Japan Software-Defined Vehicle (SDV) Platforms Market Report: Trends, Growth and Forecast (2026-2032)

By Component (Software, Services), By Software Application Domain (ADAS & Autonomous Driving Software, Infotainment & Digital Cockpit Software, Powertrain Control Software, Chassis & Vehicle Dynamics Software, Body & Comfort Software, Cross-Vehicle Enablers (Platform Infrastructure) (Vehicle OS & Middleware, OTA Update Management, Cybersecurity, DevOps & Toolchains)), By Deployment Mode (On-Board (Embedded), Cloud-Based, Hybrid (On-Board + Cloud)), By End-User (Automotive OEMs, Tier-1 Suppliers, Fleet Operators & Mobility Service Providers), By Vehicle Type (Passenger Vehicles, Commercial Vehicles) ... Read more

|

Major Players

|

Japan Software-Defined Vehicle (SDV) Platforms Market Statistics and Insights, 2026

- Market Size Statistics

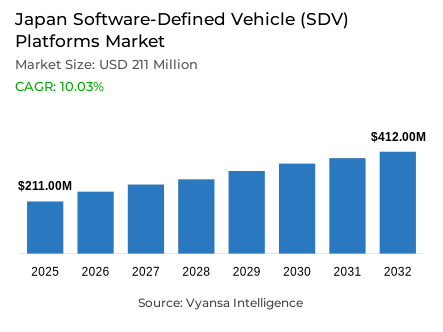

- Software-defined vehicle (sdv) platforms market size in Japan was valued at USD 211 million in 2025 and is estimated at USD 267 million in 2026.

- The market size is expected to grow to USD 412 million by 2032.

- Market to register a CAGR of around 10.03% during 2026-32.

- Software Application Domain Shares

- Adas & autonomous driving software grabbed market share of 35%.

- Competition

- Software-defined vehicle (sdv) platforms in Japan is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 30% of the market share in 2026.

- Panasonic Automotive Systems Co. Ltd., Toyota Motor Corporation (Arene), Honda Motor Co. Ltd. (ASIMO OS), Renesas Electronics Corporation (RoX), Qualcomm Japan GK (Snapdragon Digital Chassis) etc., are few of the top companies.

- Deployment Mode

- On-board (embedded) grabbed 45% of the market.

Japan Software-Defined Vehicle (SDV) Platforms Market Outlook

The Japan software-defined vehicle (SDV) platforms market covers vehicle operating systems, middleware, application software, cloud interfaces, development toolchains, cybersecurity layers, and integration services. Japanese OEMs, Tier-1 suppliers, semiconductor vendors, and cloud providers form demand nationally. Valued at USD 211 million in 2025, the Japan software-defined vehicle (SDV) platforms market reaches USD 267 million in 2026 and USD 412 million by 2032, reflecting a 10.03% CAGR. The Japan software-defined vehicle (SDV) platforms industry anchors mobility strategies.

Demand is moving toward automotive software platforms that separate application development from hardware cycles, support over-the-air updates, and connect functions with cloud services. Honda identifies ASIMO OS as the foundation for AD/ADAS, dynamics control, and experience from 2026. Honda’s official 2025 business briefing demonstrates how standardization redirects procurement toward scalable stacks. The Japan software-defined vehicle (SDV) platforms market gains from centralized vehicle computing, while the Japan software-defined vehicle (SDV) platforms industry develops around longer lifecycles.

Platform adoption changes development economics by enabling common code, virtual validation, continuous integration, and coordinated deployment across models. The Japan software-defined vehicle (SDV) platforms market supports shorter engineering cycles, reuse of embedded automotive software, and stronger control over post-production updates. Suppliers combining automotive high-performance computing with middleware and applications can capture broader scope. Meanwhile, the Japan software-defined vehicle (SDV) platforms industry must align functional safety, data governance, software assurance, and supplier accountability across interconnected chains.

