UAE Pet Products Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Cat Litter, Pet Healthcare (Flea/Tick Treatments, Pet Dietary Supplements, Worming Treatments, Others), Other Pet Products (Beauty Products, Accessories, Others)), By Sales Channel (Retail Offline, Retail E-Commerce, Veterinary Clinics) ... Read more

|

Major Players

|

UAE Pet Products Market Statistics and Insights, 2026

- Market Size Statistics

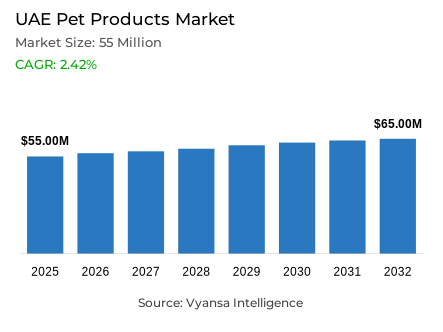

- Pet Products inUAE is estimated at $ 55 Million.

- The market size is expected to grow to $ 65 Million by 2032.

- Market to register a CAGR of around 2.42% during 2026-32.

- Product Shares

- Other Pet Products grabbed market share of 60%.

- Competition

- More than 20 companies are actively engaged in producing Pet Products inUAE.

- Top 5 companies acquired 35% of the market share.

- Radio Systems Corp, Group55 Ltd, VitaPower Ltd, The Pet Shop LLC, Four Paws Products Ltd etc., are few of the top companies.

- Sales Channel

- Veterinary Clinics grabbed 40% of the market.

UAE Pet Products Market Outlook

The UAE pet products market was valued at USD 55 million in 2025 and is projected to grow from USD 56.3 million in 2026 to USD 65 million by 2032, registering a CAGR of 2.42% across the forecast period. This measured expansion reflects a steady and structurally supported growth environment across the UAE, where rising pet ownership, deepening emotional investment between owners and their pets, and greater willingness to spend on comfort, appearance, and daily care are collectively shaping a more mature and commercially active market. Growth is being driven not by a single catalyst but by a convergence of lifestyle-led purchasing, regulatory formalisation, and a broader cultural shift toward treating pets as integral members of the household.

Product demand within the UAE market is anchored by the other pet products category, which commands 60% of the overall market share. This leading position is supported by the broad and growing appeal of grooming items, accessories, bedding, clothing, and toys among local consumers who are increasingly looking to purchase beyond basic functional needs. As pet humanisation continues to influence purchasing behaviour across the UAE, non-essential product categories are attracting stronger and more consistent spending from owners who view these purchases as meaningful expressions of care, personality, and lifestyle.

Sales channel dynamics are shaped equally by the dominant role of Veterinary Clinics, which hold 40% of the total market. This prominence reflects the institutional trust that pet owners place in clinical environments for health-adjacent product recommendations, preventive care items, supplements, and professionally guided purchases. At the same time, e-commerce is asserting a growing complementary role as owners seek the convenience of home delivery, wider product assortment, and easier access to specialty and routine-use items across digital platforms.

The overall market trajectory through 2032 remains well-supported as personalisation, premiumisation, and digital convenience continue to influence how and where owners spend on their pets. Stronger interest in customised offerings, rising demand for premium materials and health-oriented products, and the continued widening of online retail infrastructure are all expected to sustain momentum throughout the forecast period, positioning the UAE as one of the more commercially dynamic pet product markets in the broader Middle East region.

UAE Pet Products Market Growth Driver

Formalised Ownership Framework Builds Recurring Product Demand

The growing formalisation of responsible pet ownership across the UAE is emerging as one of the most consequential and commercially durable drivers of product demand in the market. As per data published by the Department of Municipalities and Transport of Abu Dhabi, animal ownership services were officially launched through the TAMM platform on February 3, 2025, establishing a centralised database linking registered owners with their microchipped animals. The programme formally integrates annual vaccinations, microchipping requirements, and regular veterinary check-ups as expected components of responsible ownership, creating a structured health routine that directly supports recurring demand for care-related and wellness-oriented pet products sold through trusted channels.

This shift from casual ownership to a regulated and health-conscious routine is redefining the commercial dynamics of everyday pet product spending in the UAE. According to statistics released by the Department of Municipalities and Transport, registration fees have been waived until further notice and existing individual pet owners are granted a one-year grace period to complete the process, which is expected to accelerate enrolment and broaden participation across the ownership base. As more owners enter a formalised care routine that emphasises hygiene, preventive health, and regular professional engagement, spending on grooming, wellness, and support products is becoming both more frequent and more deeply embedded in the everyday lifestyle of pet-owning households across the UAE.

