Spain Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

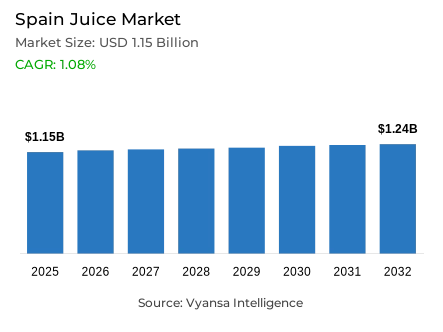

Spain Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in Spain was estimated at USD 1.15 billion in 2025.

- The market size is expected to grow to USD 1.24 billion by 2032.

- Market to register a CAGR of around 1.08% during 2026-32.

- Category Shares

- Juice drinks (up to 24% juice) grabbed market share of 40%.

- Competition

- More than 15 companies are actively engaged in producing juice in Spain.

- Top 5 companies acquired around 65% of the market share.

- Juver Alimentación SA, Cía Servicios de Bebidas Refrescantes SL, Zumos Palma SL, Mercadona SA, Centros Comerciales Carrefour SA etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 80% of the market.

Spain Juice Market Outlook

The Spain juice market is undergoing contraction as end user negotiate a costofliving crisis and growing intolerance of sugar. The market is estimated to be valued at USD 1.15 billion in 2025 and USD 1.24 billion in 2032 with a compound annual growth rate of about 1.08% in the 2026-32 period. This low growth rate is indicative of a fragmented market: valueconscious households prefer valuebased products, and a niche healthconscious segment drives the demand of highquality, functional, and superfoodenriched juices.

The industry is challenged by the rising cost of production and climaterelated volatility, particularly affecting citrus supply chains. Brands are in turn responding by orienting towards innovation in order to maintain relevance. Eckes Granini and Innocent lead these initiatives with practical shots and vegetable blends, but Juver has launched AIbased solutions to create individual recipes, aiming to establish new consumption moments outside the traditional breakfast environment.

One of the key market segments is the Juice Drinks (up to 24 % juice) segment, which has a significant market share of 40 %. The products have remained popular due to their low prices and a variety of flavour, including tropical flavours with pitaya and guava. At the same time, the industry is also investing in sustainable, onthego formats to appeal to younger, ecoconscious end user who are more concerned with convenience and transparent labeling.

The sales channel is still largely concentrated in the offtrade segment that took 80% of the market in 2025. The main sources of household juice purchases are supermarkets like Mercadona, which has a dominant Hacendado brand of the product. However, ecommerce is the most rapidly expanding channel, which enjoys improved coldchain logistics that make the online sale of fresh and perishable juices more feasible to busy Spanish end user.

Spain Juice Market Growth DriverSchool Nutrition Standards Strengthening No-Added-Sugar Credibility and Portion-Control Innovation

Mandatory nutritional standards now govern food and beverages sold through school vending machines and cafeteria services in Spain under Royal Decree No. 315/2025. The regulation caps each packaged serving at 200 kilocalories and restricts added or free sugars to a maximum of 5 grams per portion. However, this sugar threshold does not apply to fruit juices and vegetable-based beverages that contain no added sugars. Effective from 16 April 2026, the measure creates differentiated regulatory treatment that favours naturally occurring sugars and strengthens incentives for reformulation and clean-label positioning within the beverage category.

This rule reinforces the prioritisation of sugar reduction in the public policy and requires juice producers to enhance their credibility by implementing noaddedsugar formulations and offering clear ingredient labels. It maintains the demand of 100 percent juice, vegetable blends and smaller functional formats that align with family purchasing patterns. Conversely, products with added sugar face increased pressure to reformulate or must shift their consumption outside of controlled school settings. Royal Decree 315/2025 grants structural benefits to naturally sweetened juice formats and establishes compliance obstacles to addedsugar forms. In turn, this regulatory framework significantly reorganizes the opportunities in the school sales channel channel, in favour of manufacturers that can prove to be natural positioning and portionappropriate packaging in compliance with the nutritional standards and the wellness priorities of families.

Spain Juice Market ChallengeExtreme Heat and Rainfall Deficits Elevating Fruit Supply Volatility and Cost Risk

Spain is projected to experience its hottest summer since records began in 1961, with the average temperature across the peninsula expected to reach 24.2°C. This level stands 2.1°C above the long-term seasonal average, highlighting the intensity of the anticipated heat conditions. This summer is described in the same report as arid, with a mean precipitation of 57.0mm across peninsular Spain, which is 81% of the normal of 19912020. These drastic climatic conditions create a lot of agricultural pressure and instability in production.

The heat and the lack of rainfall increase the threats to the stability of the yield and quality of fruits, especially citrus varieties, which are the foundation of many juice products. Increased climatic volatility increases reliance on irrigation, makes storage more difficult, and increases the complexity of sourcing. At the same time, retailers and end user are showing resistance to additional price increases, thus narrowing margins and making competition of juice products with lowercost or functional beverage substitutes difficult. The volatility of supply due to climate creates structural cost pressures and quality consistency challenges. The manufacturers must deal with uncertainty in production and maintain competitive prices, which requires sophisticated supplychain management, diversified sourcing policies, and climateadaptation investments in the increasingly unpredictable Spanish agricultural environment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Juice Market TrendRapid E-Commerce Expansion Increasing Price Transparency and Accelerating Brand Switching

According to the National Commission on Markets and Competition, ecommerce revenue in Spain reached 25.752 b billion in the first quarter of 2025, which is an increase of 18.2 per cent. compared to the same period in 2024. At the same time, more than 474.3 million transactions were registered, which is an increase of 14.9% per year. This rapid growth of online trade essentially transforms the retail dynamics and competitive strategies of beverages.