Commercial momentum in 2026 centers on production-ready platforms rather than demonstrations. The Japan software-defined vehicle (SDV) platforms market is advancing through proprietary OEM environments, cross-domain controllers, semiconductor reference platforms, and automotive cloud platforms. Investment priorities favor zonal E/E architecture, virtual ECUs, secure pipelines, and vehicle data platforms. This shift strengthens providers with integration capabilities and local support, while the Japan software-defined vehicle (SDV) platforms industry moves toward repeatable deployments across passenger and commercial programs.

platforms market competitive analysis")

Japan Software-Defined Vehicle (SDV) Platforms Market Growth Driver

Software Complexity Converts into Platform Procurement

Rising software complexity is increasing demand for reusable platforms that coordinate safety, cockpit, connectivity, and vehicle-control functions across model lines. The Japan software-defined vehicle (SDV) platforms market benefits because common middleware and development environments reduce duplicated engineering, improve release governance, and support faster feature deployment. Japanese OEMs are therefore shifting procurement from isolated electronic-control-unit software toward integrated stacks, validation tools, and lifecycle services that can support continuous upgrades without redesigning each vehicle program.

Honda opened Honda Software Studio Osaka in April 2025 to strengthen software development and create new mobility value through collaboration with technology companies and academic institutions. Honda’s official announcement confirms a dedicated domestic operation supporting software-defined vehicle development. This expansion strengthens demand for engineering toolchains, middleware, testing environments, and connected vehicle platforms. It also signals that the Japan software-defined vehicle (SDV) platforms industry requires local talent pools and supplier integration to convert software-first strategies into production programs.

Japan Software-Defined Vehicle (SDV) Platforms Market Challenge

Talent and Integration Gaps Constrain Execution

Software talent scarcity and cross-domain integration complexity constrain execution as vehicle platforms combine safety-critical code, cloud connectivity, AI models, and legacy electronic architectures. The Japan software-defined vehicle (SDV) platforms market faces longer validation cycles when suppliers use incompatible development environments or fragmented data structures. Automotive cybersecurity, functional-safety assurance, and software-update compliance add further engineering workload, while responsibility boundaries between OEMs, Tier-1 suppliers, semiconductor companies, and cloud providers can slow procurement decisions and raise program-management costs.

Japan’s Ministry of Economy, Trade and Industry reported a notable shortage of software-related human resources and identified development and retention as a competitive requirement. The 2024 Mobility DX Strategy summary outlines training, reskilling, certification, and industry-collaboration measures. Limited specialist availability restricts architecture design, validation, and secure OTA implementation, particularly for smaller suppliers. Consequently, the Japan software-defined vehicle (SDV) platforms industry must expand workforce pipelines while standardizing interfaces and development processes to prevent recurring deployment bottlenecks.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Software-Defined Vehicle (SDV) Platforms Market Trend

Production Vehicles Move from Pilots to Platform Deployment

Production adoption is replacing concept-stage experimentation as automakers embed common software foundations into saleable vehicles. The Japan software-defined vehicle (SDV) platforms market is shifting toward architectures that support coordinated cockpit, safety, and control applications through shared development environments. Full-vehicle OTA capability, software-hardware decoupling, and virtual validation are becoming competitive differentiators because they improve feature velocity and reduce dependence on conventional model-year updates. Platform providers are consequently prioritizing production certification, scalability, and multi-domain integration over standalone demonstrations.

Toyota launched the sixth-generation RAV4 in Japan on December 17, 2025, marking the first production use of its Arene software development platform. Toyota’s official launch release states that Arene shortened development for Toyota Safety Sense and cockpit software and supports future simultaneous updates across multiple functions. This deployment validates commercial demand for integrated toolchains and reusable software components, strengthens supplier requirements for platform compatibility, and raises competitive pressure on rival proprietary OEM operating environments.

