Guatemala Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

Guatemala Juice Market Statistics and Insights, 2026

- Market Size Statistics

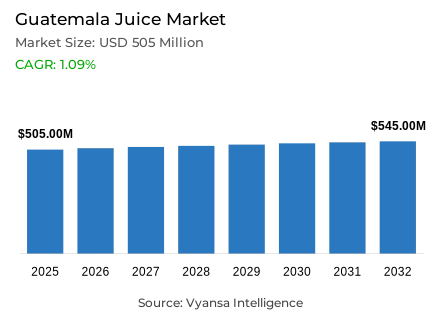

- Juice market size in Guatemala was estimated at USD 505 million in 2025.

- The market size is expected to grow to USD 545 million by 2032.

- Market to register a CAGR of around 1.09% during 2026-32.

- Category Shares

- Nectars grabbed market share of 45%.

- Competition

- More than 10 companies are actively engaged in producing juice in Guatemala.

- Top 5 companies acquired around 80% of the market share.

- Industria Procesadora de Lácteos (Inprolacsa), Jumex Guatemala SA, Alimentos Ideal SA, Alimentos Maravilla SA, Industrias Alimenticias Kern's y Cia SCA etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 90% of the market.

Guatemala Juice Market Outlook

The Guatemala Juice Market is in a stage of small yet sustainable growth as it tries to strike a balance between economic limitations and changing health perceptions. The market is estimated to grow to USD 505 million in 2025 and USD 545 million in 2032 with a CAGR of about 1.09% in the 2026-2032 forecast period. Although many adults perceive juice as a rare morning drink due to sugar concerns, it remains a dietary staple among children and a highly appreciated, low-cost source of nutrition among the general population.

Affordability is a significant market stability factor. For many Guatemalan families, family packs of 3-liter and gallon bottles are cost-effective ways to incorporate fruit-flavoured drinks into daily meals. Major competitors such as Alimentos Maravilla SA and Coca-Cola de Guatemala SA leverage this by providing a large range of formats, including innovative returnable 500 ml glass bottles of the Del Valle brand, keeping prices low and accessible to low-income consumers.

Innovation is becoming more functional and occasion-driven. To compete with rising popularity of isotonic beverages and ready-to-drink teas, juice brands are moving toward on-the-go hydration positioning. There are increasing prospects for juices infused with plant extracts or light coconut waters focused on quick rehydration features. The market is shifting toward specialized health claims such as no preservatives or natural juice, reconnecting with younger, health-conscious consumers seeking functional alternatives to traditional sweetened beverages.

The distribution landscape remains community-rooted while modernising rapidly. Off-trade outlets still control total sales, but convenience stores such as Super 24 and Express are growing faster than traditional grocers. These newer stores offer longer hours and broader selections, becoming preferred destinations for urban consumers seeking quick, single-serving items as part of increasingly convenience-oriented lifestyles.

Guatemala Juice Market Growth DriverValue Packs Keep Juice Affordable

Affordability is a fundamental factor in beverage buying behavior maintained by income pressure, thus making juice a viable choice when it is packaged and priced to match daily spending. According to national conditions surveys, 56.0% of the population lives in poverty and 16.2% in extreme poverty, which makes value formats and low-cost purchases important demand drivers of packaged beverages. Structural pressures created by economic constraints give preference to affordable beverage options, and thus, household nutrition requirements in the context of severely constrained budgets in large segments of the population.

Brands react by focusing on family packs and making them widely available in neighborhood stores. Single-serving and family-sized packages are available to support fast shopping at small local shops and convenience stores, making juice a viable product in many families. Accessible pack formats and ubiquitous retail presence position juice as a low-cost refreshment and nutrition source despite economic difficulties. Brands that manage to strike the right balance between price competitiveness and sufficient retail coverage remain relevant in the category in the economically constrained consumer environment in Guatemala, where a high level of poverty and low levels of discretionary spending power persist.

Guatemala Juice Market ChallengeSugar Concerns Weaken Juice’s Health Image

Juice is facing demand headwinds because most consumers have come to view it as a high sugar drink instead of a simple fruit drink. Adults are also starting to think of juice as a morning treat and switching to dietary supplements to support their immune system, which undermines habitual consumption habits and makes mainstream brands less able to protect health-based positioning. This cognitive transformation of nutritional staple to sugar-containing drink poses inherent category issues that demand strategic repositioning and reformulation reactions.

This attitude is supported by the larger disease burden associated with the overconsumption of sugar. Estimates from the International Diabetes Federation indicate that in 2024, there are 1,103,701 adults aged 20 to 79 years living with diabetes in Guatemala, which is equivalent to 13.2% prevalence, increasing attention on sweet beverages, including juice. The prevalence of diabetes creates awareness of health issues that exert pressure on sugar-containing drinks irrespective of differences between natural and added sugar. The overlap of evolving health attitudes and a significant burden of diabetes puts long-term strain on traditional positioning of juices, requiring reformulation to lower-sugar versions and functional benefit messaging that goes beyond conventional fruit nutrition messaging.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Guatemala Juice Market TrendPlant Waters Gain Daily Share

Coconut water and other plant-based waters become visible as consumers demand clearer wellness indicators than those offered by traditional juice claims. Better traction of coconut and plant waters, and wider distribution of aloe vera juices in convenience stores and small local grocers, show that wellness positioning is shifting to mainstream, quick-purchase outlets. The trend reflects a core shift from specialty health products to daily beverage choices available at traditional retail touchpoints.

