South Africa Dog Food Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Wet Dog Food, Dry Dog Food, Treats and Mixers), By Nature (Organic, Monoprotein, Conventional), By Ingredient (Animal Derivatives, Plant Derivatives), By Pet Type (Kitten/Pup, Adult, Senior), By Pricing (Economy, Mid-Priced, Premium), By Packaging (Pouches, Bags, Folding Cartons, Tubs & Cups, Can, Bottles & Jars), By Sales Channel (Retail Channels, Non-Retail Channels) ... Read more

|

Major Players

|

South Africa Dog Food Market Statistics and Insights, 2026

- Market Size Statistics

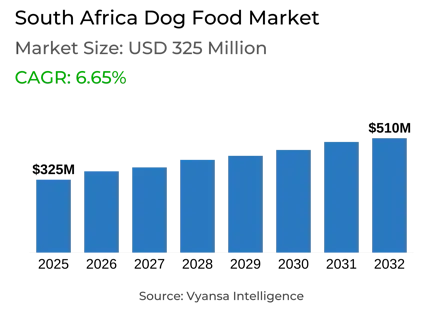

- Dog Food in South Africa is estimated at $ 325 Million.

- The market size is expected to grow to $ 510 Million by 2032.

- Market to register a CAGR of around 6.65% during 2026-32.

- Product Shares

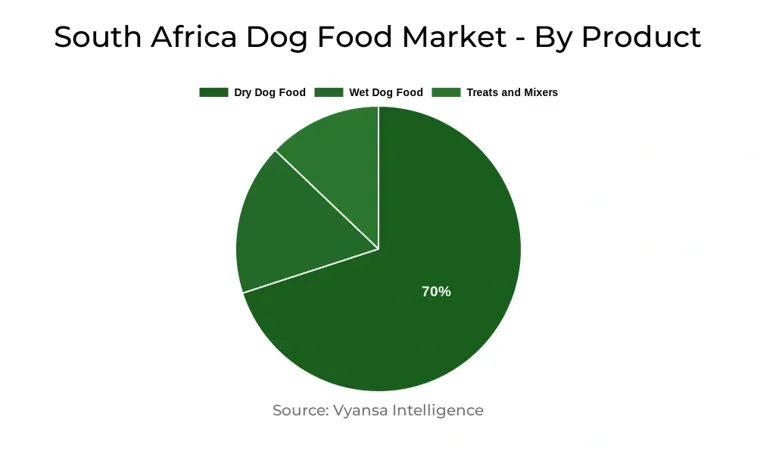

- Dry Dog Food grabbed market share of 70%.

- Dry Dog Food to witness a volume CAGR of around 3.92%.

- Competition

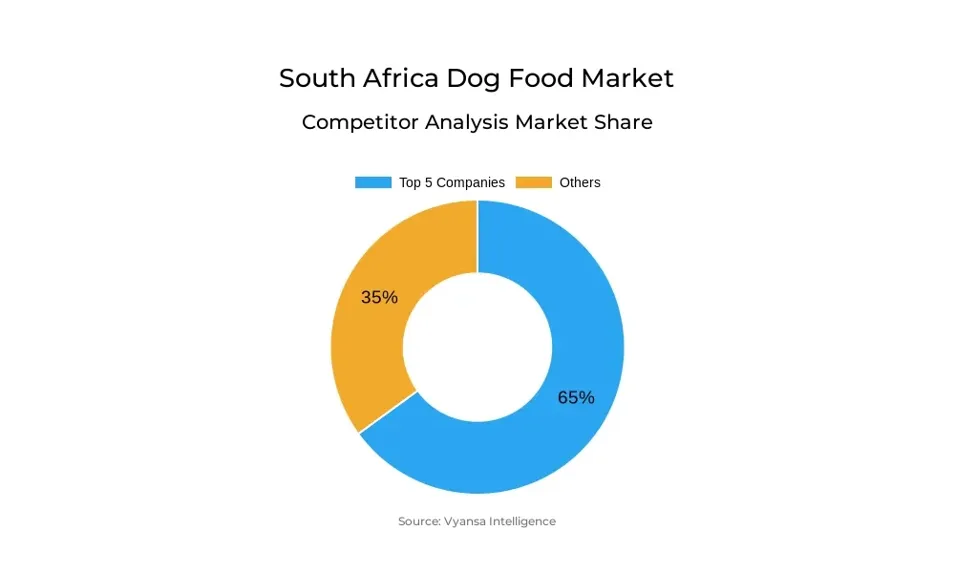

- More than 10 companies are actively engaged in producing Dog Food in South Africa.

