor manufacturing equipment market is that assembly, packaging, and test equipment demand is moving faster than broad front-end wafer fabrication equipment procurement. This happens because India’s approved project mix includes several OSAT, ATMP, packaging, and compound semiconductor facilities. Meanwhile, front-end fabs require longer cleanroom construction, technology transfer, process integration, and equipment qualification. As a result, packaging-related tools currently provide the strongest near-term route for equipment deployment.

PIB reported that the latest approved projects include Suchi Semicon’s OSAT facility in Surat, Gujarat, with proposed capacity of 1,033.20 million chips per annum, targeting power electronics, analog ICs, industrial systems, automotive, industrial automation, and consumer electronics. This validates a stronger demand for dicing, die attach, bonding, molding, inspection, and final-test tools serving discrete and analog packaging lines.

Front-End Equipment Partnerships Strengthen India’s Wafer Fab Readiness

The technical trend is the build-out of wafer-fabrication equipment partnerships around lithography, deposition, etch, inspection, and metrology. India’s first commercial wafer fab requires front-end equipment infrastructure, trained process engineers, supplier support, and technology transfer. Consequently, global equipment companies are aligning with Indian fab sponsors through partnerships, development centres, service capability, and collaborative engineering, rather than treating India only as a downstream electronics manufacturing base.

ASML and Tata Electronics announced in 2026 that ASML will support Tata Electronics’ upcoming 300 mm semiconductor fab in Dholera, Gujarat with its suite of lithography tools and solutions. Similarly, Tokyo Electron and Tata Electronics signed a 2024 MoU to accelerate equipment infrastructure for Tata’s Dholera fab and Assam assembly-test facility. These partnerships strengthen wafer-fab readiness and local technical capability.

Future Opportunities

Local Service, Spares, Training, and Equipment Ecosystem Development

The strongest opportunity lies in local service ecosystems around installed semiconductor tools. Fab and OSAT operators require application engineers, calibration teams, spare parts, software support, field service, process recipes, training, and uptime assurance. As India moves from project approval into production, equipment vendors can build recurring revenue through service contracts, tool upgrades, preventive maintenance, process support, and operator training across fab, packaging, and test lines.

The opportunity is reinforced by ISM 2.0’s focus on semiconductor equipment, materials, indigenous IP, and resilient supply chains. PIB also reported that 13 MoUs were signed during SEMICON India 2025, which shows international confidence in India’s semiconductor policy framework. Equipment suppliers can capture this opportunity through India-based engineering centres, local service hubs, university partnerships, and supply-chain localization around emerging chip manufacturing clusters, thereby opening new doors for India semiconductor manufacturing equipment market.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Semiconductor Manufacturing Equipment Market Segmentation Analysis

By Equipment Type

- Wafer Fabrication Equipment

- Lithography Equipment

- Etching Equipment

- Deposition & Epitaxy Equipment

- Metrology, Inspection & Process Control Equipment

- Others

- Assembly & Packaging Equipment

- Dicing & Singulation Equipment

- Die Bonding Equipment

- Wire Bonding & Flip-Chip Bonding Equipment

- Molding, Encapsulation & Advanced Packaging Equipment

- Others

- Semiconductor Test Equipment

- Wafer Probing Equipment

- Automated Test Equipment

- Burn-in & Reliability Test Equipment

- Final Test & System-Level Test Equipment

- Others

Assembly & Packaging Equipment Leads, While Wafer Fabrication Equipment Accelerates

Assembly & Packaging Equipment leads the equipment type segment in India semiconductor manufacturing equipment industry with 38% share in 2026 because India’s near-term semiconductor manufacturing activity is concentrated around OSAT, ATMP, packaging, and discrete semiconductor facilities. These projects require dicing, singulation, die bonding, wire bonding, flip-chip bonding, molding, encapsulation, and advanced packaging systems. Operator preference is supported by faster line installation, lower complexity than front-end fabs, and direct connection with approved packaging capacities.

Meanwhile, Wafer Fabrication Equipment is the fastest-growing equipment type, expanding at a 11.70% CAGR during 2026-2032. Growth is supported by India’s transition from assembly-led manufacturing toward front-end wafer processing. Compared with packaging tools, wafer fabrication equipment requires higher capital intensity, cleaner process control, and deeper technology transfer. However, Tata’s planned 50,000 WSPM Dholera fab strengthens long-term demand for lithography, etching, deposition, metrology, and process-control equipment.

