Spain Fire Pump Market Report: Trends, Growth and Forecast (2026-2032)

By Pump Type (Centrifugal Pumps (Overhung Pumps, Vertical Inline, Horizontal End Suction), Split Case Pumps (Single/Two Stage, Multi Stage)), Positive Displacement Pumps (Diaphragm Pumps, Piston Pumps), By Mode of Operation (Diesel Fire Pump, Electric Fire Pump, Others), By End-User (Residential, Commercial, Industrial) ... Read more

|

Major Players

|

Spain Fire Pump Market Statistics and Insights, 2026

- Market Size Statistics

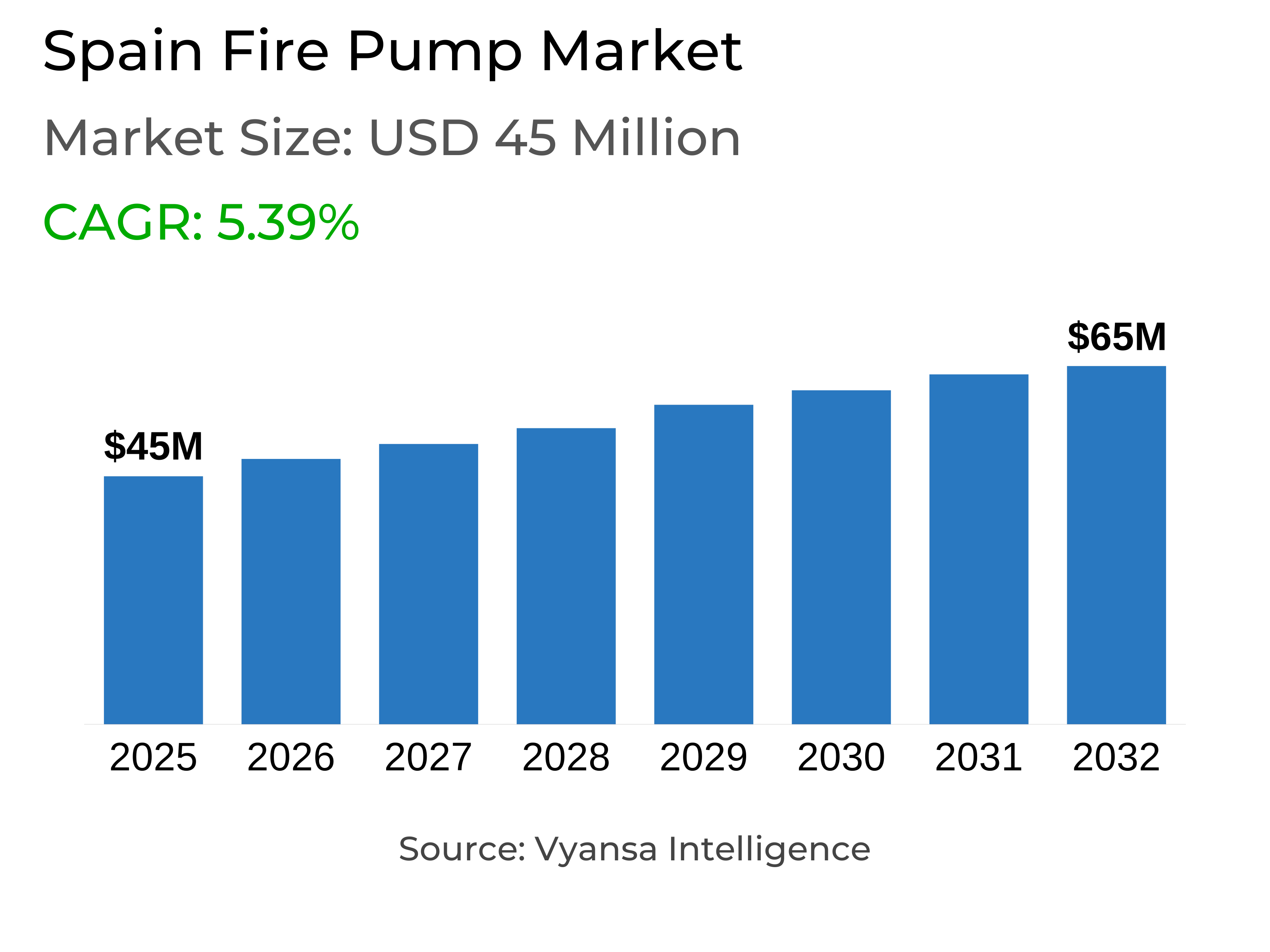

- Fire Pump in Spain is estimated at $ 45 Million.

