Mexico Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

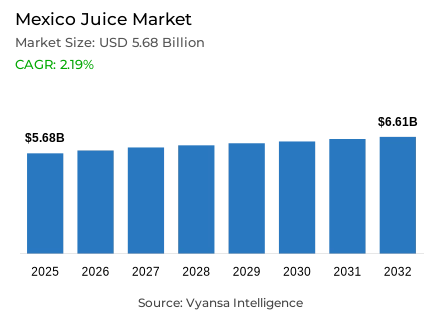

Mexico Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in Mexico was estimated at USD 5.68 billion in 2025.

- The market size is expected to grow to USD 6.61 billion by 2032.

- Market to register a CAGR of around 2.19% during 2026-32.

- Category Shares

- Juice drinks (up to 24% juice) grabbed market share of 55%.

- Competition

- More than 10 companies are actively engaged in producing juice in Mexico.

- Top 5 companies acquired around 70% of the market share.

- Grupo Lala SAB de CV, Unifoods SA de CV, Campbell de México SA de CV, Jugos del Valle SA de CV, Jumex SA de CV Grupo etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 90% of the market.

Mexico Juice Market Outlook

The Mexican juice market is at a crossroads where the end user behaviour is radically redefined by the public-health regulations. It is estimated that the market will be USD 5.68 billion in 2025 and is projected to be USD 6.61 billion in 2032, with a CAGR of about 2.19% in the forecast period. Despite the positive growth of value, volume sales are facing strong headwinds because of a law prohibiting the sale of sugary products with black-seals in schools and to almost double the sugar tax (IEPS) to 3.08 pesos per litre effective 1 January 2026.

The dynamics of products are moving towards health and transparency. Juice drinks (up to 24% juice) already occupy 55% of the market share because of their relative affordability, but are losing popularity as parents and health-conscious end users abandon high-fructose corn syrup and artificial dyes. Conversely, 100% juice has been more resilient, and it is in line with the natural trend, but it has supply issues and price surges due to a global shortage of oranges.

The main survival strategy of such giants as Jugos del Valle and Grupo Jumex has become innovation. Manufacturers are shifting to functional juices with ingredients like cactus leaf, ginger and berries to provide certain benefits like digestive health or hydration. The emergence of Cero (zero-sugar) and low-calorie brands is a direct reaction to the aggressive anti-obesity campaigns of the government and the next stage of labeling that will be introduced in 2028 and will further reduce sugar and sodium levels.

Home consumption continues to dominate sales channels with off-trade channels taking 90% of the market. Although small local grocers are the leaders, they have to compete with fast-growing discounters like Tiendas 3B and Aurrera that are fueling the development of own-label products. Supermarkets respond to this by loyalty programmes and omnichannel e-commerce investments, and forecourt retailers are the only channel that is not going down because of the steady demand of single-serve, on-the-go products.

Mexico Juice Market Growth Driver

Escalating Chronic Disease Burden Accelerating Demand for Lower-Sugar and Naturally Positioned Juices

The focus on obesity and diabetes by the Mexican government continues to put sugar consumption in the spotlight of the population, and end users are increasingly preferring beverages that are seen as more natural and less sugar-dense. Diabetes mellitus is one of the major causes of death according to INEGI, 211,894 deaths were registered between January and March 2025 and the crude death rate stood at 162.5 per 100,000 inhabitants in the same period, thus keeping health risks at the center of the daily household agenda. The leading cause of death is cardiovascular diseases, and 51,382 deaths in the first quarter of 2025 will support the need to promote healthier lifestyles at home and in schools.

This health climate drives the demand of 100% juice, smaller portion sizes, and reduced-sugar lines that offer refreshment and help families reduce the amount of sugar consumed daily. The public-health awareness is producing a structural change in the demand to naturally positioned, lower-sugar juice substitutes. The high chronic-disease burden and the ongoing public-health messaging create favourable circumstances in which products that are positioned as healthier options can be promoted, which helps the category to shift towards higher-end, naturally sweetened formulations that are consistent with preventive-health behaviours that are becoming increasingly ingrained in Mexican end user consciousness and buying behaviour.