By End User

- Foundries

- Integrated Device Manufacturers

- OSAT Companies

- Research Institutes & Universities

- Others

OSAT Companies Lead, While Foundries Gain from Front-End Investment

OSAT Companies lead the end-user segment in India semiconductor manufacturing equipment industry with 37% share in 2026 because India’s approved semiconductor projects are currently weighted toward assembly, testing, packaging, and chip finishing. OSAT users require equipment that supports dicing, bonding, molding, inspection, reliability testing, and final test at commercial throughput. Their leadership is also supported by shorter deployment timelines compared with front-end fabs and stronger alignment with India’s initial packaging-led manufacturing ramp.

Meanwhile, Foundries are the fastest-growing end users, expanding at a 11.58% CAGR during 2026-2032. Growth is supported by India’s emerging wafer fabrication capability, particularly Tata Electronics’ Dholera fab. Compared with OSAT companies, foundries require broader front-end toolchains, including lithography systems, etch tools, deposition equipment, epitaxy systems, metrology platforms, and process control solutions. This makes foundries a smaller but strategically faster-growing demand base for high-value equipment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Semiconductor Manufacturing Equipment Market Competitive Landscape

The semiconductor manufacturing equipment industry in India is consolidated, with the top five companies accounting for 62% share in 2026. Competition is led by global semiconductor equipment suppliers with deep technology portfolios, process expertise, installed-base relationships, and application support capability. Competitive strength depends on lithography leadership, deposition and etch depth, inspection and metrology accuracy, packaging equipment coverage, field service, software support, spares availability, local engineering centres, and ability to support India’s transition from OSAT-led operations toward wafer fabrication.

Key Companies in the India Semiconductor Manufacturing Equipment Market

- ASML Holding N.V.

- Applied Materials India Private Limited

- Lam Research (India) Private Limited

- Tokyo Electron India Pvt. Ltd.

- KLA-Tencor Software India Private Limited

- ASMPT India Private Limited

- Advantest India Private Limited

- Teradyne, Inc.

- Hitachi High-Tech India Private Limited

- DISCO HI-TEC (INDIA) PRIVATE LIMITED

Company Profiling

The profiles below assess equipment portfolios, India presence, technology capability, service support, semiconductor project relevance, and competitive positioning across India’s emerging manufacturing ecosystem.

ASML Holding N.V.

ASML Holding N.V. is a Netherlands-headquartered semiconductor equipment company best known for lithography systems used by chipmakers to pattern silicon wafers. Its relevant portfolio includes EUV lithography, DUV lithography, metrology and inspection systems, computational lithography, and customer support. ASML’s 2026 partnership with Tata Electronics will support the ramp-up of Tata’s upcoming 300 mm Dholera fab. This positions ASML as a lithography-led technology supplier for India’s front-end wafer fabrication roadmap.

Applied Materials India Private Limited

Applied Materials India Private Limited is part of Applied Materials, a global semiconductor and display equipment supplier. The company states that Applied Materials India is a strategic partner and enabler of India’s semiconductor, display, and solar manufacturing ecosystems. Its wider equipment role covers materials engineering used to modify materials at atomic levels and industrial scale. The company’s planned collaborative engineering centre in Bengaluru strengthens local ecosystem participation, positioning it as a materials-engineering and process-equipment participant.

Lam Research (India) Private Limited

Lam Research (India) Private Limited is part of Lam Research, a global wafer fabrication equipment company. Lam states that its product portfolio covers thin-film deposition, plasma etch, photoresist strip, and wafer cleaning, which are complementary processing steps used throughout semiconductor manufacturing. Lam Research India has operated in Bengaluru since 2000, supporting the semiconductor innovation cycle. This positions the company as an etch, deposition, clean, and process-support supplier for India’s emerging fab ecosystem.

Tokyo Electron India Pvt. Ltd.

Tokyo Electron India Pvt. Ltd. is the India entity of Tokyo Electron, a global semiconductor production equipment supplier. TEL’s official India location page lists Tokyo Electron India Pvt. Ltd. in New Delhi and identifies its business as marketing in India. In 2025, TEL also announced a new Bengaluru development site for software development, equipment design, simulation, and collaboration with Indian universities. This positions TEL as an equipment infrastructure and development partner for India’s semiconductor ramp.

KLA-Tencor Software India Private Limited

KLA-Tencor Software India Private Limited is part of KLA, a global process control and yield management equipment supplier. KLA’s product portfolio covers inspection, metrology, and data analytics systems that help manufacturers manage yield across IC fabrication. In 2026, KLA opened a more than 300,000 sq. ft. R&D and Innovation Hub in Chennai, supporting AI, software development, engineering, and product support for up to 1,300 employees. This positions KLA as a process-control and metrology specialist.

