Saudi Arabia Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade), By Region (East, West, South, Central) ... Read more

|

Major Players

|

Saudi Arabia Juice Market Statistics and Insights, 2026

- Market Size Statistics

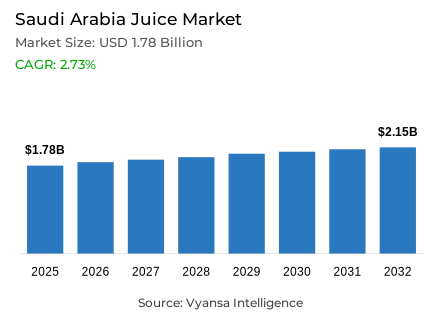

- Juice market size in Saudi Arabia was estimated at USD 1.78 billion in 2025.

- The market size is expected to grow to USD 2.15 billion by 2032.

- Market to register a CAGR of around 2.73% during 2026-32.

- Category Shares

- Nectars grabbed market share of 65%.

- Competition

- More than 10 companies are actively engaged in producing juice in Saudi Arabia.

- Top 5 companies acquired around 70% of the market share.

- Al Othman Agricultural & Processing Co, Al Safi Danone Ltd, National Agricultural Development Co (NADEC), Almarai Co Ltd, Al Rabie AlSaudia Dairy Co Ltd etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 75% of the market.

Saudi Arabia Juice Market Outlook

The Saudi Arabia juice market is experiencing a positive shift, which is driven by the government initiative of Vision 2030 to encourage active lifestyles and prevent obesity. The market is estimated to be USD 1.78 billion in 2025, and is expected to reach USD 2.15 billion in 2032, with a CAGR of about 2.73% in the 2026-32 forecast period. This gradual expansion is mostly supported by the fact that the country has a growing tourism market, which is expected to receive more than 100 million tourists every year, and by the fact that the nation is always in need of hydration because of its dry climate.

The pillars of growth are innovation and premiumisation. As a result, nectars have gained a dominant market share of 65%, supported by the perception of being a healthier alternative to traditional juice beverages. end user are shifting towards products with low juice content (up to 24%) to cold-pressed, organic, and functional products with immune boosters. This is especially noticeable during Ramadan, when large family-sized portions are sold in large volumes, and the back-to-school season, which drives the demand of small, convenient formats.

Almarai, the market leader, remains dominant through heavy investments in sustainable operations and high-end sub-brands like Select by Farm. However, the competition is increased by international fresh-juice bars such as Jamba Juice that responds to the need of natural ingredients. In order to stay competitive, packaged juice producers are focusing on environmentally friendly packaging and clean-label transparency, including No Preservatives claims, to match the values of environmentally and health-conscious end user.

sales channel is still deeply entrenched in retail, and off-trade channels constitute 75% of the market. Supermarkets are the most common outlet because they have a wide variety of products and they are very aggressive in their promotions. However, the online world is evolving at a fast pace; e-commerce and discounts are the most vibrant mediums, which attract younger and more technologically advanced end user with online-only offers and expedited delivery. This omnichannel strategy will be critical to players who want to maintain a competitive edge up to 2032.

Saudi Arabia Juice Market Growth DriverExcise-Led Sugar Reduction Policies Accelerating Health-Oriented Juice Demand

The efforts of Saudi Arabia as part of Vision 2030, along with the public awareness campaigns, create a preference towards lower-sugar as a decisive factor in end user purchasing behavior in 2026. With end user becoming more and more determined to reduce their sugar intake, brands that position juice as a healthier daily drink gain traction, a phenomenon that is particularly strong in a region where hydration is an ongoing need because of the constantly hot weather. Nutrition education programmes and public health initiatives, in turn, maintain end user focus on sugar content as a key factor in choosing beverages.

This behavioural change is further cemented by regulatory measures. The Zakat, Tax and Customs Authority (ZATCA) has decided that the excise tax on sweetened beverages and sweetened juice beverages will be 50% of the current tax, which will directly affect the price and force the reformulation of the product to contain less added sugar to maintain the open disclosure of both end user and manufacturers. This fiscal tool offers strong economic incentives to reformulate to naturally sweetened or reduced-sugar formulations. Thus, the intersection of social health consciousness and punitive taxation of sweetened drinks creates structural demand benefits of naturally positioned, low-sugar juice substitutes that are consistent with national wellness goals and the current health awareness of end user.

Saudi Arabia Juice Market ChallengeExpanding Fresh-Prepared Alternatives Diluting Packaged Juice Occasions

Packaged juice is confronted with a formidable headwind health-aware end user are increasingly moving towards fresh, more natural juice options, which is supported by the growth of fresh-juice bars and global smoothie and juice franchises. This change creates high levels of substitution effects; packaged products need to strive harder to prove their worth in comparison with made-to-order products that promise freshness and simplicity. The perceived benefits of fresh preparation therefore create competitive pressure on packaged formats and differentiated positioning strategies are required.

The fact that this pressure is not theoretical but real is supported by macro activity. The wholesale and retail trade, restaurants and hotels market grew by 6.6% year-on-year in the second quarter of 2025, indicating a strong out-of-home ecosystem where fresh-beverage operators have the opportunity to take over the occasions previously served by packaged juice. This growth in the food-service market allows fresh-juice operators to scale sales channels and end user touchpoints quickly. The overlapping of end user demands of freshness and the robust expansion of the food-service market therefore exerts a long-term competitive pressure on packaged juice, requiring it to innovate in convenience, premium positioning, and perceived naturalness to maintain its relevance in comparison with fresh-prepared substitutes.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Saudi Arabia Juice Market TrendClean-Label and Reduced-Sugar Positioning Becoming Competitive Baseline Expectations

End user no longer tolerate ordinary juice; they now reward products that are perceived to have better quality and more transparency, with clean labels, few additives and better ingredient perceptions. This repositioning changes brand competition to focus not on flavour but on trust signals so that products can approximate real fruit and better-for-you positioning. In this way, the expectations of premium clean-label become more of a category entry requirement than a differentiation opportunity, increasing the minimum quality standards in the market.