UAE Pet Products Market Challenge

Import and Licensing Conditions Constrain Market Pace

Strict regulatory requirements governing both pet imports and veterinary channel operations are creating a persistent and commercially meaningful constraint on the pace of market expansion across the UAE. Based on data from the Ministry of Climate Change and Environment of the UAE, individuals are permitted to import a maximum of two companion animals per person in any given year, and pet import permits carry a validity window of only 90 days. These procedural limits place a structural ceiling on the speed at which new pet households are formed, which in turn moderates the rate at which fresh product demand can be generated across the market.

The regulatory pressure is equally visible within the veterinary distribution channel, which remains a primary route for healthcare-adjacent pet products across the UAE. As indicated by authoritative sources at the Ministry of Climate Change and Environment, veterinary establishment licenses carry a one-year validity period, an annual renewal fee of AED 500 applies, and the renewal service page currently records 5,574 company transactions. This reflects an active but compliance-intensive operating environment where periodic renewal obligations, facility-level requirements, and licensing oversight can meaningfully increase the administrative burden on product-linked veterinary distributors and slow the pace at which clinic-based retail channels scale across the country.

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Pet Products Market Trend

Digital Retail Infrastructure Is Redefining Consumer Access

A well-defined and commercially significant trend is reshaping how consumers discover, evaluate, and purchase specialty products across the UAE, as digital retail infrastructure expands at a pace that is broadening access to niche and lifestyle-driven categories. Evidence drawn from public data released by the Dubai Department of Economy and Tourism confirms that the Dubai Traders programme onboarded more than 2,400 new e-commerce sellers within its first twelve months of operation while simultaneously providing targeted growth support to 1,000 existing online sellers. This rapid expansion of digital selling capacity is making it easier for specialised pet product offerings to reach a wider and more geographically distributed consumer base across the UAE.

The commercial implications for pet-related categories are particularly strong, given that convenience and product variety are primary purchase drivers in this segment. In line with findings from the Dubai Department of Economy and Tourism, sellers participating in the programme gained access to millions of consumers through established partnerships with major platforms, while 42% expanded into new product categories and 63% added new stock keeping units to their existing digital offerings. As online retail continues to widen its reach and assortment depth, it is progressively reshaping how pet owners across the UAE engage with the market, shifting discovery and purchase decisions toward digital-first behaviours that favour accessible, well-presented, and conveniently delivered products.

UAE Pet Products Market Opportunity

Economic Strength Creates Favourable Conditions for Premium Spending

The UAE's robust macroeconomic environment is creating a commercially compelling opportunity for brands positioned in higher-value and lifestyle-oriented pet product categories. As per official figures from the Central Bank of the UAE, real GDP grew by 5.6% in 2025 while inflation eased to 1.3%, a combination that directly supports household purchasing power and gives premium product providers more room to justify elevated price positioning around quality, wellness, comfort, and design. In a market where discretionary spending is structurally well-supported, the conditions for premiumisation are more favourable than in most comparable regional markets.

This opportunity becomes more strategically attractive because premium positioning aligns naturally with the lifestyle-led retail culture that characterises consumer spending across the UAE. Based on data from the Central Bank of the UAE, economic expansion in 2025 was underpinned by strong non-oil sector contributions and continued structural diversification, reinforcing the durability of the broader spending environment beyond any single sector or cyclical factor. For pet product suppliers, this creates meaningful room to develop differentiated offerings across premium accessories, higher-quality grooming lines, personalised and custom-designed items, and wellness-oriented products that appeal to owners who are seeking added value, self-expression, and care quality rather than simply meeting basic functional requirements.

| Report Coverage | Details |

|---|---|

| Market Forecast | 2026-32 |

| USD Value 2025 | $ 55 Million |

| USD Value 2032 | $ 65 Million |

| CAGR 2026-2032 | 2.42% |

| Largest Category | Other Pet Products segment leads with 60% market share |

| Top Drivers | Formalised Ownership Framework Builds Recurring Product Demand |

| Top Challenge | Import and Licensing Conditions Constrain Market Pace |

| Top Trends | Digital Retail Infrastructure Is Redefining Consumer Access |

| Top Opportunities | Economic Strength Creates Favourable Conditions for Premium Spending |

| Key Players | Radio Systems Corp, Group55 Ltd, VitaPower Ltd, The Pet Shop LLC, Four Paws Products Ltd, Pet Head Inc, Beaphar BV, Merial Ltd, Mars GCC, TFH Publications and Others. |