- Top 5 companies acquired 65% of the market share.

- Hill's Pet Nutrition Inc, Promeal (Pty) Ltd, Cube Route Pty Ltd, RCL Foods Ltd, Martin & Martin (Pty) Ltd etc., are few of the top companies.

- Sales Channel

- Retail Channels grabbed 75% of the market.

South Africa Dog Food Market Outlook

The South Africa dog food market is anticipated to witness stable growth during the forecast period on the back of an expanding population of dogs and increased pet adoption, primarily in urban regions. Not only is urbanisation boosting the number of prospective pet owners but also changing consumer preferences for processed, high-value, and specialty dog food. Safely stabilising inflation and interest rates are making for a more conducive economic environment, allowing more households to afford pet care spending. Less loadshedding is also increasing the efficiency of production, guaranteeing regular supply to match demand.

Dry dog food will remain the top seller, especially the economy one, as it is affordable and worth its price. Though premiumisation is on the increase, there is still budget limitation among many consumers, meaning low-cost dry versions are the most sought after. Mid-range and premium canned dog food are projected to expand from a small base as pet humanisation and pet health knowledge grow, with more owners ready to invest in improved nutrition when able.

RCL Foods will continue its market leadership with established brands like Bobtail and Canine Cuisine targeting both the economy-conscious and mid-range segments. Supermarkets will be the primary distribution channel, but cost-of-living forces will encourage some to use alternative buying techniques, including specialist stores and online shopping. Internet sales will achieve the most vigorous growth, as shoppers enjoy subscription deliveries and convenient price comparisons.

Sustainable production will also be a prime emphasis, with manufacturers investing in solar panels, energy efficiency, and products providing health benefits like high protein and immune system enhancement. Nevertheless, ongoing poverty and unemployment will persist to restrict total market potential, keeping the economy dry dog food category the most resilient and most consumed.

South Africa Dog Food Market Growth Driver

Demand for dog food keeps increasing, backed by growing economic stability, which increases consumer confidence and purchasing power. Growing urbanisation is driving the number of pet owners in urban areas, while pet humanisation and premiumisation become stronger trends. Increasing numbers of owners are considering their dogs to be family members and opting for premium, specialist products. Increasing concern for pet health and wellbeing further supports spending on improved nutrition, with mid-range and premium wet dog food experiencing especially good growth prospects.

Though ongoing issues like widespread poverty, joblessness, and low household incomes constrain the category's complete potential, they are slowly improving. They are still however inhibiting a part of the population from buying prepared dog food, thus inflicting a definite gap in demand among various income brackets.

South Africa Dog Food Market Opportunity

During 2025-2030, South Africa dog food manufacturers will expand investment in green manufacturing strategies. Most stakeholders will focus on being more energy independent through initiatives like solar and energy-efficient technologies. These measures will assist manufacturers in keeping production costs affordable while providing continuous operations during loadshedding, facilitating sustainable business stability.

Meanwhile, businesses will concentrate on developing better dog food for enhancing pets' living conditions. Items with health-related claims such as high protein levels, vitamins, and immune system enhancers will experience increased demand. With the increasing health-consciousness of local consumers, high-spending consumers will pay extra for products that provide better health benefits for their pets, thus spurring growth in the premium sector.

Unlock Market Intelligence

Explore the market potential with our data-driven report

| Report Coverage | Details |

|---|---|

| Market Forecast | 2026-32 |

| USD Value 2025 | $ 325 Million |

| USD Value 2032 | $ 510 Million |

| CAGR 2026-2032 | 6.65% |

| Largest Category | Dry Dog Food segment leads with 70% market share |

| Top Drivers | Rising Consumer Confidence and Lifestyle Shifts Propel Demand Market Growth |

| Top Opportunities | Rising Focus on Sustainable Production and Pet Health |

| Key Players | Hill's Pet Nutrition Inc, Promeal (Pty) Ltd, Cube Route Pty Ltd, RCL Foods Ltd, Martin & Martin (Pty) Ltd, Montego Pet Nutrition (Pty) Ltd, Mars Africa (Pty) Ltd, Afrique Pet Food (Pty) Ltd, Gourmet Pet Industries (Pty) Ltd, Marltons Pets & Products (Pty) Ltd and Others. |

Unlock Market Intelligence

Explore the market potential with our data-driven report

South Africa Dog Food Market Segmentation Analysis

By Sales Channel

- Retail Channels

- Non-Retail Channels

The most popular market segment under the channel of sales is retail, dominated by supermarkets. They are popular due to the ease of purchasing a whole variety of products at one stop. This channel, however, has been impacted by increasing cost of living and decreased consumer spending, and some shoppers have reduced the amount of dog food they purchase at supermarkets.

