UAE Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade), By Region (Dubai, Abu Dhabi, Sharjah, Northern Emirates) ... Read more

|

Major Players

|

UAE Juice Market Statistics and Insights, 2026

- Market Size Statistics

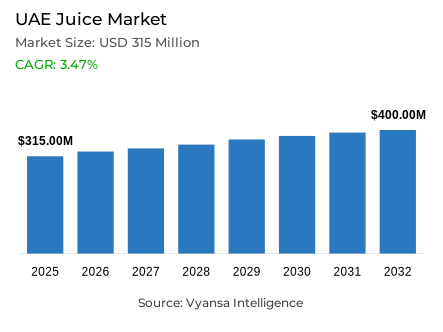

- Juice market size in UAE was estimated at USD 315 million in 2025.

- The market size is expected to grow to USD 400 million by 2032.

- Market to register a CAGR of around 3.47% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 60%.

- Competition

- More than 20 companies are actively engaged in producing juice in UAE.

- Top 5 companies acquired around 55% of the market share.

- Aujan Coca-Cola Beverages Co, Marmum Dairy Farm LLC, Capri Sun Group Holding AG, Al Rawabi Co, Almarai Co Ltd etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 80% of the market.

UAE Juice Market Outlook

The UAE juice market is experiencing a gradual change, which is caused by the increasing population and a substantial change towards high-end and health-conscious products. The market is estimated to be USD 315 million in 2025 and USD 400 million in 2032 with a CAGR of about 3.47% in the 2026-32 period. This expansion is further driven by a health-first attitude, with end users shifting off high-sugar nectars to 100% natural varieties and functional products with Vitamin C added.

Local sourcing and innovation are emerging as essential pillars to the market players. To counter the disruptions in global supply-chains and the increasing prices of raw-materials, local conglomerates like Al Rawabi are concentrating on local ingredients to enhance their juice products. In the meantime, hypermarkets such as Carrefour and Lulu are still popular with their low-cost freshly squeezed juices due to direct cooperation with Egyptian and Moroccan fruit suppliers. This plan enables them to avoid high domestic procurement prices and offer fresh and high quality products at competitive prices.

Technology is also significant in transforming end user engagement. Brands are no longer just launching products but going digital-first and smart packaging that adds to the overall experience of the juice. An example is the recent introduction of a children line by Rubicon Arabia, which is dedicated to e-commerce, and the introduction of interactive QR-coded packaging with mini-games and AR by Gulf Union Foods. These digital solutions allow the brands to gather real-time information about end user preferences and introduce a new dimension of novelty to the drinking experience.

The distribution environment is varied, but the Off-Trade channel remains dominant. Supermarkets continue to be the biggest family grocery shopping destination, although e-commerce has become the fastest-growing sales driver. The emergence of fast-commerce applications like Noon Minutes and Talabat has made the process of buying juice more accessible than ever, which is why the category continues to play a significant role in the everyday life of the UAE residents.

UAE Juice Market Growth DriverPopulation Growth and Health Awareness Drive Premium Juice Demand

The UAE juice market is still enjoying consistent growth in volume due to the direct proportional growth in population which directly contributes to increased household consumption. According to the Federal Competitiveness and Statistics Centre, the population stood at 11.35 million in 2024, which means that the population continues to grow, which is why the demand in the everyday grocery categories, such as juice, remains. The growing number of expatriates and urban living patterns also support frequent shopping via supermarkets and convenience stores.

At the same time, the increased health awareness pushes consumers to 100% juice and natural versions. According to the UAE Ministry of Health and Prevention, over 66 percent of adults are overweight or obese, which highlights the prevalence of health issues. This tendency supports an increasing popularity of the products that are promoted as natural, free of added sugar, and rich in vitamin C instead of low-juice beverages, which strengthens the premiumisation of the category.

UAE Juice Market ChallengeImport Dependency and Rising Input Costs Pressure Margins

The UAE juice market is faced with structural cost pressure due to high dependency on imported raw materials. According to the World Bank, over 90% of the food consumption requirements in the country are met by imports, which makes the market susceptible to international price fluctuations and logistical shocks. This reliance increases the exposure to transportation risks and currency risks, particularly with regard to imported fruits in Africa and other areas.

Cost pressure is also increased by global food price dynamics. In 2024, the FAO Food Price Index was 118.5 points on average, which means that the prices of agricultural products remain volatile. High raw-material and freight prices limit the flexibility of pricing by juice manufacturers, and consumers are picky and price sensitive. This mix limits growth in low-juice-based categories and narrows profit margins on brands that compete on both health positioning and affordability.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Juice Market TrendDigital Engagement and Smart Packaging Reshape Brand Interaction

Digital technology is becoming a part of the UAE juice category in terms of product launches and packaging. To enhance consumer interaction, brands are embracing digitally released product lines and interactive smart packaging. This is in line with the overall digital ecosystem of the UAE, with the internet penetration of the population standing at 99% according to the International Telecommunication Union in 2024. The high connectivity enables quick adoption of QR based campaigns and integration of e-commerce.