Mexico Juice Market Challenge

Mandatory School Nutrition Restrictions Curtailing High-Sugar Juice Consumption Occasions

Stricter school-nutrition policies decrease one of the major occasions of juice and nectar intake, which are commonly viewed as high-sugar items. According to the Mexican education authority, 258,689 schools will be required to follow these provisions as of 29 March 2025, which will increase the control over the purchases made by children and restrict the impulse buying in the canteens and the kiosks located nearby. This regulatory implementation eradicates a large amount of traditional high-sugar juice formats that were once available in school channels.

A 2023–2024 school-cycle official monitoring of 10,533 schools found that 98% sold junk food and 95% sold sugary beverages, and 25% had junk-food advertising in schools. This increases the pressure on packaged juice formats with warning seals, hastens the reformulation process, and reduces the daily exposure of children and teenagers who make regular purchases. School restrictions thus provide structural impediments to volume expansion of traditional sweetened juice categories and encourages the creation of reformulated, compliant products that comply with nutritional guidelines and regulatory standards.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Mexico Juice Market Trend

Expanded Sugar and Sweetener Taxation Forcing Accelerated Reformulation and Clean-Label Repositioning

Fiscal measures to curb sugar consumption have been tightened significantly forcing beverage producers to re-evaluate compositions, such as juice drinks and nectars, which include added sugar or sweeteners. According to the Mexican Chamber of Deputies, the approved adjustment of the IEPS will alter the particular quota of flavored beverages to 1.6451 pesos per litre in 2025 to 3.0818 pesos per litre in 2026, which will exert pressure on the cost of sweetened recipes and retail prices. This almost doubling of the sugar tax generates instant economic reformulation incentives.

The tax base includes beverages with any form of sweetener, not just added sugar, which hastens the transition to no added sugar, cleaner labels, and more accurate wellness positioning. Functional ingredients that do not make the product heavy sweet are being investigated by brands. This financial trend is leading to a fundamental category shift with manufacturers striking a balance between palatability, cost competitiveness and regulatory compliance. The overall taxation of sweeteners puts a long-term strain on innovation in natural sweetening options, flavour-enhancement technologies, and the incorporation of functional ingredients, which essentially redefines the juice-formulation environment and competitive-positioning approaches in Mexico.

Mexico Juice Market Opportunity

High Internet Penetration Enabling Digital Scale for Functional and Premium Juice Innovation

Retail online provides new avenues to differentiated juices, particularly functional and reduced-sugar lines, which need more explanation than shelf labels can offer. In 2024, 83.1% of individuals aged six and above were internet users, which translates to 100.2 million users, and this presents a significant market to online search of wellness-oriented beverages. This wide internet penetration creates a favourable infrastructure to the growth of digital commerce and end user education via the internet.

Grocer-beverage sales are already supported by online buying behaviour. According to the data provided by INEGI, 35.8% of internet users have made online purchases, and the most frequent online purchases are foods and beverages (33.0). This channel is also appropriate to single-serve packs and high-quality 100% juices with clear origin information, allowing the brands to inform end users about the ingredients like ginger, berries, or cactus leaf. E-commerce enables comprehensive nutritional communication, ingredient disclosure, and functional benefit clarification, which aids in premium positioning and trial generation of innovative formulations that overcome the traditional retail communication barriers.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Mexico Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the Mexico juice market, where Juice Drinks (up to 24% Juice) grabbed a market share of 55%. This segment’s lead is primarily maintained through its competitive pricing and wide availability across various pack sizes, appealing to large families and budget-sensitive end users. However, its dominance is being tested by new 2025 regulations that prohibit these high-sugar items from being sold in public schools, prompting a noticeable shift in purchase patterns among parents.