Shopping habits in urban areas favor this grab-and-go trend and single-serve pack formats. According to World Bank statistics, in 2024, 55.95% of the Guatemala population resided in urban centers, boosting demand for immediate consumption from local shops and promoting portable formats beyond conventional breakfast occasions. Urbanization accelerates convenience-based buying patterns and functional beverage use. The plant-based hydration trend opens possibilities for brands to create naturally positioned, functionally credible alternatives to traditional juice, attracting health-conscious consumers with convenient formats and transparent wellness positioning aligned with changing urban consumption trends.

Guatemala Juice Market OpportunityHeat Boosts Hydration-Led Occasions

The increased frequency of heat stress increases the significance of quick hydration, providing juice with an opportunity to compete based on refreshment advantages rather than breakfast tradition alone. Rising demand for isotonic beverages during heat waves also highlights clear gaps for light coconut waters or juices with plant extracts focused on hydration on the move. Climate conditions create broader hydration-oriented consumption events outside traditional meal-based beverage settings.

These use cases are supported by climate conditions. According to a May 2024 bulletin by INSIVUMEH, temperatures in some areas of Guatemala reached 37°C to 42°C, reinforcing the need for portable hydration when commuting, taking children to school, or working outdoors. Excessive heat exposure creates urgent hydration needs that juice can meet through appropriate formulation and format positioning. A heat-based opportunity allows brands to reposition juice from a breakfast staple to a functional hydration solution, seizing new consumption occasions through climate-appropriate product development focused on rapid rehydration, electrolyte content, and portability in Guatemala’s increasingly heat-stressed environment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Guatemala Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment with the largest share in the category division is Nectars, which has a market share of 45%. Nectars are favored because of their combination of familiar local flavours such as mango, peach, and guava with competitive pricing. This segment is especially strong among low-end consumers purchasing convenient single-serve cans and cartons for daily consumption, making nectars the volume anchor that facilitates broad category access.

Although nectars hold a 45% share, they are under pressure to evolve with health trends. Manufacturers are enriching products with vitamins A, C, and D to maintain parental appeal and exploring sugar-free versions to address wellness concerns. Jumex and other brands continue to dominate this segment with deep flavour portfolios and strong presence in neighborhood stores, making nectars the main volume driver through 2032. The combination of format accessibility, flavour diversity, and competitive pricing makes nectars the cornerstone category base supporting mass-market penetration across Guatemala’s diverse consumer base.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment with the largest portion in the sales channel division is Off-Trade, which holds 90% of total market sales. This dominance is driven by the cultural importance of small local grocers, where people frequently purchase juice for immediate consumption. These neighborhood tiendas form the backbone of the Guatemalan retail environment, providing access to both single-serve and large-format family juices across communities and ensuring broad geographic coverage that supports universal category access.

Although traditional grocers account for most of this 90% share, convenience stores are the fastest-growing sub-channel within off-trade. Convenience chains attract younger shoppers focused on speed and efficiency through standardized management and regular promotional multipacks. The coexistence of traditional access and modern convenience ensures off-trade channels remain the primary entry point for juice brands in Guatemala, supporting varied purchase occasions through complementary retail formats aligned with diverse consumer preferences and shopping behaviors.

List of Companies Covered in Guatemala Juice Market

The companies listed below are highly influential in the Guatemala juice market, with a significant market share and a strong impact on industry developments.

- Industria Procesadora de Lácteos (Inprolacsa)

- Jumex Guatemala SA

- Alimentos Ideal SA

- Alimentos Maravilla SA

- Industrias Alimenticias Kern's y Cia SCA

- Livsmart Brands SA

- Ajemaya SA

- Coca-Cola de Guatemala SA

- OKF Corp

- Distribuidora Sula SA

Competitive Landscape

Guatemala juice market is led by Alimentos Maravilla, whose broad portfolio (Del Frutal, De la Granja, Tampico, Del Monte) and extensive distribution across small local grocers underpin leadership, with child-focused fortified variants and multi-format offerings reinforcing scale advantages. Coca-Cola de Guatemala leverages Del Valle and Del Valle Fresh through its powerful carbonates network, returnable 500ml bottles and cross-promotions, strengthening reach and affordability. Jumex acts as a dynamic challenger in nectars, competing on flavour familiarity and convenient single-serve packs for budget-conscious consumers. Indirect competition from isotonic drinks, RTD teas and plant waters—particularly coconut water—intensifies health-led substitution. Key differentiation opportunities lie in credible low-sugar reformulation, functional claims (hydration, gut health), exotic flavours, and multipack innovation tailored to on-the-go and family consumption occasions.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Guatemala Juice Market Policies, Regulations, and Standards

- Guatemala Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Guatemala Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Guatemala 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Guatemala Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Guatemala Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Guatemala Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Guatemala Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Alimentos Maravilla SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Industrias Alimenticias Kern's y Cia SCA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Livsmart Brands SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ajemaya SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coca-Cola de Guatemala SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Industria Procesadora de Lácteos (Inprolacsa)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Jumex Guatemala SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alimentos Ideal SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- OKF Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Distribuidora Sula SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alimentos Maravilla SA

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.