- The market size is expected to grow to $ 65 Million by 2032.

- Market to register a CAGR of around 5.39% during 2026-32.

- Pump Type Segment

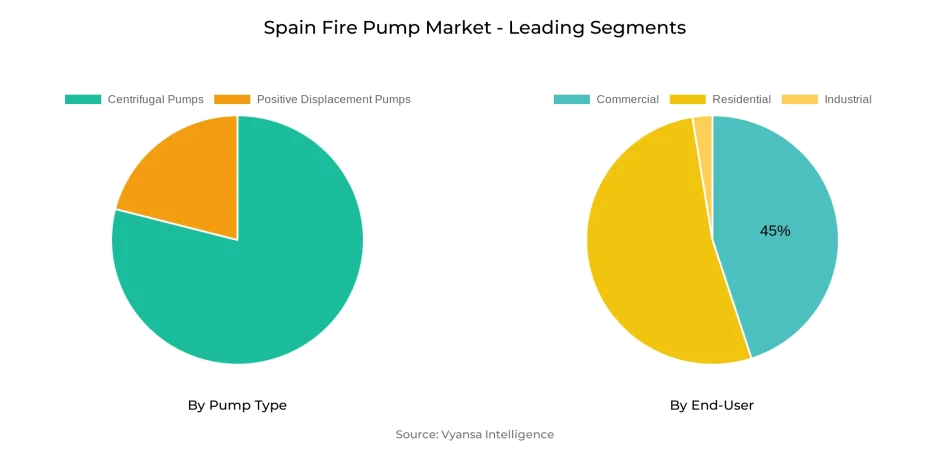

- Centrifugal Pumps continues to dominate the market.

- Competition

- More than 10 companies are actively engaged in producing Fire Pump in Spain.

- Top 5 companies acquired the maximum share of the market.

- WILO SE, Ebara Corporation, ITT Goulds Pumps, Flowserve Corporation, Pentair PLC etc., are few of the top companies.

- End-User

- Commercial grabbed 45% of the market.

Spain Fire Pump Market Outlook

The Spain Fire Pump Market worth USD 45 million as of 2025 is expected to grow to USD 65 million by 2032 at a CAGR of approximately 5.39% over the period 2026–32. Development is heavily driven by Royal Decree 164/2025, which imposes sophisticated fire protection systems and compulsory sprinkler installations on high-risk industrial buildings. Together with the Technical Building Code (CTE) and Royal Decree 513/2017, this law provides one of the most demanding compliance systems in Europe, guaranteeing steady demand for contemporary and dependable fire pump systems throughout industrial and commercial buildings.

Construction expansion provides additional momentum, with Spain’s sector recording 2% real growth in 2024. With an urbanization rate of 81.8% and a population of 48.6 million, increasing infrastructure and housing projects require robust fire protection. Concurrently, wildfire crises that consumed over 403,000 hectares in 2025 have fueled public safety agendas, propelling industries and municipalities towards reliable fire protection facilities backed by cutting-edge pump technologies.

Technology uptake also influences the market perspective. IoT sensors, live monitoring, and AI-based analytics enhance predictive maintenance and response effectiveness. This is especially seen in Spain's hotel industry, which will have 250 new hotels by 2026, many of them high-end hotels needing smart fire safety systems. Growth in commercial real estate, with USD 14 billion of investment made in 2024, also increases demand, especially in hotels, offices, logistics, and entertainment venues that need high-capacity fire protection systems.