As digital buying grows, juice products are competing more in online grocery stores where price comparison is immediate and brand switching is achieved with very little resistance. This situation highlights the importance of open pricing, product labeling, and strong promotional implementation. Simultaneously, the digital platforms support the delivery of the benefits of functional and premium juice variants via the description of the products and personalised recommendations, which promotes trial and repeat purchases. The move towards ecommerce represents a paradigm shift to pricetransparent, conveniencebased buying experiences, which requires brands to streamline their online presence, competitive pricing, and benefit communication. Digital channels offer the potential of premium positioning through improved storytelling and at the same time increase price competition through instant comparability across the fastdigitising grocery market in Spain.

Spain Juice Market OpportunityRising AI Adoption Enabling Personalised Engagement and New Juice Consumption Occasions

According to the National Statistics Institute, 21.1% of Spanish firms with ten or more employees use artificial intelligence in the first quarter of 2025. This number is a growth of 8.7%age points compared to the first quarter of 2024, which shows how quickly AI capabilities are diffusing into the commercial sector. This kind of technological advancement has significant opportunities of advanced consumer interaction and customised marketing approaches.

In the case of juice manufacturers and retailers, the use of artificial intelligence can be used to personalise consumer interactions, create recipe suggestions, and advertise functional or noaddedsugar options in online retail environments. The AIpowered tools can contribute to the development of new consumption moments, especially when the classic ones like breakfast lose their significance. Individualised suggestions and ingredientbased advice rebrand juice as a component of smoothies, meal combinations, and wellness practices, thus reinforcing interaction beyond pricebased competition. This AI opportunity allows manufacturers to provide customised value propositions, promote targeting, and build direct consumer relationships based on datadriven personalisation. Brands with advanced AI usage can distinguish themselves by offering personalised recommendations, increased usage cases, and functional benefit communication, thus facilitating longterm engagement in the increasingly technologyadvanced retail landscape in Spain.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the Spanish juice market, where Juice Drinks (up to 24% Juice) grabbed a market share of 40%. This dominance is largely due to the segment's appeal as a valueoriented choice for families and pricesensitive end user. During the ongoing costofliving crisis, these drinks have maintained their position as a versatile and affordable alternative to 100% juices, which have seen sharper price increases due to raw material shortages.

To keep this segment competitive, manufacturers are focusing on flavor innovation and the addition of functional benefits. Brands like Pascual are revitalizing the category with new tropical blends and "superfood" infusions like spirulina and ginger. By aligning these popular, lowerjuicecontent drinks with health and wellness trends, companies are successfully retaining a broad consumer base while mitigating the overall volume decline seen across the broader Spanish juice industry.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is the OffTrade, which grabbed 80% of the market. This channel is anchored by the deeprooted habit of juice being a primary family staple, usually purchased in bulk during weekly grocery trips. Supermarkets lead this space, representing nearly 50% of the total value share, as they provide the ideal platform for highvolume sales through private label dominance and aggressive price promotions.

While the offtrade channel remains the market's backbone, it is also the stage for the most significant digital shifts. Ecommerce is currently the most dynamic retail subchannel, as improved logistics allow for the safe delivery of premium, fresh, and coldpressed juices directly to end user' homes. This ensures that while physical retail continues to command the vast majority of sales, the offtrade segment is evolving to meet the modern demand for convenience and digital accessibility.

List of Companies Covered in Spain Juice Market

The companies listed below are highly influential in the Spain juice market, with a significant market share and a strong impact on industry developments.

- Juver Alimentación SA

- Cía Servicios de Bebidas Refrescantes SL

- Zumos Palma SL

- Mercadona SA

- Centros Comerciales Carrefour SA

- Eckes-Granini International

- J García Carrión SA

- Schweppes SA

- Aguas Danone SA

- Tropicana Alvalle SL

Competitive Landscape

Spain juice market continues to record declining retail volume sales as price sensitivity, rising production costs and growing health concerns redirect demand towards flavoured water, coconut water and functional beverages. The category is increasingly polarised: value-driven households favour private label options led by Mercadona’s Hacendado, while a smaller health-focused segment supports functional and premium innovations from players such as J. García Carrión (Don Simón), Eckes-Granini, Pascual, Innocent Iberia and Juver Alimentación. Brands are responding with vegetable-based blends, superfood-infused variants, limited editions and AI-driven engagement tools to create new consumption occasions. However, climate-related volatility affecting citrus supply and persistent sugar avoidance are expected to maintain downward pressure, even as supermarkets dominate distribution and e-commerce posts the fastest growth.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Spain Juice Market Policies, Regulations, and Standards

- Spain Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Spain Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Spain 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Spain Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Mercadona SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- J García Carrión SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Schweppes SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Centros Comerciales Carrefour SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eckes-Granini International

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Juver Alimentación SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cía Servicios de Bebidas Refrescantes SL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zumos Palma SL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aguas Danone SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Calidad Pascual SAU

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mercadona SA

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.