Switzerland Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

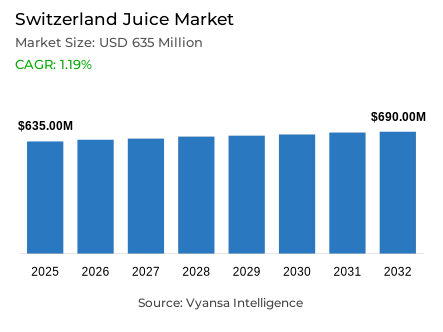

Switzerland Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in Switzerland was estimated at USD 635 million in 2025.

- The market size is expected to grow to USD 690 million by 2032.

- Market to register a CAGR of around 1.19% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 75%.

- Competition

- More than 10 companies are actively engaged in producing juice in Switzerland.

- Top 5 companies acquired around 65% of the market share.

- Capri Sun GmbH, Thurella AG, Rivella AG, Migros Genossenschaftsbund eG, Ramseier Suisse AG etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 80% of the market.

Switzerland Juice Market Outlook

The Switzerland juice market is a wellestablished and largely retailbased market that is currently facing a stagnant volume growth. It is estimated to increase to a projected USD 635 million in 2025 to USD 690 million in 2032, with a compound annual growth rate of about 1.19% between 2026 and 2032. Even though the Swiss end user consider juice as a healthy substitute to the carbonated drinks, the rising prices, which can be explained by the climaterelated shortages in harvesting in South America and Europe, have led to more responsible drinking habits.

The category is still supported by health and wellness, and end user are highly interested in natural, organic, and lowsugar options. In this environment, 100% Juice enjoys a leading market share of 75% indicating the preference of the shoppers to highquality and minimally processed products. However, traditional juices are facing stiff competition with new functional segments like flavored waters and readytodrink teas that offer hydration but have fewer calories.

Innovation is increasingly being functional and nichebased. Plantbased waters, especially coconut, are becoming important drivers of growth, due to their richness in electrolytes and low caloric content. Innocent and other brands like this lead this growth, leveraging on the marketing power of their parent company CocaCola and on a strong presence in the functional beverage market. At the same time, longestablished players like Migros and Coop are still imposing their will through highend ownlabel products that emphasize organic and Fairtrade certifications.

In the future, the market will experience a slow change that will be propelled by technology and trade policy. The high cost of production can hinder the rapid introduction of new manufacturing technology, but the possibility of a Mercosur freetrade agreement can eventually improve costefficiency in importing fruits. The sales channel remains centralized in the offtrade channel, which is supported by the high levels of supermarket penetration and the increasing need to have healthconscious vending solutions that can support the fastpaced onthego lifestyle of the country.

Switzerland Juice Market Growth DriverChronic Disease and Weight Concerns Sustaining Demand for Better-for-You Beverage Choices

The health still makes the choice of beverages a subject of long-term examination. The findings of Swiss Health Survey show that 55 per cent of women and 44 per cent of men live with at least one chronic disease, and 52 per cent of men and 34 per cent of women are overweight or obese. These statistics highlight the fact that a significant percentage of the adult population is overloaded with chronic illnesses or weight-related health issues, which makes daily beverage decisions the part of the personalized health-management plan. The high rate of chronic illness therefore maintains end user interest in the nutritional content and health effects of drinks.

This climate promotes drinks that preempt naturalness and reduced sugar levels, which in turn improves the positioning of juice as a better substitute to most sweetened soft drinks. It also creates a tendency to smaller, better-quality purchases and functional positioning that end users can afford even in the face of price increases, thus remaining relevant to the niche plant waters and functional juice ideas on Swiss shelves. The demand trends of health-conscious individuals provide favourable opportunities to premium, naturally positioned juice substitutes. Brands with proven health credentials, such as lower sugar, functional, and clean ingredient profiles, are placed to attract health-conscious end users who manage chronic conditions, thus sustaining category demand in the Swiss health-conscious end user environment, which is typified by a high chronic disease burden.

Switzerland Juice Market ChallengeStructurally High Price Levels Limiting Pricing Headroom and Dampening Juice Volumes

The structural cost system in Switzerland makes juice more susceptible to price resistance compared to lower-price markets. In the international price comparison of the Federal Statistical Office in 2024, the Swiss price level is 158.8 index points, compared to the EU27 level of 100. The purchasing-power parity of Switzerland is also reported in the same release as CHF 1.51 per euro, which shows that households face significantly higher baseline prices before any category-specific cost shocks. This structural cost disadvantage stiffens the affordability constraint, thus limiting the flexibility of category pricing.

Shoppers are less tolerant and respond quickly when the supply of fruits is interrupted or the cost of inputs increases further to raise the price of juice. They decrease the purchase rate, switch to own label, purchase smaller packs, or replace with substitutes like functional waters and ready-to-drink tea, which provide perceived health and convenience at a reduced outlay. This price ceiling is the key driver that stifles the volumes of juice in a mature, retail-dominated category. The structural cost environment creates enduring affordability issues that limit volume growth. The end user price sensitivity coupled with high levels of baseline price restricts the ability of manufacturers to pass through cost increases, thus requiring high levels of cost management, value demonstration and strategic positioning to maintain volumes in the expensive, mature market of Switzerland where end users can easily substitute to alternative beverages.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Switzerland Juice Market TrendUltra-Low Inflation Amplifying Sensitivity to Visible Shelf-Price Increases

Switzerland inflation is extremely low, which has radically changed the way end users perceive shelf-price changes. According to the Federal Statistical Office, the end user price index stood at 106.9 points in December 2025, with a base of 100 in December 2020. In the same update, year-on-year inflation is +0.1% in December 2025 and an average of +0.2% per year in 2025. Such a remarkably low inflation environment increases sensitivity to any apparent price increases in categories. Within this low-inflation environment, price increases at the category level are especially salient and cause more accelerated substitution behaviour. In the case of juice, an increase in unit prices due to supply constraints or pack-size changes is more salient, and end users are more likely to respond by considering juice as a luxury and substituting it with other ready-to-drink products that are perceived to be healthier and more cost-effective, particularly functional water and ready-to-drink tea. Retailers thus strengthen promotions and more distinct value levels to sustain demand.