On the basis of type, centrifugal pumps account for the greatest share owing to efficiency, low maintenance, and excellent performance at high-pressure conditions. In end-users, the commercial segment leads with 45% market share, fueled by Spain's service-based economy and high tourism investment. On the other hand, the residential segment is the most rapidly growing segment with a growth of 8.1% CAGR as new constructions and reconstruction implement modern fire protection solutions. Such a blend of commercial leadership and housing growth gives a balanced growth trend to Spain's fire pump market.

Spain Fire Pump Market Growth Driver

Regulatory Environment Strengthens Market Expansion

Spain Fire Pump Market is witnessing fast-tracked growth in the wake of Royal Decree 164/2025, effective from May 10, 2025. The law demands sophisticated fire safety installations, classifying industrial units into risk categories and necessitating automatic sprinkler installations for high and very high-risk locations. The decree fills out current frameworks, such as the Technical Building Code (CTE) and Royal Decree 513/2017, establishing one of the most stringent regulatory fire protection environments in Europe. These overarching standards force investment in fire pumps on both industrial and commercial sites.

Spain's building sector further augments demand, growing by 2% in real terms in 2024 and set to grow at an average annual rate of 3% for the period 2025–2028. At a rate of urbanization of 81.8% and a population base of 48.6 million, Spain's expanding urban infrastructure necessitates strong safety provisions. This growth heightens the importance of dependable fire pump systems to sustain Spain's contemporary development and safety agenda.

Spain Fire Pump Market Challenge

Regulatory Complexity and Environmental Pressures

The Spain Fire Pump Market is threatened by the multi-layered regulatory environment of the country. The combination of Royal Decree 164/2025 with previous systems like the Technical Building Code (DB-SI) and Royal Decree 513/2017 results in intricate, facility-specific compliance. For industrial facilities, requirement for compulsory dynamic simulations of crowd movement and smoke propagation as part of evacuation planning adds cost and technicality. This climate requires sophisticated knowledge and lengthens project implementation periods, especially in large-scale development projects.

Pressures from the environment compound these issues, with Spain suffering unprecedented wildfire destruction in 2025. Over 403,000 hectares have been torched this year, 111,916 hectares in 38 recent blazes, as recorded by the European Forest Fire Information System. This disaster has spurred regulatory tightening and reinforced calls for robust fire protection infrastructure. The government's deployment of over 3,600 firefighters during the emergency underscores the importance of efficient fire pump systems despite growing pressure on public and private resources.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Fire Pump Market Trend

Smart Technologies Transform Safety Standards

Technical innovation is transforming the Spain Fire Pump Market, especially in terms of the incorporation of IoT sensors, real-time observation, and AI-based analytics. All these solutions enhance detection, suppression, and system reliability and become more crucial to modern-day construction. The emergence of intelligent building management platforms ensures that fire pumps are integrated with other safety systems seamlessly, providing predictive maintenance as well as quicker response times. This technological transformation is especially applicable where there is high-density urbanization, and efficiency in safety is crucial.

Hospitality development further illustrates this trend, with hotel construction and refurbishment expanding by 64.8% in the first quarter of 2024, totaling 412 projects worth €1.96 billion. Approximately 250 new hotels are expected to open by 2026, one-quarter of which are high-end properties concentrated in major tourism hubs. These facilities require advanced fire safety infrastructure, including automated suppression systems and digital monitoring tools. As upscale property developments grow, the demand for intelligent, compliant, and sustainable fire pump systems increases proportionally.

Spain Fire Pump Market Opportunity

Expanding Infrastructure and Tourism-Led Prospects

Spain's recovering tourism industry strongly improves demand in the Spain Fire Pump Market. During 2024, 94 million international tourists visited the nation, which yielded revenue of €126 billion, up 16% year on year. Tourism's contribution to GDP stood at close to €249 billion, with forecasts inclining toward €260 billion in 2025. This boom has driven enormous investments in hotels, resorts, and leisure complexes, all needing sophisticated fire protection infrastructure to ensure rigorous safety standards and safeguard increasing numbers of visitors.

