Spain Dog Food Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Wet Dog Food, Dry Dog Food, Treats and Mixers), By Nature (Organic, Monoprotein, Conventional), By Ingredient (Animal Derivatives, Plant Derivatives), By Pet Type (Kitten/Pup, Adult, Senior), By Pricing (Economy, Mid-Priced, Premium), By Packaging (Pouches, Bags, Folding Cartons, Tubs & Cups, Can, Bottles & Jars), By Sales Channel (Retail Channels, Non-Retail Channels) ... Read more

|

Major Players

|

Spain Dog Food Market Statistics and Insights, 2026

- Market Size Statistics

- Dog Food in Spain is estimated at $ 1.52 Billion.

- The market size is expected to grow to $ 1.65 Billion by 2032.

- Market to register a CAGR of around 1.18% during 2026-32.

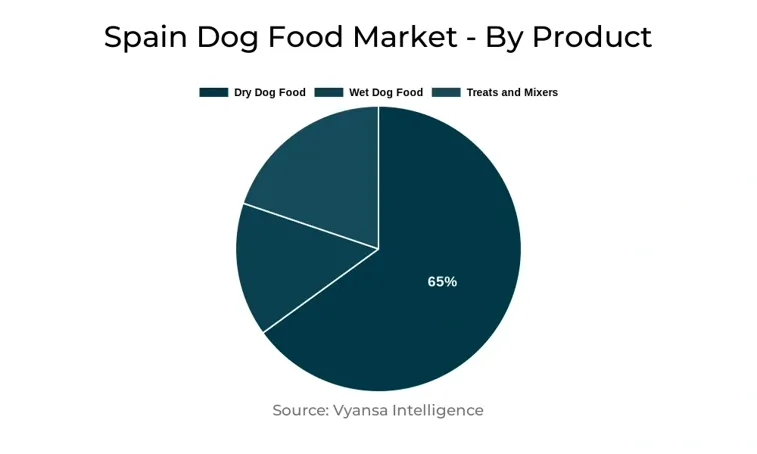

- Product Shares

- Dry Dog Food grabbed market share of 65%.

- Competition

- More than 20 companies are actively engaged in producing Dog Food in Spain.

- Top 5 companies acquired 50% of the market share.

- Hill's Pet Nutrition España SL, Carrefour SA, Dibaq-Diproteg SA, Affinity Petcare SA, Mercadona SA etc., are few of the top companies.

- Sales Channel

- Retail Channels grabbed 90% of the market.

Spain Dog Food Market Outlook

The dog food market in Spain is forecast to record steady current value growth between 2025-2030, driven by the premiumisation trend and sustained pet humanisation. Although inflation pressures are decelerating, elevated prices in 2025 have impacted on consumer behavior, with some price-conscious pet owners opting for home-prepared diets or leftovers. Nevertheless, static dog population numbers—alongside growing demand for small breeds—are stimulating demand for premium products. Super-premium wet food, enjoying success among small dogs, puppies, and older animals, will develop more rapidly than dry food. The natural ingredients and "real food" trends will continue to power innovation and brand differentiation.

Competition in retail will become more intense, with supermarkets holding the bulk but coming under increasing pressure from discounters such as Lidl and Aldi, which are building store chains and premium private label lines. Online sales will take an increasing share of distribution, stimulated by convenience, increased choice of product, and younger dog owners' tendency to shop online. Hybrid retail business models bringing together bricks and clicks will grow in significance for industry players.

Product innovation will continue to be a growth driver, with the brands moving into functional, health-oriented treats, therapeutic diets, and small breed formats. Companies are addressing specific health challenges like digestive, urinary, and weight care through specialty formulas. Mini sizes and on-the-go snacks will also become popular as owners take pets out more frequently.

Overall, the growth of the market will be driven by increasing demand for premium, natural, and functional products, growth in omnichannel retailing, and the ongoing evolution of brands to meet changing consumers' preferences. Volume growth might stay constrained because of stable dog population, but value sales will be boosted by trading up to more expensive, specialist products.

Spain Dog Food Market Growth Driver

The pet humanisation keeps driving demand for high-quality dog food with natural ingredients and health benefits. More and more pet owners in Spain opt for less processed, more natural diets for themselves and look for the same quality for their dogs. This creates a demand to introduce new products. Arquivet releases Fresh Arquivet wet dog food for small breeds with natural, gluten-free formulas and no artificial additives. Dingonatura enlarges its Natura Diet pâté line and Natura Vet therapeutic wet food with new puppy, adult, and weight control recipes.

Mini sizes are on the rise, appealing to small breeds and the increasingly busy life, as Spaniards increasingly take their dogs along. This drives demand for healthy, convenient snacks. Pet Snack Company introduces functional varieties to its snack ranges, YowUp! introduces lactose-free functional milk for cats and dogs, and Dibaq Petcare features natural, functional snacks addressing particular health concerns.

Spain Dog Food Market Opportunity

The therapeutic dog food segment is poised to provide significant growth opportunities as pet owners increasingly take proactive measures to monitor their dogs' health through specialized nutrition. With increased attention toward identifying and treating specific health issues, premium formulas approved by vets will become increasingly in demand. Digestive and urinary health will remain an ongoing driver of sales, prompting manufacturers to invest in specialized product development.