Beverage accessibility is also enhanced by e-commerce penetration. According to the UAE Telecommunications and Digital Government Regulatory Authority, online retail transactions are growing, with smartphone penetration being over 96 percent. This degree of digital maturity allows brands to obtain real-time consumer data through interactive packaging and online sales channels. As a result, technology transforms juice into a more experience-driven category, which is supported by data analytics and targeted promotions.

UAE Juice Market OpportunityLocal Sourcing and Hypermarket Fresh Counters Strengthen Value Proposition

Local sourcing is a strategic opportunity, with producers being less vulnerable to import volatility and meeting consumer demands of freshness. The UAE Ministry of Climate Change and Environment reports that local agricultural output is growing as part of food-security programs, thus contributing to the growth of local fruit supply. The reinforcement of regional sourcing increases cost predictability and brand communication focusing on freshness and sustainability.

Value creation is also supported by affordable, freshly squeezed products in hypermarkets. Large retailers are growing in-store juice preparation models that mix imported and locally sourced fruit to control expenses. In the Global Food Security Index 2024, the UAE was the top-ranked country in the Middle East in food security, which underscored the infrastructural preparedness to enable diversified supply chains. Firms that combine local sourcing and premium 100% juice positioning can defend margins and maintain affordability in a competitive retail environment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment commanding the highest share within the category division is Juice Drinks (up to 24% Juice), capturing a market share of 60%. This dominance is largely driven by mass-market accessibility and the strong presence of brands such as FoodStar (Deedo). These products are favored for casual refreshment and benefit from deep distribution in neighborhood convenience stores and local grocers, where price sensitivity and immediate availability serve as primary purchase decision factors. Affordability and distribution breadth establish juice drinks as the volume anchor within Thailand's competitive beverage landscape.

As the market matures through 2032, this 60% share segment will serve as a critical testing ground for novel sensory experiences. Manufacturers are expected to integrate textures such as jellies or fruit bits into lower-percentage juices to maintain end user engagement amid rising competition from ready-to-drink teas and energy drinks. While 100% juice and plant waters focus on premium wellness positioning, the juice drinks segment remains the volume anchor by providing affordable, flavorful variety to the broader Thai population. This segment's volume foundation enables brands to fund premium innovation while maintaining mass market penetration and distribution scale across diverse retail touchpoints.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment commanding the highest share within the sales channel division is Off-Trade, capturing 85% of total market sales. This channel's strength is rooted in Thailand's bifurcated retail landscape, where convenience stores and small local grocers serve as primary touchpoints for daily refreshment. These outlets prove essential for high-volume, lower-percentage juice drinks relying on purchase frequency and impulse buying, particularly in regions outside major urban centers where traditional trade remains the economic backbone. The 85% share reflects deep retail infrastructure integration across diverse geographic markets.

Within the off-trade segment, modern trade channels including supermarkets and rapidly growing retail e-commerce are becoming premiumization engines. These platforms enable brands to highlight functional benefits and high-quality ingredients, supporting value-added positioning appealing to urban, health-conscious shoppers. While mass channels sustain volume fundamentals, the shift toward discovery-led shopping in modern retail enables the off-trade segment to maintain its dominant 85% share as end user priorities evolve toward wellness. The channel's combination of mass accessibility and premium discovery capabilities creates a comprehensive distribution ecosystem accommodating both value-driven and health-motivated juice purchasing behaviors.

List of Companies Covered in UAE Juice Market

The companies listed below are highly influential in the UAE juice market, with a significant market share and a strong impact on industry developments.

- Aujan Coca-Cola Beverages Co

- Marmum Dairy Farm LLC

- Capri Sun Group Holding AG

- Al Rawabi Co

- Almarai Co Ltd

- Al Ain Dairy Co

- Al Boheira Lacnor Co

- Barakat Ltd

- Fit Fresh LLC

- International Beverage & Filling Industries

Competitive Landscape

The UAE juice market is led by Al Rawabi, which commands strong volume share in reconstituted 100% juice while maintaining presence across nectars and juice drinks, leveraging local production and brand trust. It is also the fastest-growing major player, benefiting from demand for natural positioning and broad supermarket distribution. New Age Beverages, via Vita Coco, is a dynamic challenger capitalising on rapid growth in coconut and plant waters aligned with plant-based wellness trends. In contrast, Del Monte faces decline in not-from-concentrate 100% juice amid intensifying competition from competitively priced local brands and hypermarket fresh offerings. Indirect pressure from freshly squeezed counters and functional beverages persists. Differentiation opportunities lie in no added sugar claims, vitamin fortification, smart packaging engagement, and deeper localisation of sourcing to manage costs and reinforce quality perception.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- UAE Juice Market Policies, Regulations, and Standards

- UAE Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- UAE Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Region

- Dubai

- Abu Dhabi

- Sharjah

- Northern Emirates

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- UAE 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Al Rawabi Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Almarai Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Ain Dairy Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Boheira Lacnor Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Barakat Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aujan Coca-Cola Beverages Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Marmum Dairy Farm LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Capri Sun Group Holding AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fit Fresh LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- International Beverage & Filling Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Rawabi Co

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.