Sweden Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

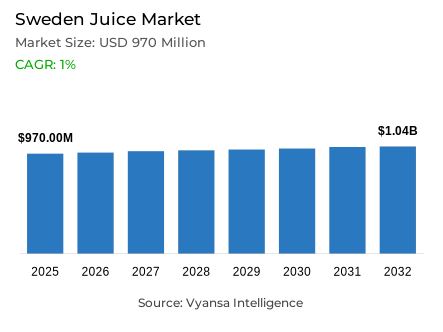

Sweden Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in Sweden was estimated at USD 970 million in 2025.

- The market size is expected to grow to USD 1.04 billion by 2032.

- Market to register a CAGR of around 1% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 55%.

- Competition

- More than 20 companies are actively engaged in producing juice in Sweden.

- Top 5 companies acquired around 55% of the market share.

- Coca-Cola Enterprises Sverige AB, Karl Fazer Oy Ab, Carlsberg Sverige AB, Proviva AB, Eckes-Granini Sverige AB etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 85% of the market.

Sweden Juice Market Outlook

The Sweden juice market is going through a difficult phase characterized by a major shortage of oranges in the world market and changing consumer health attitudes. The market is estimated to be USD 970 million in 2025 and USD 1.04 billion in 2032 with a CAGR of about 1% between 2026 and 2032. The high prices of orangejuice have been caused by extreme weather and citrus greening in key producer nations, which has reduced demand and led to many end user switching to cheaper substitutes like nectars or other flavors of fruit like apple.

Market dynamics are largely driven by health and wellness trends, with end user shunning highsugar content. This has seen an increase in the popularity of zerosugar products and naturally functional drinks like coconut water. Thai Agri Foods under its Foco brand has managed to position coconut water as a healthy, electrolyterich substitute to postworkout hydration. At the same time, demographic changes, namely a decreasing birth rate among the population aged 014, will put the pressure on the category of juicedrink, which is traditionally popular among younger end user.

Proviva AB maintains its leadership in the competitive environment due to diversified portfolio, active marketing, and robust healthbased positioning. The firm has been able to maintain pricesensitive customers through the provision of zerosugar versions and healthoriented innovations. Digitalisation is also a major factor in the development of the market, as QR codes on packaging help to achieve sustainability goals and fastdelivery applications increase accessibility.

sales channel is primarily centered in the OffTrade channel, which grabbed 85% of the market in 2025. Supermarkets like ICA and Axfood remain dominant due to their wide variety and strong private label lines. However, discounters like Lidl are emerging as the most dynamic channel, attracting shoppers with competitively priced branded products and economical private labels as the cost of living remains high. To stay resilient, producers are expected to focus on highquality, notfromconcentrate products that appeal to a broader adult demographic.

Sweden Juice Market Growth DriverValue-Led Grocery Behaviour Sustaining Trade-Down Demand for Affordable Juice Formats

Swedish end user are valueconscious because the price of necessities is still high, despite the decline in headline inflation. According to statistics Sweden, CPI inflation stands at 0.3% in December 2025, and food and nonalcoholic beverages are increasing by 3.1% annually in November 2025. This price difference continues to strain grocery budgets and makes valuebased juice formats more competitive than highend 100% juice. The gap between general and food inflation generates longterm affordability pressures that fuel valuebased buying patterns.

This pricing climate forces end user to consider price per litre, multipack options and ownlabel options to control overall expenditure, which in turn favors demand of cheaper blends and nectars. Discount positioning and frequent promotions by retailers thus have bigger roles in ensuring that juice remains a household regular. Costmanaged brands that do not raise shelfprices abruptly are in a better position to retain repeat purchases and household penetration. Valueled demand shift is a strategic reaction to endemic food inflation, which needs brands to streamline cost bases, show explicit value propositions, and compete efficiently on price without sacrificing quality perceptions in the pricesensitive consumer market in Sweden, which is typified by cautious expenditure despite declining headline inflation.

Sweden Juice Market ChallengeOrange Input Price Volatility Maintaining Structural Cost and Pricing Instability

The juice in orange is still very vulnerable to volatility of raw materials since a significant portion of the category relies on orange concentrate. IMF Primary Commodity Prices indicate the orangelinked benchmark price increasing to 3.0 in 2023, then to 5.0 in 2024, then to 3.7 in 2025, and 2.4 in 2025. These dramatic fluctuations impose significant margin pressures and pricing complexity on manufacturers trying to keep retail prices steady as they deal with fluctuating input prices.

These volatilities increase the demands of pricing discipline in Sweden significantly. When prices shoot up, manufacturers are forced to either absorb the shocks by reducing their margins or transfer the rise to end user who are already tight with their wallets. The unpredictable supply also makes it difficult to agree on volumes with retailers and may interfere with promotional plans, which puts the risk of less shelf space on core orange flavours. This exposure to rawmaterials is a structural limitation to the stable unit pricing and volume retention of the category. The volatility of orange supply poses a sustained problem in managing margins, promotional planning, and stability of relationships with retailers. To reduce the impact of inputcost volatility and remain competitive in the valueconscious market environment of Sweden, manufacturers need to devise hedging strategies, diversify the sourcing of fruits, and strengthen supplychain resilience.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Sweden Juice Market TrendMainstream Online Purchasing Shifting Beverage Discovery Toward Digital Shelf Execution

In Sweden, online purchasing behaviour is mainstream, and it is changing the way beverage brands are promoted to shoppers and how end user learn about new SKUs. According to statistics Sweden, in 2025, 76% of individuals purchased goods or services online within the past three months, and 9% purchased online within three to twelve months ago. This unprecedented digital uptake makes ecommerce the main channel of purchase and not an auxiliary one, which generates strategic demands of digital excellence.

