Poland Plant-Based Dairy Market Report: Trends, Growth and Forecast (2026-2032)

Product Type (Plant-Based Milk (Soy Drinks, Almond, Blends, Coconut, Oat, Rice, Other Plant-Based Milk), Plant-Based Yoghurt, Plant-Based Cheese), Sales Channel (Offline (Grocery Retailers, Convenience Retailers, Supermarkets, Hypermarkets), Online) ... Read more

|

Major Players

|

Poland Plant-Based Dairy Market Statistics and Insights, 2026

- Market Size Statistics

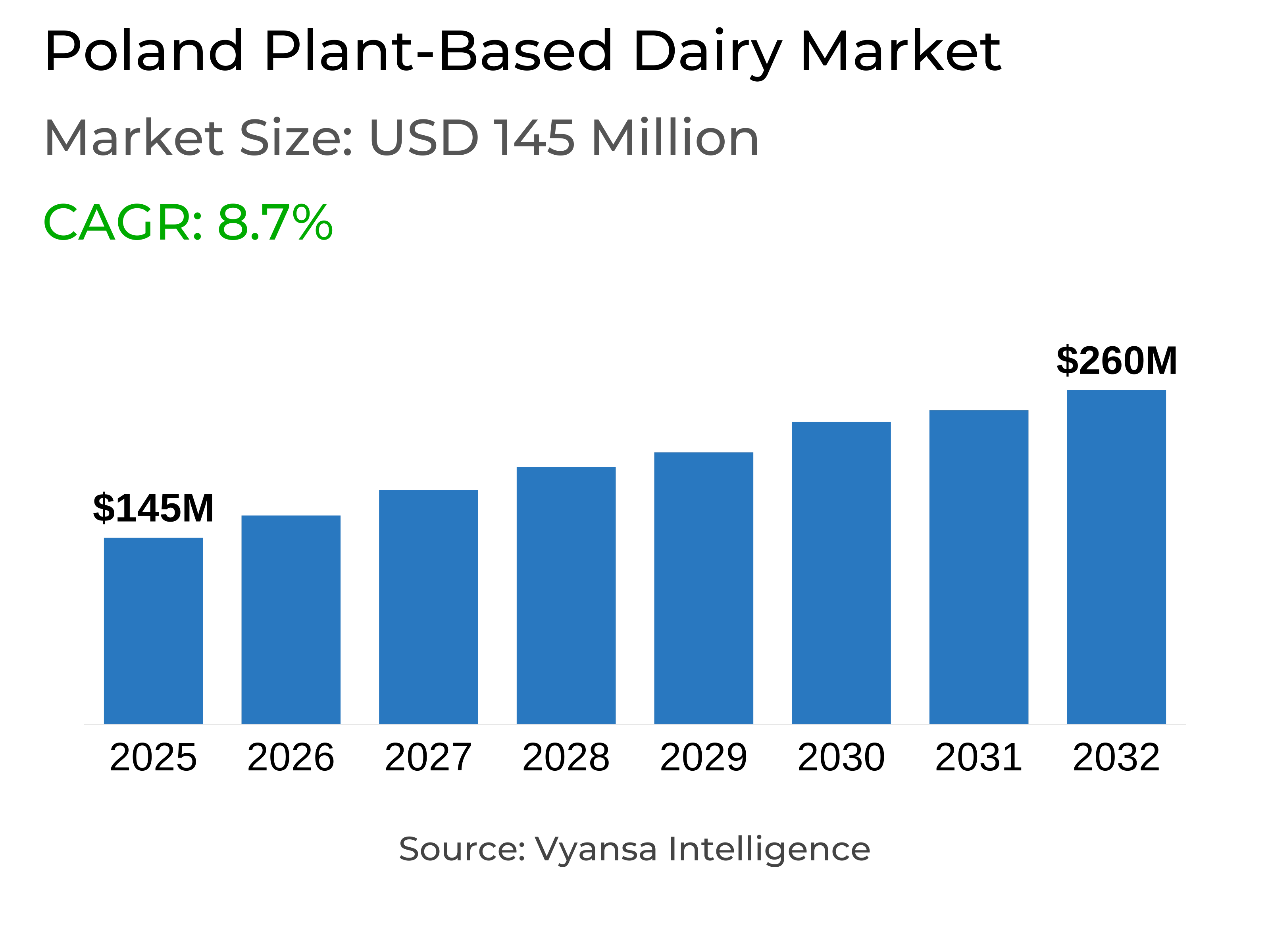

- Plant-based dairy in poland is estimated at USD 145 million.