This trend is strengthened by regulation that maintains vigilance on sugar content and sweetening agents. The structure of ZATCA levies a 50% excise duty on sweetened juice drinks, which makes the positioning of no added sugar / less sugar commercially relevant, but not just rhetorical. This financial strain makes sure that clean-label and premium cues will remain salient until 2026 and further. Health positioning regulatory support creates long-term competitive advantages to brands that exhibit authentic ingredient transparency, low processing, and natural sweetness profiles. The clean-label trend, therefore, represents a category shift to premium positioning as the new end user expectation in the health-conscious, regulation-based beverage environment in Saudi Arabia.

Saudi Arabia Juice Market OpportunityTourism Expansion Broadening Hydration Occasions Across Retail and Hospitality Channels

Tailwinds of demand are created by tourism development and large-scale events the more visitors and days of activity, the higher the need states of refreshment, convenience, and hydration. In the case of juice manufacturers, this increases consumption occasions beyond the normal household consumption- especially where end user want quick, portable, health-positioned drinks. The growth of tourism creates demand pools that can be addressed without relying on the conventional retail outlets, thus facilitating the growth of the category by the hospitality and convenience-based formats.

This opportunity is supported by measurable expansion of tourism capacity. According to GASTAT, the number of licensed tourism hospitality facilities is 5,622 in Q3 2025 (up 40.6% year-on-year) and the average hotel room occupancy rate is 49.1%, which is a scaling visitor ecosystem that expands potential touchpoints to purchase packaged juice. Hotel, restaurant, and tourism development provides sales channels in food-service and convenience-based retail formats that meet the needs of visitors. The demand of tourism allows the brands to seize incremental occasions through single-serve formats, premium positioning, and convenience-based placement strategies that match the visitor consumption trends and hospitality channel needs in the fast-growing tourism infrastructure in Saudi Arabia.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Saudi Arabia Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the Saudi Arabia juice market, where Nectars grabbed a market share of 65%. This segment has become the primary beneficiary of the country's sugar tax and health-driven regulations, as many manufacturers have reformulated their traditional juice drinks into nectars to offer a more "natural" profile. With a juice content ranging from 25% to 99%, nectars appeal to families who seek better nutritional value without the premium price tag of 100% pure juice.

While nectars dominate, the market is also seeing a rapid rise in niche categories like coconut water and exotic fruit blends. Younger end user are increasingly experimenting with flavors like passionfruit and strawberry mixes, moving away from classic orange and apple. As the forecast period progresses, the nectar segment is expected to maintain its lead by incorporating functional ingredients such as vitamins and antioxidants, further cementing its position as a health-oriented staple for the Saudi Arabia population.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 75% of the market. Retail dominance is driven by the sheer scale of modern supermarkets and hypermarkets, which offer the extensive chiller space necessary for a wide range of juice brands and premium organic lines. These large-format stores remain the preferred destination for planned household shopping, especially for family-sized multipacks that see high demand during cultural periods like Ramadan and the summer months.

Despite the lead of physical retail, the sales landscape is being disrupted by the rapid growth of e-commerce and discounters. With over 600 discounters now operating in the Kingdom, value-conscious shoppers are increasingly moving away from traditional grocers. Simultaneously, the younger generation is flocking to online platforms for the convenience of home delivery and digital-only promotions. While the off-trade sector will continue to hold the vast majority of the market, the shift toward these high-growth digital and discount channels will redefine how brands reach end user in Saudi Arabia by 2032.

List of Companies Covered in Saudi Arabia Juice Market

The companies listed below are highly influential in the Saudi Arabia juice market, with a significant market share and a strong impact on industry developments.

- Al Othman Agricultural & Processing Co

- Al Safi Danone Ltd

- National Agricultural Development Co (NADEC)

- Almarai Co Ltd

- Al Rabie AlSaudia Dairy Co Ltd

- Aujan Industries Co Ltd

- Binzagr Lever Ltd (Unilever Arabia)

- Gulf Union Foods Co

- Abuljadayel Beverages Industries Llc

- Al Manhal Water Factory

Competitive Landscape

Saudi Arabia juice market is led by Almarai, which укрепed its dominance through a diversified portfolio spanning no added sugar lines and premium Farm’s Select offerings, backed by significant investment aligned with Vision 2030. Al Rabie and Suntop are key challengers, competing closely in nectars and 100% juice, with Suntop recording the strongest growth, while KDD advances through quality positioning. Competitive intensity is rising as smaller players lose share. Category dynamics favour coconut water and nectars, while low juice content drinks decline under sugar tax and health scrutiny. Indirect competition from fresh juice chains such as Jamba Juice is intensifying. Differentiation opportunities centre on reduced sugar reformulation, functional fortification, exotic flavour innovation, sustainable packaging, and targeted seasonal marketing around Ramadan and tourism.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Saudi Arabia Juice Market Policies, Regulations, and Standards

- Saudi Arabia Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Saudi Arabia Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Region

- East

- West

- South

- Central

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Saudi Arabia 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Saudi Arabia Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Saudi Arabia Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Saudi Arabia Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Saudi Arabia Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Almarai Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Rabie AlSaudia Dairy Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aujan Industries Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Binzagr Lever Ltd (Unilever Arabia)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gulf Union Foods Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Othman Agricultural & Processing Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Safi Danone Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- National Agricultural Development Co (NADEC)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Abuljadayel Beverages Industries LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Manhal Water Factory

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Almarai Co Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.