Unlock Market Intelligence

Explore the market potential with our data-driven report

UAE Pet Products Market Segmentation Analysis

By Product

- Cat Litter

- Pet Healthcare

- Flea/Tick Treatments

- Pet Dietary Supplements

- Worming Treatments

- Others

- Other Pet Products

- Beauty Products

- Accessories

- Others

The segment with highest market share under Product is other pet products command the highest share at 60%, a position that reflects broad and deeply embedded consumer appetite for grooming items, accessories, bedding, clothing, and toys across the UAE's pet-owning population. Owners across the country are consistently purchasing products that go beyond essential care, driven by a strong humanisation trend that frames pet spending as an extension of personal lifestyle and an expression of emotional attachment. This segment's dominance confirms that indulgence-oriented and comfort-focused purchasing is not a peripheral behaviour but a central commercial force within the UAE pet products market.

Its sustained leadership also signals that product innovation and lifestyle alignment are more important drivers of category performance than purely functional demand. Owners across the UAE are using non-essential pet products to express affection, curate the appearance and comfort of their animals, and participate in a growing culture of pet-lifestyle consumption that closely mirrors broader personal care and lifestyle retail trends. As premiumisation and personalisation continue to gain traction, this segment is expected to remain the primary commercial pillar of the market and the category most responsive to innovation-led growth throughout the forecast period.

By Sales Channel

- Retail Offline

- Retail E-Commerce

- Veterinary Clinics

Veterinary Clinics hold the highest share within the sales channel category at 40%, establishing professional clinical environments as the most commercially significant route through which pet products reach consumers across the UAE. Owners are consistently choosing clinic-based purchasing for healthcare-adjacent products, prescription items, supplements, and preventive care solutions because the channel combines direct product access with professional guidance, trusted recommendations, and a health-focused context that reinforces confidence in the purchase. This channel's lead position confirms that trust and expertise remain primary decision drivers in how UAE pet owners choose where to buy.

Its continued dominance also reflects the structural importance of health-oriented product distribution in a market where formalised ownership and veterinary engagement are becoming more deeply embedded in everyday pet care routines. As registration programmes and annual health check requirements expand across the UAE, the veterinary clinic channel is expected to see sustained footfall from owners fulfilling structured care obligations, creating consistent and predictable opportunities for product sales within a professionally managed environment. Through the forecast period, this channel is expected to maintain its leadership as the most influential and commercially dependable route to market within the UAE pet products market.

List of Companies Covered in UAE Pet Products Market

The companies listed below are highly influential in the UAE pet products market, with a significant market share and a strong impact on industry developments.

- Radio Systems Corp

- Group55 Ltd

- VitaPower Ltd

- The Pet Shop LLC

- Four Paws Products Ltd

- Pet Head Inc

- Beaphar BV

- Merial Ltd

- Mars GCC

- TFH Publications

Competitive Landscape

UAE pet products market is witnessing strong momentum, driven by the rising humanisation of pets, where owners increasingly treat pets as family members and spend on grooming, accessories and premium care items. The “other pet products” category leads growth, supported by demand for grooming essentials, personalised accessories, luxury bedding and interactive toys that enhance pet wellbeing. The Pet Shop LLC continues to strengthen its leadership through brands like Trixie, while Mars Incorporated maintains dominance in cat litter with Thomas. Veterinary clinics and e-commerce remain key distribution channels, combining trust, specialised healthcare offerings and convenience. Looking ahead, personalisation and premiumisation trends, supported by rising disposable incomes and growing awareness of pet health, are expected to sustain market expansion.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- UAE Pet Products Market Policies, Regulations, and Standards

- UAE Pet Products Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- UAE Pet Products Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Cat Litter- Market Insights and Forecast 2022-2032, USD Million

- Pet Healthcare- Market Insights and Forecast 2022-2032, USD Million

- Flea/Tick Treatments- Market Insights and Forecast 2022-2032, USD Million

- Pet Dietary Supplements- Market Insights and Forecast 2022-2032, USD Million

- Worming Treatments- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- Other Pet Products- Market Insights and Forecast 2022-2032, USD Million

- Beauty Products- Market Insights and Forecast 2022-2032, USD Million

- Accessories- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Retail E-Commerce- Market Insights and Forecast 2022-2032, USD Million

- Veterinary Clinics- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- UAE Cat Litter Products Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Pet Healthcare Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- UAE Other Pet Products Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Pet Shop LLC, The

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Four Paws Products Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pet Head Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Beaphar BV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Merial Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Radio Systems Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Group55 Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- VitaPower Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mars GCC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TFH Publications

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pet Shop LLC, The

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.