The low-inflationary trend fosters increased price transparency and faster substitution processes. In the case of general price levels being stable, any category that is inflated will become conspicuous, forcing brands to be extremely careful with pricing, invest in promotion, and show clear value propositions to prevent a rapid shift to alternatives in the Swiss price-stable, value-conscious market environment.

Switzerland Juice Market OpportunityEFTA–Mercosur Trade Tailwinds Supporting Input Cost Efficiency and Price Stabilisation

Trade policy offers a high degree of leverage to counter cost pressures that affect Swiss shelf prices. According to the State Secretariat for Economic Affairs, the EFTAMercosur agreement has the potential to produce savings in customs of more than CHF155million annually after the expiry of tariff-reduction periods. SECO also observes that about 96 percent of Swiss exports to Mercosur countries would be completely free of custom duties. These liberalisation advantages offer great opportunities to lower the input costs by improving the sourcing economics.

In the case of juice supply chains, the opportunity is to leverage tariff cuts and more transparent trade regulations to enhance sourcing economics of South American fruit ingredients and minimise landed-cost volatility. More predictable input costs contribute to more consistent price levels and reduce the necessity of pack-size cuts that increase unit prices. In a full-grown segment where customers rapidly switch to functional water or ready-to-drink tea when juice seems costly, price stability protects demand and allows investing in low-sugar recipes and eco-friendly packaging. The opportunity of trade agreement provides manufacturers with cost-management tools that maintain price competitiveness and margin stability. Through preferential trade terms, the brands will be able to counterbalance the structural cost disadvantages of Switzerland, keep prices competitive, and reinvest the savings in innovation, which will sustain long-term category health in the expensive and substitution-prone market environment of Switzerland.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Switzerland Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the Switzerland juice market, where 100% Juice grabbed a market share of 75%. This overwhelming dominance is rooted in the Swiss consumer's strong preference for premium, natural products that align with strict health and quality standards. Even as prices rise due to global supply challenges, shoppers in Switzerland tend to favor the nutritional integrity of 100% juice over nectars or diluted drinks.

To maintain this lead, brands are focusing on locally sourced and organic labels to justify higher unit prices. While the overall category faces pressure from lowcalorie alternatives like functional water, the 100% juice segment remains resilient by positioning itself as a "qualityoverquantity" staple. Future growth in this area is expected to be supported by innovations in coldpressed technology and more sustainable, plantbased packaging, catering to the country's high environmental and wellness consciousness.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is the OffTrade, accounting about 80%. Supermarkets specifically lead this channel, holding over 46% of all volume sales. This dominance is anchored by major retail chains like Migros and Coop, which leverage their massive footprints and highly popular private label lines to remain the primary destination for household juice purchases.

The offtrade segment is further bolstered by the rising cost of living, which has encouraged end user to buy juice for home consumption rather than dining out. Additionally, modern convenience trends are sparking growth in niche areas of the offtrade channel, such as vending machines. These automated outlets are increasingly stocked with healthy juice options to meet the demand from younger, mobile generations who prioritize quick, healthy snacks during their commutes or busy workdays.

List of Companies Covered in Switzerland Juice Market

The companies listed below are highly influential in the Switzerland juice market, with a significant market share and a strong impact on industry developments.

- Capri Sun GmbH

- Thurella AG

- Rivella AG

- Migros Genossenschaftsbund eG

- Ramseier Suisse AG

- Coop Genossenschaft

- Eckes-Granini (Suisse) SA

- innocent Alps GmbH

- Tropicana Europe NV

- Schlör AG

Competitive Landscape

Switzerland juice market is experiencing stagnant performance in 2025, primarily due to rising retail prices linked to droughts, citrus greening and other climate-related disruptions affecting key sourcing regions, which have pushed up production costs and reduced volumes. As unit prices increase and pack sizes shrink, price-sensitive consumers are cutting back or switching to alternatives such as functional bottled water and RTD tea, intensifying competitive pressure within soft drinks. Although juice retains a relatively healthy image compared to carbonates, this is no longer sufficient to offset affordability concerns. At the same time, coconut and other plant waters are gaining traction thanks to their low-calorie positioning, electrolyte content and functional appeal. Over the forecast period, sales are expected to remain broadly flat, with maturity, high saturation and sustained price pressures limiting stronger recovery despite incremental innovation in sustainability and sugar reduction.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Switzerland Juice Market Policies, Regulations, and Standards

- Switzerland Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Switzerland Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Switzerland 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Switzerland Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Switzerland Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Switzerland Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Switzerland Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Migros Genossenschaftsbund eG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ramseier Suisse AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coop Genossenschaft

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eckes-Granini (Suisse) SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- innocent Alps GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Capri Sun GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thurella AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rivella AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tropicana Europe NV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Schlör AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Migros Genossenschaftsbund eG

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.