- The market size is expected to grow to USD 260 million by 2032.

- Market to register a cagr of around 8.7% during 2026-32.

- Product Type Shares

- Plant-based milk grabbed market share of 80%.

- Competition

- More than 10 companies are actively engaged in producing plant-based dairy in poland.

- Top 5 companies acquired around 80% of the market share.

- Nutriops-Laboratorios Almond SL, Hain Europe NV, Ekomera UAB, SANTE Sp zoo, Rossmann SDP Sp zoo etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 90% of the market.

Poland Plant-Based Dairy Market Outlook

The Poland plant-based dairy market was worth $145 million in 2025 and would be reaching $260 million by 2032, with a CAGR of around 8.7%. Plant-based milk is dominating the market with a share of around 80%, supported by strong end users demand for healthy and sustainable diets. Younger generations, particularly Gen Z, are leading demand increasingly, choosing plant-based substitutes for their environmental and moral benefits. End users concerned about health are also driving growth, choosing foods with added calcium, vitamin B12, and vitamin D to meet the nutritional quality of conventional dairy.

Retail offline channels are to continue dominating the market, with 90% of turnover. Discounters offer a stable end users base to enjoy good prices and an extensive range of plant-based products, while supermarkets and hypermarkets are key retailers for premium brands such as Alpro and Violife. Retail online is to keep expanding dynamically, as convenient end users who desire ease of price comparison, home delivery of an extensive assortment of plant-based products, and quick availability are drawn to it.

Product extension will be the growth driver for the market. National brands and private labels will both extend their ranges throughout milk, yoghurt, and cheese alternatives to cater for different tastes, dietary needs, and price levels. Improved taste, a softer texture, and advancing technology are making plant-based yoghurts and cheese increasingly appealing to a growing end users market.

Overall, Poland plant-based dairy market will be experiencing robust growth over the forecast period. Increased health awareness, environmental and ethical awareness, and expanding product availability will drive adoption, making the market capable of winning over a wide base of end users and acquiring further momentum through retail channels.

Poland Plant-Based Dairy Market Growth Driver

Rising Awareness of Health and Sustainability

Rising awareness of sustainability and health among end users is significantly boosting the growth of Poland plant-based dairy segment. End users are becoming more conscious of seeking products that are lactose-free, vitamin-fortified, and ethically produced, offering improved animal welfare and reduced environmental impact. This focus inspires more families to embrace plant-based dairy in regular diets, triggering volume and value expansion in the market.

The combination of nutritional wholesomeness and eco-friendliness also motivates the manufacturers to extend their product ranges. Alpro and Violife brands provide a diverse range of plant-based milks, yogurts, and cheeses at different price points, and thus the products reach a large segment. Healthy and green-conscious end users who are looking to promote plant-based foods will generate robust demand and propel continued growth in the marketplace.

Poland Plant-Based Dairy Market Trend

Gen Z Ethical end usersism

A significant trend among Poland plant-based dairy market is Gen Z ethical consciousness. Diet, as far as this generation is concerned, is an ethical choice, choosing plant-based options to inflict less harm on animals and to stand by their ideals of veganism and social justice.

Gen Z also requires transparency and responsibility from brands regarding production methods and animal welfare. Brands that engage in ethical procurement and cruelty-free labeling excel with this generation. Such a trend is influencing consumption patterns, making plant-based milk a values-driven choice rather than a simple dietary preference, and ensuring long-term engagement and loyalty among young end users.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Poland Plant-Based Dairy Market Opportunity

Product Innovation and Nutritional Enhancement

Year-round innovation offers massive growth opportunities for Poland plant-based dairy market. Companies will enrich their products with calcium, vitamin B12, and vitamin D in order to make them taste, texture, and nutritionally richer compared to dairy, offering them alternatives to dairy.

