US In-Vehicle Intrusion Detection Systems Market Report: Trends, Growth and Forecast (2026-2032)

By Component (Hardware, Software, Services), By Deployment (Centralized IDS, Distributed IDS, Hierarchical IDS), By Detection Layer (Network-Based IDS, Host-Based IDS, Hybrid IDS), By Detection Methodology (Signature-Based Detection, Anomaly-Based Detection, Specification-Based Detection, Hybrid Detection), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)), By Communication Interface (CAN (Controller Area Network), LIN (Local Interconnect Network), FlexRay, Automotive Ethernet, Others), By Region (West, Midwest, South, North, Northeast) ... Read more

|

Major Players

|

The US In-Vehicle Intrusion Detection Systems Market Statistics and Insights, 2026

- Market Size Statistics

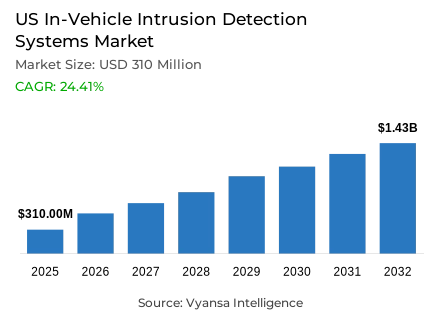

- In-vehicle intrusion detection systems market size in The US was valued at USD 310 million in 2025 and is estimated at USD 352 million in 2026.

- The market size is expected to grow to USD 1.43 billion by 2032.

- Market to register a CAGR of around 24.41% during 2026-32.

- Component Shares

- Software grabbed market share of 53%.

- Competition

- More than 10 companies are actively engaged in producing in-vehicle intrusion detection systems in The US.

- Top 5 companies acquired around 30% of the market share in 2026.

- NXP Semiconductors N.V., Karamba Security Ltd., Upstream Security Ltd., Aptiv PLC, Harman International Industries Incorporated (Samsung Electronics Co. Ltd.) etc., are few of the top companies.

- Deployment

- Distributed ids grabbed 45% of the market.

The US In-Vehicle Intrusion Detection Systems Market Outlook

The US In-Vehicle Intrusion Detection Systems (IDS) Market was valued at USD 310 million in 2025 and is projected to grow from USD 352 million in 2026 to USD 1.43 billion by 2032, exhibiting a CAGR of 24.41% during the forecast period. Growth is being supported by rising vehicle connectivity, increasing deployment of software-defined vehicle architectures, and growing cybersecurity requirements across modern transportation systems. As vehicles incorporate more digital functions, cloud connectivity, telematics, advanced driver assistance systems, and over-the-air software updates, protecting vehicle communication networks has become a critical priority for automotive manufacturers.

The cybersecurity environment in the United States continues to strengthen the need for advanced threat detection capabilities. According to the FBI Internet Crime Report 2024, the agency received 859,532 cybercrime complaints and recorded more than USD 16.6 billion in reported losses. Although these incidents span multiple industries, they highlight the broader escalation of cyber risks affecting connected technologies. As a result, automotive companies are increasing investments in vehicle cybersecurity, automotive intrusion detection, and real-time threat monitoring solutions designed to improve automotive cyber resilience.

Software represents the largest component segment with a share of approximately 53%, reflecting the growing reliance on automotive cybersecurity software, security analytics platforms, and vehicle network security tools. Distributed IDS accounts for around 45% of deployment demand, supported by its ability to provide broader visibility across electronic control units, gateways, telematics systems, and in-vehicle communication networks. These architectures are becoming increasingly important as vehicle software complexity continues to increase.

The In-Vehicle Intrusion Detection Systems (IDS) Market is also benefiting from growing adoption of connected vehicle security solutions, automotive threat intelligence platforms, and AI-powered automotive IDS technologies. Expanding vehicle connectivity, rising cybersecurity governance requirements, and continued development of software-defined vehicle security frameworks are supporting long-term demand for advanced vehicle cyber protection capabilities across the US automotive ecosystem.

The US In-Vehicle Intrusion Detection Systems Market Growth Driver

Connected Vehicle Expansion Increases Cybersecurity Requirements

Growing connected vehicle adoption is increasing the need for advanced vehicle cybersecurity across automotive ecosystems. Modern vehicles rely on telematics systems, cloud connectivity, vehicle-to-everything communication, advanced driver assistance systems, and OTA software updates, creating a larger attack surface for potential cyber threats. According to the FBI Internet Crime Report 2024, the agency received 859,532 complaints and reported losses exceeding USD 16.6 billion, highlighting the broader rise in cyber risks across connected digital environments.

The US in-vehicle intrusion detection systems (IDS) market benefits from increasing vehicle connectivity expansion because manufacturers require real-time threat monitoring capabilities that can identify suspicious behavior across vehicle communication networks. As connected vehicle security becomes a strategic requirement, automotive manufacturers are deploying automotive intrusion detection and vehicle network security solutions to improve visibility, strengthen automotive cyber resilience, and support secure vehicle communications throughout the vehicle lifecycle.