Commercial real estate expansion also aids market growth, with overall investment volumes hitting €14 billion in 2024. Hotel holdings contributed €3.2 billion of activity and made hospitality the second most appealing real estate asset category for investors. Logistics properties are also experiencing strong momentum, growing consistently across Spain's major markets. This dual surge in tourist-driven infrastructure and business growth identifies significant expansion opportunities for fire pump systems, which are critical to protecting these new, high-capacity structures.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Fire Pump Market Segmentation Analysis

By Pump Type

- Centrifugal Pumps

- Positive Displacement Pumps

Among pump types, centrifugal pumps hold the largest share in the Spain Fire Pump Market because of their established reliability, affordability, and suitability for large-scale fire protection systems. Centrifugal pumps have the highest capacity for consistent flow and pressure, thus making them a necessity for high-rise structures, industrial buildings, and business complexes. Their ease of maintenance and wide compatibility with building management systems make them the first choice for new as well as retrofit installations in the country.

The adoption of centrifugal pumps aligns closely with Spain’s stringent regulations, including Royal Decree 164/2025, which mandates automatic sprinkler systems in high and very high-risk industrial facilities. With Spain’s commercial real estate investment reaching €14 billion in 2024, demand for these pumps is expected to expand steadily across logistics, office, and hospitality properties. Their robust performance in high-pressure environments and technological adaptability reinforces centrifugal pumps as the backbone of Spain’s evolving fire protection infrastructure.

By End-User

- Residential

- Commercial

- Industrial

Commercial sectors have the largest percentage in Spain Fire Pump Market, meeting 45% of demand. This is a testimony to Spain's service-oriented economy where 76% of GDP comes from services and tourism alone generates billions annually in investment. Hotels, offices, and retail malls increasingly incorporate complete fire protection systems in accordance with the Technical Building Code as well as recently tightened industrial safety standards. The magnitude of hotel investments, totaling over €3.2 billion in 2024, reflects commercial leadership in the adoption of fire pumps.

The residential segment directly is the fastest-growing end-user segment, growing at a CAGR of 8.1%. On-going urbanization, underpinned by Spain's 81.8% urban populace rate, and increased housing construction drive steady demand. With average annual construction growth forecast at 3% between 2028, new housing and renovation schemes necessitate contemporary fire protection improvements. This twin dynamic of commercial primacy and residential acceleration underlines the balanced yet growing base of demand for Spain's fire pump market.

Top Companies in Spain Fire Pump Market

The top companies operating in the market include WILO SE, Ebara Corporation, ITT Goulds Pumps, Flowserve Corporation, Pentair PLC, Sulzer Limited, Grundfos Holding A/S, KSB SE & Co. KGaA, Patterson (Gorman Rupp), Armstrong, etc., are the top players operating in the Spain Fire Pump Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Spain Fire Pump Market Policies, Regulations, and Standards

4. Spain Fire Pump Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Spain Fire Pump Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Pump Type

5.2.1.1. Centrifugal Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1.1. Overhung Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1.2. Vertical Inline- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1.3. Horizontal End Suction- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Split Case Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.1. Single/Two Stage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.2. Multi Stage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Positive Displacement Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Diaphragm Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Piston Pumps - Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Mode of Operation

5.2.2.1. Diesel Fire Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Electric Fire Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By End-User

5.2.3.1. Residential- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Commercial- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Industrial- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. Spain Centrifugal Fire Pump Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Mode of Operation- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By End-User- Market Insights and Forecast 2022-2032, USD Million

7. Spain Positive Displacement Fire Pump Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Mode of Operation- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By End-User- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Flowserve Corporation

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Pentair PLC

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.Sulzer Limited

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Grundfos Holding A/S

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.KSB SE & Co. KGaA

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.WILO SE

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.Ebara Corporation

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.ITT Goulds Pumps

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Patterson (Gorman Rupp)

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. Armstrong

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Pump Type |

|

| By Mode of Operation |

|

| By End-User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.