Greater taste, form, and category innovation will power trial and acquisition among health- and sustainability-conscious end users. Start-ups and larger brands alike will be able to launch new products that meet ethical, ecological, and functional requirements, further driving market penetration and long-term growth in the plant-based dairy sector.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Poland Plant-Based Dairy Market Segmentation Analysis

By Product Type

- Plant-Based Milk

- Plant-Based Yoghurt

- Plant-Based Cheese

The segment with highest market share under Product Type in Poland plant-based dairy market is plant-based milk, which accounts for about 80% of the market. Plant-based milk is in the lead due to its versatility, ease of use, and wide acceptance by end users seeking healthier and ethically superior alternatives. Oat, almond, and rice milks are top sellers and are accompanied by branded and store brands at different price levels.

Greater accessibility in larger stores, discounters, and convenience stores has cemented this segment dominance. End users increasingly incorporate plant-based milk into their daily routines, mixing it with cereals, coffee, and smoothies. Continuous product development, such as fortified and flavored ones, has enhanced appeal, turning plant-based milk into the first-choice beverage for Poland end users that prioritize health and the environment.

By Sales Channel

- Offline

- Online

The segment with highest market share under Sales Channel is retail offline, which has a share of approximately 90%. Supermarkets and discounters are leading the distribution, providing extensive product assortment and low prices appealing to a wide end users base. Discounters are particularly strong, offering affordable plant-based products that believe in price-sensitive end users.

Retail Online is emerging as the most lively channel, offering convenience, home delivery, and easy price comparison. While Retail offline channels prevail, Retail online destinations become increasingly vital as outlets for end users seeking niche or specialty plant-based products. The confluence of existing offline infrastructures and increasing retail online enables widespread access and fuels overall market expansion.

Top Companies in Poland Plant-Based Dairy Market

The top companies operating in the market include Nutriops-Laboratorios Almond SL, Hain Europe NV, Ekomera UAB, SANTE Sp zoo, Rossmann SDP Sp zoo, Jeronimo Martins Polska SA, Upfield Holdings BV, Natumi AG, Sante A Kowalski Sp j, Tesco Polska Sp zoo, etc., are the top players operating in the poland plant-based dairy market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Poland Plant Based Dairy Market Policies, Regulations, and Standards

4. Poland Plant Based Dairy Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Poland Plant Based Dairy Market Statistics, 2020-2030F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Plant-Based Milk- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.1. Soy Drinks- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.2. Almond- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.3. Blends- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.4. Coconut- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.5. Oat- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.6. Rice- Market Insights and Forecast 2020-2030, USD Million

5.2.1.1.7. Other Plant-Based Milk- Market Insights and Forecast 2020-2030, USD Million

5.2.1.2. Plant-Based Yoghurt- Market Insights and Forecast 2020-2030, USD Million

5.2.1.3. Plant-Based Cheese- Market Insights and Forecast 2020-2030, USD Million

5.2.2.By Sales Channel

5.2.2.1. Offline- Market Insights and Forecast 2020-2030, USD Million

5.2.2.1.1. Grocery Retailers- Market Insights and Forecast 2020-2030, USD Million

5.2.2.1.2. Convenience Retailers- Market Insights and Forecast 2020-2030, USD Million

5.2.2.1.3. Supermarkets- Market Insights and Forecast 2020-2030, USD Million

5.2.2.1.4. Hypermarkets- Market Insights and Forecast 2020-2030, USD Million

5.2.2.2. Online- Market Insights and Forecast 2020-2030, USD Million

5.2.3.By Competitors

5.2.3.1. Competition Characteristics

5.2.3.2. Market Share & Analysis

6. Poland Plant-Based Milk Market Outlook, 2020-2030F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

7. Poland Plant-Based Yoghurt Market Outlook, 2020-2030F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

8. Poland Plant-Based Cheese Market Outlook, 2020-2030F

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in US$ Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Sales Channel- Market Insights and Forecast 2020-2030, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.SANTE Sp zoo

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Rossmann SDP Sp zoo

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Jeronimo Martins Polska SA

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Upfield Holdings BV

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Natumi AG

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.Nutriops-Laboratorios Almond SL

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Hain Europe NV

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.Ekomera UAB

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Sante A Kowalski Sp j

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Tesco Polska Sp zoo

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.