This transition will provide opportunities for businesses to broaden their product base with tailored solutions. Recent instances include Royal Canin's Fibre Response and Gastrointestinal Low Fat Small Dogs, which cater to specific digestive requirements, and Calibra's products for gastrointestinal and pancreatic well-being. With increasing owners wanting diets that fit their dogs' medical history, those players addressing this need will be in a strong position to gain market share and drive long-term growth.

Unlock Market Intelligence

Explore the market potential with our data-driven report

| Report Coverage | Details |

|---|---|

| Market Forecast | 2026-32 |

| USD Value 2025 | $ 1.52 Billion |

| USD Value 2032 | $ 1.65 Billion |

| CAGR 2026-2032 | 1.18% |

| Largest Category | Dry Dog Food segment leads with 65% market share |

| Top Drivers | Rising Surege in Premium, Natural, and Functional Pet Products Driving Market Growth |

| Top Opportunities | Rising Demand for Specialised Therapeutic Dog Food |

| Key Players | Hill's Pet Nutrition España SL, Carrefour SA, Dibaq-Diproteg SA, Affinity Petcare SA, Mercadona SA, Nestlé Purina PetCare España SA, Mars España Inc y Cía Food SRC, Royal Canin Ibérica SA, Champion Petfoods LP, Schell & Kampeter Inc and Others. |

Unlock Market Intelligence

Explore the market potential with our data-driven report

Spain Dog Food Market Segmentation Analysis

By Sales Channel

- Retail Channels

- Non-Retail Channels

The most important segment in the channel of sales by market share is retail, responsible for approximately half of all dog food sales in Spain. Supermarkets are dominant in this channel, with discounters like Lidl and Aldi growing steadily. Lidl has made pet care its top priority and has extended its product range and opened 50 new outlets to reach a total of 700 stores. Aldi is expanding too, with 40 new stores planned for 2025, increasing its size to 500. Competitive prices, one-stop shop, and increased fresh food are all helping to drive discounters' success.

Warehouse clubs are still a niche but growing more rapidly than nearly all others, with Costco's success leading the charge. E-commerce is growing at a speedier rate as well, providing customers with wider product selection, price comparison, and convenience. With increasing digitalisation, pet stores and food retailers are incorporating online sales as part of omnichannel strategies to ensure a frictionless experience.

Top Companies in Spain Dog Food Market

The top companies operating in the market include Hill's Pet Nutrition España SL, Carrefour SA, Dibaq-Diproteg SA, Affinity Petcare SA, Mercadona SA, Nestlé Purina PetCare España SA, Mars España Inc y Cía Food SRC, Royal Canin Ibérica SA, Champion Petfoods LP, Schell & Kampeter Inc, etc., are the top players operating in the Spain Dog Food Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Spain Dog Food Market Policies, Regulations, and Standards

4. Spain Dog Food Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Spain Dog Food Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.1.2.By Quantity Sold in Kilo Tons

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product

5.2.1.1. Wet Dog Food- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Dry Dog Food- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Treats and Mixers- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Monoprotein- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Ingredient

5.2.3.1. Animal Derivatives- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Plant Derivatives- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Pet Type

5.2.4.1. Kitten/Pup- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Adult- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Senior- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Pricing

5.2.5.1. Economy- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Mid-Priced- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Packaging

5.2.6.1. Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Folding Cartons- Market Insights and Forecast 2022-2032, USD Million

5.2.6.4. Tubs & Cups- Market Insights and Forecast 2022-2032, USD Million

5.2.6.5. Can- Market Insights and Forecast 2022-2032, USD Million

5.2.6.6. Bottles & Jars- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Sales Channel

5.2.7.1. Retail Channels- Market Insights and Forecast 2022-2032, USD Million

5.2.7.1.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.7.1.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2. Non-Retail Channels- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2.1. Veterinary Clinics- Market Insights and Forecast 2022-2032, USD Million

5.2.8.By Competitors

5.2.8.1. Competition Characteristics

5.2.8.2. Market Share & Analysis

6. Spain Wet Dog Food Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.1.2.By Quantity Sold in Kilo Tons

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Ingredient- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Pet Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Pricing- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Packaging- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Spain Dry Dog Food Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.1.2.By Quantity Sold in Kilo Tons

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Ingredient- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Pet Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Pricing- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Packaging- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Spain Treats and Mixers Dog Food Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.1.2.By Quantity Sold in Kilo Tons

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Ingredient- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Pet Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Pricing- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Packaging- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Affinity Petcare SA

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Mercadona SA

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Nestlé Purina PetCare España SA

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Mars España Inc y Cía Food SRC

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Royal Canin Ibérica SA

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Hill's Pet Nutrition España SL

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Carrefour SA

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Dibaq-Diproteg SA

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Champion Petfoods LP

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Schell & Kampeter Inc

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Nature |

|

| By Ingredient |

|

| By Pet Type |

|

| By Pricing |

|

| By Packaging |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.