As the government introduces stricter taxes on artificial sweeteners and sugar, the juice drinks segment is undergoing rapid reformulation. Manufacturers are introducing lower-calorie versions, such as "Jumex Bida" and "Blist," to capture the younger demographic while avoiding the most severe tax penalties. While 100% juice is growing in popularity among affluent urbanites, the sheer reach of juice drinks in traditional and discount retail channels ensures it remains the market's largest category through the 2032 forecast period.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 90% of the market. This channel's strength reflects the high frequency of household juice consumption in Mexico, supported by an extensive network of small local grocers and wholesalers. However, the retail landscape is changing as aggressive discounters like Aurrera penetrate smaller cities, offering low-cost private-label alternatives that challenge established brands. These stores are increasingly becoming the destination for bulk juice purchases as end users look to maximize their spending power.

Within the off-trade sector, supermarkets are maintaining their relevance by investing in digital transformation and loyalty-driven discounts. At the same time, convenience stores and forecourt retailers are seeing steady performance as the only channels to avoid volume declines in 2025, thanks to the demand for single-serve "on-the-go" formats. As e-commerce continues to integrate with traditional retail, the off-trade channel is expected to remain the primary driver of the US$ 6.61 billion market by 2032.

List of Companies Covered in Mexico Juice Market

The companies listed below are highly influential in the Mexico juice market, with a significant market share and a strong impact on industry developments.

- Grupo Lala SAB de CV

- Unifoods SA de CV

- Campbell de México SA de CV

- Jugos del Valle SA de CV

- Jumex SA de CV Grupo

- Sociedad Cooperativa Trabajadores de Pascual SCL

- Ajemex SA de CV

- Coca-Cola Mexico

- Derivados de Frutas SA de CV

- Herdez SAB de CV Grupo

Competitive Landscape

Mexico’s juice market in 2025 is led by Jugos del Valle, backed by Coca Cola’s portfolio breadth across 100% juice, nectars, and juice drinks, leveraging flavour diversification, wide pack formats, and strong distribution to defend share amid regulatory pressure. Grupo Jumex is a key challenger, gaining relative momentum through innovation such as Blist for younger consumers and Jumex Cero and Bida, which emphasise low calorie and no added sugar positioning in response to tightening school sales bans and black seal regulations. Private label is intensifying competition as discounters expand nationally. Indirect competition from bottled water, functional beverages, and other low sugar soft drinks is rising. Differentiation opportunities lie in functional claims, clean label reformulation, origin transparency, and targeted reduced sugar innovation compliant with evolving regulation.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Mexico Juice Market Policies, Regulations, and Standards

4. Mexico Juice Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Mexico Juice Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.1.2.By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1.By Category

5.2.1.1. 100% Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Reconstituted- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Nectars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.3. Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Nature

5.2.2.1. Conventional- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Organic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Packaging Material

5.2.3.1. Plastic- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Glass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Metal- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Packaging Type

5.2.4.1. PET Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Metal Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Sales Channel

5.2.5.1. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.1. Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.2. Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.3. Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

5.2.5.1.4. Online Platforms- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Mexico 100% Juice Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.1.2.By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Mexico Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.1.2.By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Mexico Nectars Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.1.2.By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Mexico Vegetable Juice Market Statistics, 2022-2032

9.1. Market Size & Growth Outlook

9.1.1.By Revenues in USD Million

9.1.2.By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1.By Nature- Market Insights and Forecast 2022-2032, USD Million

9.2.2.By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

9.2.3.By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Mexico Fruit and Vegetable Blends Market Statistics, 2022-2032

10.1. Market Size & Growth Outlook

10.1.1. By Revenues in USD Million

10.1.2. By Quantity Sold in Million Litres

10.2. Market Segmentation & Growth Outlook

10.2.1. By Nature- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1. Company Profiles

11.1.1. Jugos del Valle SA de CV

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Jumex SA de CV, Grupo

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Sociedad Cooperativa Trabajadores de Pascual SCL

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Ajemex SA de CV

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Coca-Cola Mexico

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Grupo Lala SAB de CV

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Unifoods SA de CV

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Campbell de México SA de CV

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Derivados de Frutas SA de CV

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. Herdez SAB de CV, Grupo

11.1.10.1.Business Description

11.1.10.2.Product Portfolio

11.1.10.3.Collaborations & Alliances

11.1.10.4.Recent Developments

11.1.10.5.Financial Details

11.1.10.6.Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.