The US In-Vehicle Intrusion Detection Systems Market Challenge

Managing Cybersecurity Complexity Across Vehicle Architectures

Vehicle network complexity is creating implementation challenges for cybersecurity providers and automakers. Modern vehicles integrate numerous electronic control units, wireless communication modules, cloud-connected applications, infotainment platforms, and telematics systems. Securing these interconnected environments requires continuous monitoring, extensive validation, and cybersecurity management throughout development and operation. UNECE WP.29 cybersecurity requirements further increase compliance obligations by requiring manufacturers to maintain Cyber Security Management Systems across the vehicle lifecycle.

The US in-vehicle intrusion detection systems (IDS) market also faces challenges related to IDS integration complexity and cross-platform compatibility issues. Security solutions must operate across diverse vehicle architectures while maintaining detection accuracy and minimizing false positive detection issues. As software-defined vehicles become more common, balancing cybersecurity performance, operational efficiency, and compliance requirements remains a key challenge for industry participants.

Unlock Market Intelligence

Explore the market potential with our data-driven report

The US In-Vehicle Intrusion Detection Systems Market Trend

AI-Powered Threat Detection Gains Momentum

Artificial intelligence is becoming increasingly important within automotive cybersecurity strategies. Vehicle networks generate large volumes of operational data that require continuous analysis to identify unusual behavior and emerging cyber threats. As a result, manufacturers are increasingly deploying AI-powered automotive IDS platforms that support automotive threat intelligence, behavioral threat detection, and real-time anomaly detection across connected vehicle environments.

The US in-vehicle intrusion detection systems (IDS) market is witnessing stronger adoption of machine learning cybersecurity tools, anomaly-based IDS solutions, and automotive security orchestration capabilities. These technologies improve the ability to detect both known and previously unseen threats while supporting automotive cyber defense strategies across software-defined vehicle security platforms. The trend reflects a broader shift toward predictive cyber defense and data-driven threat monitoring across modern vehicle ecosystems.

The US In-Vehicle Intrusion Detection Systems Market Opportunity

Cybersecurity Governance Expands Deployment Scope

Growing emphasis on cybersecurity governance is creating additional adoption opportunities across the automotive sector. NIST Cybersecurity Framework 2.0 places greater focus on governance, risk management, and cybersecurity program maturity, encouraging organizations to strengthen cybersecurity oversight across connected technologies. Similar initiatives from National Highway Traffic Safety Administration (NHTSA) and Cybersecurity and Infrastructure Security Agency (CISA) emphasize continuous monitoring, risk management, and lifecycle cybersecurity practices for connected systems.

The US in-vehicle intrusion detection systems (IDS) market is increasingly relevant within this environment because intrusion detection technologies support automotive cybersecurity management systems, vehicle cyber risk management, and continuous security monitoring objectives. As manufacturers strengthen governance frameworks and automotive cyber resilience programs, demand for automotive threat detection, security event management, and vehicle security analytics solutions is expected to expand across connected vehicle platforms.

Unlock Market Intelligence

Explore the market potential with our data-driven report

The US In-Vehicle Intrusion Detection Systems Market Segmentation Analysis

By Component

- Hardware

- Software

- Services

Software accounts for approximately 53% of the component segment in the US in-vehicle intrusion detection systems (IDS) market. The dominance of software reflects the increasing reliance on analytics engines, threat intelligence integration, anomaly detection algorithms, and cybersecurity monitoring solutions to identify suspicious activities across vehicle communication networks. Software-driven security platforms allow manufacturers to update detection capabilities as new threats emerge.

The US in-vehicle intrusion detection systems (IDS) market continues to witness growing adoption of automotive cybersecurity software because it supports security analytics platforms, automotive security analytics, and continuous monitoring requirements. These capabilities are becoming increasingly important as connected vehicle ecosystems expand and cybersecurity threats evolve across software-defined vehicle environments.

By Deployment

- Centralized IDS

- Distributed IDS

- Hierarchical IDS

Distributed IDS represents approximately 45% of deployment demand within the US in-vehicle intrusion detection systems (IDS) market. This architecture enables monitoring across multiple vehicle subsystems, providing broader visibility into vehicle communication channels, gateways, electronic control units, and connected interfaces. Such visibility is increasingly important as vehicles incorporate more connected and software-driven functions.

The US in-vehicle intrusion detection systems (IDS) market benefits from distributed deployment models because they improve vehicle network monitoring, strengthen ECU security, and support CAN bus security across complex vehicle architectures. As connected vehicle protection requirements continue to increase, distributed IDS deployments remain well suited for identifying cyber threats across multiple points within modern vehicle networks.