With such a high degree of digital buying, grocery ecommerce and appbased delivery are more applicable touchpoints to juice than in most traditional beverage categories. A robust digital shelf presence, product image, and speed of message delivery around value and health positioning are becoming more and more demanded by producers because online comparisons are immediate and price transparency is complete. This continued channel migration supports the functions of datadriven promotions and convenient home delivery in ensuring the availability of juice. The digital buying trend is a radical shift in the consumerbrand relationship, where digital discoverability, comparative assessment, and convenient fulfilment are prioritised. Brands with high ecommerce performance, digital marketing performance, and onlinetodelivery experiences are well placed to attract emerging digitalfirst consumer groups in the digitally advanced, highly connected market environment in Sweden.

Sweden Juice Market OpportunityReduced-Sugar Reformulation White Space Enabling Everyday Wellness Repositioning for Juice

The sugar and health examination opens up a significant potential of reformulated juice that is more justifiable in everyday diets. The Public Health Agency of Sweden monitors the increase in the consumption of sweetened drinks, and the proportion of people who consume sweetened drinks at least twice a week is growing by 28 to 34% between 2016 and 2024. In 2024, the share is nearly 60% among adults between 16 and 29, which indicates high levels of sweetened beverage consumption especially among younger populations who need healthier options.

In the case of juice brands, this environment provides a chance to attract shoppers with lowersugar recipes, smaller portion packs, and the frontofpack communication that emphasizes the fruit content without overpromising. Blends of multifruits with easily accessible fruits and vegetables can also be used to reposition the category towards everyday wellness and decrease the use of most sugarrelated variants. Competitive pricing and credible nutrition messaging in products are more likely to turn healthconscious end user who appreciate taste and convenience. The lowersugar option would allow the manufacturers to cater to the increasing health awareness and distinguish themselves among the highly sweetened drinks. Authentic sugar reduction and retained taste profiles can win healthconscious end user and create a premium positioning through wellness associations in the growing healthconscious beverage market in Sweden.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Sweden Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the Sweden juice market, where 100% Juice grabbed a market share of 55%. This segment remains the core of the market due to its strong appeal among adults who value high juice content and natural nutrients. Despite the significant price hikes caused by the global orange concentrate shortage, 100% juice continues to be perceived as a more premium and "real" option compared to diluted alternatives, helping it maintain more than half of the total market value.

Innovation within this segment is shifting toward notfromconcentrate (NFC) varieties, which are projected to be more resilient to demographic changes than children's juice drinks. While orange remains a staple flavor, high prices have encouraged experimentation with apple and vegetable blends. As healthconscious end user scrutinize sugar levels, brands are increasingly focusing on clearly labeled health benefits and premium positioning to justify higher price points and retain their 55% share in a maturing market.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is the OffTrade, which grabbed 85% of the market. This channel's dominance is driven by the Swedish habit of purchasing juice as a staple during regular grocery trips. Supermarkets are the primary engine for these sales, offering high visibility and a diverse range of both mainstream brands and private labels. The convenience of onestop shopping allows supermarkets to cater to both budgetconscious families and those seeking premium, healthoriented products.

While the offtrade channel is established, it is seeing a shift in dynamics as discounters gain traction. Driven by the soaring costs of raw materials like oranges, more end user are visiting discounters to find valueformoney private label options. Additionally, digital integration through online grocery platforms and quickdelivery apps is modernizing the offtrade experience. Despite these shifts, the physical retail environment remains the essential pillar for juice sales channel in Sweden, holding the vast majority of market volume through 2032.

List of Companies Covered in Sweden Juice Market

The companies listed below are highly influential in the Sweden juice market, with a significant market share and a strong impact on industry developments.

- Coca-Cola Enterprises Sverige AB

- Karl Fazer Oy Ab

- Carlsberg Sverige AB

- Proviva AB

- Eckes-Granini Sverige AB

- Skånemejerier AB

- Innocent Ltd

- Loviseberg Presseri AB

- Kiviks Musteri AB

- Axfood AB

Competitive Landscape

Sweden juice market faced a challenging year in 2025, as a global orange shortage disrupted supply and pushed concentrate prices to record highs, leading to a decline in off-trade volume sales. With orange traditionally the leading flavour, poor harvests in Brazil, the US and Spain driven by extreme weather and citrus greening significantly constrained availability. At the same time, persistent cost-of-living pressures encouraged consumers to cut back on higher-priced beverages such as 100% juice, while ongoing concerns about sugar content further weighed on demand. Apple consequently overtook orange in juice drinks, reflecting supply-side adjustments. Nectars recorded the slowest decline due to their more affordable positioning. Despite digital innovation and interest in zero-sugar and premium offerings, structural pressures are expected to continue limiting growth prospects.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Sweden Juice Market Policies, Regulations, and Standards

- Sweden Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Sweden Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Sweden 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Sweden Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Sweden Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Sweden Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Sweden Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Proviva AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eckes-Granini Sverige AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Skånemejerier AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Innocent Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Loviseberg Presseri AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Karl Fazer Oy Ab

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Carlsberg Sverige AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kiviks Musteri AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Axfood AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ICA Sverige AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Proviva AB

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.