Specialist channels like veterinary clinics and e-commerce are gaining the attention of premium dog food consumers. Such channels provide high-quality, well-chosen products, professional guidance, and individual service. E-commerce is growing especially quickly, backed by the involvement of large supermarkets and veterinary clinics. It is valued for easy price and product comparison and regular home delivery by consumers, making this channel the main driver of future growth in sales.

Top Companies in South Africa Dog Food Market

The top companies operating in the market include Hill's Pet Nutrition Inc, Promeal (Pty) Ltd, Cube Route Pty Ltd, RCL Foods Ltd, Martin & Martin (Pty) Ltd, Montego Pet Nutrition (Pty) Ltd, Mars Africa (Pty) Ltd, Afrique Pet Food (Pty) Ltd, Gourmet Pet Industries (Pty) Ltd, Marltons Pets & Products (Pty) Ltd, etc., are the top players operating in the South Africa Dog Food Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. South Africa Dog Food Market Policies, Regulations, and Standards

4. South Africa Dog Food Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. South Africa Dog Food Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.1.2.By Quantity Sold in Kilo Tons

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product

5.2.1.1. Wet Dog Food- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Dry Dog Food- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Treats and Mixers- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Monoprotein- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Ingredient

5.2.3.1. Animal Derivatives- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Plant Derivatives- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Pet Type

5.2.4.1. Kitten/Pup- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Adult- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Senior- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Pricing

5.2.5.1. Economy- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Mid-Priced- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Packaging

5.2.6.1. Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.6.2. Bags- Market Insights and Forecast 2022-2032, USD Million

5.2.6.3. Folding Cartons- Market Insights and Forecast 2022-2032, USD Million

5.2.6.4. Tubs & Cups- Market Insights and Forecast 2022-2032, USD Million

5.2.6.5. Can- Market Insights and Forecast 2022-2032, USD Million

5.2.6.6. Bottles & Jars- Market Insights and Forecast 2022-2032, USD Million

5.2.7.By Sales Channel

5.2.7.1. Retail Channels- Market Insights and Forecast 2022-2032, USD Million

5.2.7.1.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.7.1.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2. Non-Retail Channels- Market Insights and Forecast 2022-2032, USD Million

5.2.7.2.1. Veterinary Clinics- Market Insights and Forecast 2022-2032, USD Million

5.2.8.By Competitors

5.2.8.1. Competition Characteristics

5.2.8.2. Market Share & Analysis

6. South Africa Wet Dog Food Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.1.2.By Quantity Sold in Kilo Tons

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Ingredient- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Pet Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Pricing- Market Insights and Forecast 2022-2032, USD Million

6.2.5.By Packaging- Market Insights and Forecast 2022-2032, USD Million

6.2.6.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. South Africa Dry Dog Food Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.1.2.By Quantity Sold in Kilo Tons

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Ingredient- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Pet Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Pricing- Market Insights and Forecast 2022-2032, USD Million

7.2.5.By Packaging- Market Insights and Forecast 2022-2032, USD Million

7.2.6.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. South Africa Treats and Mixers Dog Food Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.1.2.By Quantity Sold in Kilo Tons

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Ingredient- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Pet Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Pricing- Market Insights and Forecast 2022-2032, USD Million

8.2.5.By Packaging- Market Insights and Forecast 2022-2032, USD Million

8.2.6.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.RCL Foods Ltd

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Martin & Martin (Pty) Ltd

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Montego Pet Nutrition (Pty) Ltd

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Mars Africa (Pty) Ltd

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Afrique Pet Food (Pty) Ltd

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Hill's Pet Nutrition Inc

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Promeal (Pty) Ltd

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Cube Route Pty Ltd

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Gourmet Pet Industries (Pty) Ltd

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Marltons Pets & Products (Pty) Ltd

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Nature |

|

| By Ingredient |

|

| By Pet Type |

|

| By Pricing |

|

| By Packaging |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.