List of Companies Covered in The US In-Vehicle Intrusion Detection Systems Market

The companies listed below are highly influential in the The US in-vehicle intrusion detection systems market, with a significant market share and a strong impact on industry developments.

- NXP Semiconductors N.V.

- Karamba Security Ltd.

- Upstream Security Ltd.

- Aptiv PLC

- Harman International Industries Incorporated (Samsung Electronics Co. Ltd.)

- Robert Bosch GmbH (including brands)

- Continental AG (including brands)

- DENSO Corporation

- GuardKnox Cyber Technologies Ltd.

- VicOne Corporation (Trend Micro Incorporated)

Market News & Updates

- Karamba Security Ltd., 2026:

Karamba Security announced a multi-year licensing renewal and expansion agreement for its XGuard cybersecurity platform. The platform incorporates host-based intrusion detection and prevention capabilities designed to monitor runtime behavior, protect memory integrity, prevent unauthorized code execution, and detect advanced cyber threats affecting connected devices. The agreement expands deployment of XGuard's embedded cybersecurity technologies and supports increasing demand for edge-based security architectures applicable to connected vehicles and software-defined mobility platforms.

- VicOne Corporation (Trend Micro Incorporated), 2025:

VicOne announced the integration and validation of its xCarbon On-Board IDS/IPS solution with the Red Hat In-Vehicle Operating System for software-defined vehicles. The solution provides operating system-level intrusion detection, runtime anomaly monitoring, and automated threat mitigation capabilities designed to identify and block cyberattacks before they propagate across vehicle networks. The technology was showcased at the North American Intelligent Cockpit and Smart Driving Summit in Detroit, supporting automotive OEMs and suppliers developing secure software-defined vehicle architectures.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- The US In-Vehicle Intrusion Detection Systems (IDS) Market Policies, Regulations, and Standards

- The US In-Vehicle Intrusion Detection Systems (IDS) Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- The US In-Vehicle Intrusion Detection Systems (IDS) Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component

- Hardware- Market Insights and Forecast 2022-2032, USD Million

- Software- Market Insights and Forecast 2022-2032, USD Million

- Services- Market Insights and Forecast 2022-2032, USD Million

- By Deployment

- Centralized IDS- Market Insights and Forecast 2022-2032, USD Million

- Distributed IDS- Market Insights and Forecast 2022-2032, USD Million

- Hierarchical IDS- Market Insights and Forecast 2022-2032, USD Million

- By Detection Layer

- Network-Based IDS- Market Insights and Forecast 2022-2032, USD Million

- Host-Based IDS- Market Insights and Forecast 2022-2032, USD Million

- Hybrid IDS- Market Insights and Forecast 2022-2032, USD Million

- By Detection Methodology

- Signature-Based Detection- Market Insights and Forecast 2022-2032, USD Million

- Anomaly-Based Detection- Market Insights and Forecast 2022-2032, USD Million

- Specification-Based Detection- Market Insights and Forecast 2022-2032, USD Million

- Hybrid Detection- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type

- Passenger Cars- Market Insights and Forecast 2022-2032, USD Million

- Light Commercial Vehicles (LCVs)- Market Insights and Forecast 2022-2032, USD Million

- Heavy Commercial Vehicles (HCVs)- Market Insights and Forecast 2022-2032, USD Million

- By Communication Interface

- CAN (Controller Area Network)- Market Insights and Forecast 2022-2032, USD Million

- LIN (Local Interconnect Network)- Market Insights and Forecast 2022-2032, USD Million

- FlexRay- Market Insights and Forecast 2022-2032, USD Million

- Automotive Ethernet- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Region

- West- Market Insights and Forecast 2022-2032, USD Million

- Midwest- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- North- Market Insights and Forecast 2022-2032, USD Million

- Northeast- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Component

- Market Size & Growth Outlook

- The US Hardware Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Detection Layer- Market Insights and Forecast 2022-2032, USD Million

- By Detection Methodology- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Communication Interface- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The US Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Detection Layer- Market Insights and Forecast 2022-2032, USD Million

- By Detection Methodology- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Communication Interface- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- The US Services Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Deployment- Market Insights and Forecast 2022-2032, USD Million

- By Detection Layer- Market Insights and Forecast 2022-2032, USD Million

- By Detection Methodology- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Communication Interface- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Aptiv PLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Harman International Industries Incorporated (Samsung Electronics Co. Ltd.)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Robert Bosch GmbH (including brands)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Continental AG (including brands)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DENSO Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NXP Semiconductors N.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Karamba Security Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Upstream Security Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GuardKnox Cyber Technologies Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- VicOne Corporation (Trend Micro Incorporated)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aptiv PLC

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Component |

|

| By Deployment |

|

| By Detection Layer |

|

| By Detection Methodology |

|

| By Vehicle Type |

|

| By Communication Interface |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.