Japan Software-Defined Vehicle (SDV) Platforms Market Opportunity

Open Cloud-to-Vehicle Ecosystems Expand Supplier Access

Open cloud-to-vehicle engineering ecosystems represent an underpenetrated opportunity for suppliers able to connect in-car systems with simulation, data analytics, digital twins, and remote operations. The Japan software-defined vehicle (SDV) platforms market can expand beyond embedded licensing toward development services, cloud-managed testing, fleet data processing, and lifecycle orchestration. Providers that offer secure APIs and interoperable toolchains can improve market access among OEMs and Tier-1 suppliers seeking faster development without building every platform layer internally.

Astemo Cypremos and Wipro announced in June 2025 that they would jointly build and operate an Internet of Vehicles platform supporting digital engineering. Astemo’s official release states that planned capabilities include data analysis, digital-twin development support, and simulators spanning in-car and out-car domains. The initiative creates supplier opportunities in automotive cloud platforms, vehicle data management, cybersecurity, and engineering automation. It also expands demand capture for service providers that can localize scalable platform operations for Japanese vehicle programs.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Software-Defined Vehicle (SDV) Platforms Market Segmentation Analysis

By Software Application Domain

- ADAS & Autonomous Driving Software

- Infotainment & Digital Cockpit Software

- Powertrain Control Software

- Chassis & Vehicle Dynamics Software

- Body & Comfort Software

- Cross-Vehicle Enablers (Platform Infrastructure)

- Vehicle OS & Middleware

- OTA Update Management

- Cybersecurity

- DevOps & Toolchains

ADAS & Autonomous Driving Software holds 35% under the Software Application Domain category, supported by strong demand for perception, sensor fusion, behavior planning, driver monitoring, and safety-control functions. The Japan software-defined vehicle (SDV) platforms market concentrates value in this domain because advanced driving functions require high computing performance, continuous model improvement, and rigorous validation. Integration with mapping, connectivity, and vehicle-control layers also increases software content per program and strengthens procurement demand for scalable, safety-certified development platforms.

Nissan stated in April 2026 that it aims to deploy Nissan AI Drive technology across 90% of its lineup over the long term, while the new Elgrand will adopt next-generation ProPILOT with end-to-end autonomous capability by fiscal 2027. Nissan’s official mobility vision demonstrates expanding production pathways for autonomous driving software. Broader model coverage strengthens demand for reusable ADAS stacks, AI validation environments, automotive semiconductors, and secure update mechanisms across domestic vehicle development and deployment programs.

platforms market segmentation overview")

By Deployment Mode

- On-Board (Embedded)

- Cloud-Based

- Hybrid (On-Board + Cloud)

On-Board (Embedded) holds 45% under the Deployment Mode category because control-critical workloads require deterministic response, functional safety, continuous availability, and low-latency processing independent of network conditions. Embedded deployment remains central for ADAS, powertrain, chassis, body control, and cockpit functions. OEM procurement therefore favors tightly integrated compute, middleware, and application stacks that can operate reliably inside vehicles while selectively connecting to cloud resources for analytics, development, content delivery, and noncritical service orchestration across connected fleets.

DENSO announced in September 2024 that its new Zenmyo facility would primarily manufacture large-scale integrated ECUs required for overall vehicle-function control. DENSO’s official plant announcement specifies digital infrastructure, flexible production, and capability for 24-hour unmanned operation. This capacity direction supports on-board embedded SDV platforms by improving supply readiness for cross-domain controllers. It also strengthens domestic integration between software, semiconductors, electronic hardware, and safety-critical vehicle applications as centralized architectures enter wider Japanese production programs at commercial scale.

List of Companies Covered in Japan Software-Defined Vehicle (SDV) Platforms Market

The companies listed below are highly influential in the Japan software-defined vehicle (sdv) platforms market, with a significant market share and a strong impact on industry developments.

- Panasonic Automotive Systems Co. Ltd.

- Toyota Motor Corporation (Arene)

- Honda Motor Co. Ltd. (ASIMO OS)

- Renesas Electronics Corporation (RoX)

- Qualcomm Japan GK (Snapdragon Digital Chassis)

- ETAS K.K.

- DENSO Corporation

- Astemo Ltd.

- Nissan Motor Co. Ltd.

- Google Cloud Japan G.K.