Recent Developments and Updates

- In May 2026, ASML and Tata Electronics signed an MoU to advance India’s semiconductor manufacturing ecosystem. ASML will support Tata Electronics’ upcoming 300 mm Dholera fab with lithography tools and solutions, strengthening India’s front-end wafer fabrication readiness and local equipment infrastructure.

- In February 2026, KLA announced the opening of its Chennai R&D and Innovation Hub. The facility covers more than 300,000 sq. ft. and supports up to 1,300 employees, strengthening local AI, software, engineering, product support, and process-control capability for semiconductor equipment operations in India.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Semiconductor Production Equipment Market Policies, Regulations, and Standards

- India Semiconductor Production Equipment Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Semiconductor Production Equipment Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Equipment Type

- Wafer Fabrication Equipment- Market Insights and Forecast 2022-2032, USD Million

- Lithography Equipment- Market Insights and Forecast 2022-2032, USD Million

- Etching Equipment- Market Insights and Forecast 2022-2032, USD Million

- Deposition & Epitaxy Equipment- Market Insights and Forecast 2022-2032, USD Million

- Metrology, Inspection & Process Control Equipment- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Assembly & Packaging Equipment- Market Insights and Forecast 2022-2032, USD Million

- Dicing & Singulation Equipment- Market Insights and Forecast 2022-2032, USD Million

- Die Bonding Equipment- Market Insights and Forecast 2022-2032, USD Million

- Wire Bonding & Flip-Chip Bonding Equipment- Market Insights and Forecast 2022-2032, USD Million

- Molding, Encapsulation & Advanced Packaging Equipment- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Semiconductor Test Equipment- Market Insights and Forecast 2022-2032, USD Million

- Wafer Probing Equipment- Market Insights and Forecast 2022-2032, USD Million

- Automated Test Equipment- Market Insights and Forecast 2022-2032, USD Million

- Burn-in & Reliability Test Equipment- Market Insights and Forecast 2022-2032, USD Million

- Final Test & System-Level Test Equipment- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Wafer Fabrication Equipment- Market Insights and Forecast 2022-2032, USD Million

- By Wafer Size

- 300 mm- Market Insights and Forecast 2022-2032, USD Million

- 200 mm- Market Insights and Forecast 2022-2032, USD Million

- 150 mm- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Technology Node

- Leading-Edge Nodes (≤5 nm)- Market Insights and Forecast 2022-2032, USD Million

- Advanced Nodes (>5 nm to 14 nm)- Market Insights and Forecast 2022-2032, USD Million

- Mature Nodes (>14 nm to 90 nm)- Market Insights and Forecast 2022-2032, USD Million

- Legacy Nodes (>90 nm)- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Semiconductor Device Type

- Logic & Micro component Devices- Market Insights and Forecast 2022-2032, USD Million

- Memory Devices- Market Insights and Forecast 2022-2032, USD Million

- Analog & Mixed-Signal ICs- Market Insights and Forecast 2022-2032, USD Million

- Discrete, Power & Optoelectronic Devices- Market Insights and Forecast 2022-2032, USD Million

- MEMS & Sensor Devices- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Foundries- Market Insights and Forecast 2022-2032, USD Million

- Integrated Device Manufacturers- Market Insights and Forecast 2022-2032, USD Million

- OSAT Companies- Market Insights and Forecast 2022-2032, USD Million

- Research Institutes & Universities- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- East- Market Insights and Forecast 2022-2032, USD Million

- West- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Equipment Type

- Market Size & Growth Outlook

- India Wafer Fabrication Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Wafer Size- Market Insights and Forecast 2022-2032, USD Million

- By Technology Node- Market Insights and Forecast 2022-2032, USD Million

- By Semiconductor Device Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Assembly & Packaging Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Wafer Size- Market Insights and Forecast 2022-2032, USD Million

- By Technology Node- Market Insights and Forecast 2022-2032, USD Million

- By Semiconductor Device Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Semiconductor Test Equipment Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Wafer Size- Market Insights and Forecast 2022-2032, USD Million

- By Technology Node- Market Insights and Forecast 2022-2032, USD Million

- By Semiconductor Device Type- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- ASML Holding N.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Applied Materials India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lam Research (India) Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tokyo Electron India Pvt. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- KLA-Tencor Software India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ASMPT India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Advantest India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Teradyne, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hitachi High-Tech India Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DISCO HI-TEC (INDIA) PRIVATE LIMITED

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ASML Holding N.V.

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Equipment Type |

|

| By Wafer Size |

|

| By Technology Node |

|

| By Semiconductor Device Type |

|

| By End User |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.