Market News & Updates

- Renesas Electronics Corporation (RoX), 2025:

Renesas expanded its R-Car Gen 5 software-defined vehicle platform with R-Car X5H silicon samples, complete evaluation boards, and the RoX Whitebox software development kit. The platform combines ADAS, infotainment, real-time operating systems, edge AI, Linux, Android, and virtualization through a multi-domain compute architecture. The update gives Japanese OEMs and Tier-1 suppliers a more complete environment for centralized vehicle software development.

- Panasonic Automotive Systems Co. Ltd., 2025:

Panasonic Automotive Systems expanded its VERZEUSE cybersecurity series for cockpit high-performance computers and integrated vehicle ECUs. The update adds protection for virtualized software environments and supports security across vehicle design, implementation, assessment, operation, and software updates. The release supports Japanese SDV programs that require lifecycle cybersecurity for centralized computing and continuously updated vehicle functions.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Japan Software-Defined Vehicle (SDV) Platforms Market Policies, Regulations, and Standards

- Japan Software-Defined Vehicle (SDV) Platforms Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Japan Software-Defined Vehicle (SDV) Platforms Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component

- Software- Market Insights and Forecast 2022-2032, USD Million

- Services- Market Insights and Forecast 2022-2032, USD Million

- By Software Application Domain

- ADAS & Autonomous Driving Software- Market Insights and Forecast 2022-2032, USD Million

- Infotainment & Digital Cockpit Software- Market Insights and Forecast 2022-2032, USD Million

- Powertrain Control Software- Market Insights and Forecast 2022-2032, USD Million

- Chassis & Vehicle Dynamics Software- Market Insights and Forecast 2022-2032, USD Million

- Body & Comfort Software- Market Insights and Forecast 2022-2032, USD Million

- Cross-Vehicle Enablers (Platform Infrastructure)- Market Insights and Forecast 2022-2032, USD Million

- Vehicle OS & Middleware- Market Insights and Forecast 2022-2032, USD Million

- OTA Update Management- Market Insights and Forecast 2022-2032, USD Million

- Cybersecurity- Market Insights and Forecast 2022-2032, USD Million

- DevOps & Toolchains- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode

- On-Board (Embedded)- Market Insights and Forecast 2022-2032, USD Million

- Cloud-Based- Market Insights and Forecast 2022-2032, USD Million

- Hybrid (On-Board + Cloud)- Market Insights and Forecast 2022-2032, USD Million

- By End-User

- Automotive OEMs- Market Insights and Forecast 2022-2032, USD Million

- Tier-1 Suppliers- Market Insights and Forecast 2022-2032, USD Million

- Fleet Operators & Mobility Service Providers- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type

- Passenger Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Commercial Vehicles- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Component

- Market Size & Growth Outlook

- Japan ADAS & Autonomous Driving Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Infotainment & Digital Cockpit Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Powertrain Control Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Chassis & Vehicle Dynamics Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Body & Comfort Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Japan Cross-Vehicle Enablers (Platform Infrastructure) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Semiconductor & Computing Platform Providers

- Renesas Electronics Corporation (RoX)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Qualcomm Japan GK (Snapdragon Digital Chassis)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Renesas Electronics Corporation (RoX)

- Vehicle OS, Middleware & Enabler Platform Providers

- ETAS K.K.

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ETAS K.K.

- Tier-1 Suppliers with SDV Platform Capabilities

- DENSO Corporation

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Astemo Ltd.

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Panasonic Automotive Systems Co. Ltd.

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DENSO Corporation

- OEMs with Proprietary SDV Platforms

- Toyota Motor Corporation (Arene)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Honda Motor Co. Ltd. (ASIMO OS)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nissan Motor Co. Ltd.

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Toyota Motor Corporation (Arene)

- Cloud & Technology Platform Providers

- Google Cloud Japan G.K.

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Google Cloud Japan G.K.

- Semiconductor & Computing Platform Providers

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Component |

|

| By Software Application Domain |

|

| By Deployment Mode |

|

| By End-User |

|

| By Vehicle Type |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.