Peru Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

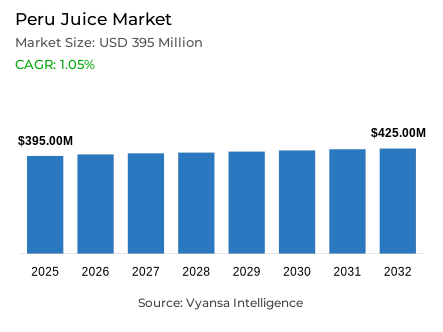

Peru Juice Market Statistics and Insights, 2026

- Market Size Statistics

- Juice market size in Peru was estimated at USD 395 million in 2025.

- The market size is expected to grow to USD 425 million by 2032.

- Market to register a CAGR of around 1.05% during 2026-32.

- Category Shares

- Nectars grabbed market share of 51%.

- Competition

- More than 10 companies are actively engaged in producing juice in Peru.

- Top 5 companies acquired around 70% of the market share.

- Zand SAC, Industrias San Miguel, Processed Food SAC, Ajeper SA, Arca Continental Lindley SA etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 85% of the market.

Peru Juice Market Outlook

The Peru juice market is going through a complicated stage of structural transformation as the end user preferences are changing towards lighter and more refreshing products. The market is estimated to be USD 395 million in 2025 and USD 425 million in 2032 with a CAGR of about 1.05% in the period 2026-32. Although value performance is maintained through price changes and an increasing interest in natural options, the category is generally experiencing overall volume pressure due to cheaper and lower-sugar drinks like flavored waters and sports drinks.

There is a significant internal repositioning as high-sugar nectars become irrelevant to healthier offers. The market share of nectars is currently at 51%, but the segment is shrinking because of the increased cost of production and health issues. Conversely, reconstituted 100% juices are also becoming very popular, with major players like the AJE Group investing in them. These natural versions are made more available to the mass end user, and the gap between the high-end health benefits and the affordability is narrowed.

Innovation is also not limited to Lima, as functional shots, cold-pressed juices, and detox blends are making their way into secondary cities. Such premiumisation is fuelled by brands like Zuma that attract end user who want fresh and minimally processed drinks. Moreover, the tougher government controls on honest labelling and image of fruits are compelling manufacturers to remodel their packaging. This shift to transparency will prefer brands that focus on authentic quality signals, including fruit origin and clean-label formulations.

sales channel is still deeply entrenched in retail, with 85% of the market being controlled by Off-Trade channels. Small local grocers remain the leaders because of their proximity and accessibility in lower-income neighborhoods, especially in single-serve formats. Nevertheless, the most vibrant growth drivers are convenience stores like Tambo and Oxxo, which serve urban end user who are interested in grab-and-go convenience. With the market shifting to 2032, the ability to succeed will be based on the capability of the brands to change their portfolios to reflect these new lifestyle and wellness trends.

Peru Juice Market Growth DriverRising Obesity Concerns Elevating Demand for Natural and Authentic Juice Positioning

The everyday beverage decisions of Peruvian end user are becoming more health- and weight-conscious, which increases the desire to focus on more natural and simple juice propositions. According to the Ministry of Health of Peru, based on the Demographic and Family Health Survey 2024, 62% of Peruvians aged 15 and older are overweight, with 25.7% obese. This high health burden maintains social consciousness of diet-related health risks and shapes beverage buying behavior towards perceived healthier options.

This health pressure forms the basis of the demand of juices placed around authenticity and transparent nutritional indicators, making 100% juice variants more applicable in well-being moments and meal accompaniment. In response, brands are focusing on products that communicate less processing and fewer dubious claims, with end user becoming increasingly choosy and appreciating quality over price-based purchases. The shift in demand towards wellness presents an opportunity to premium, naturally positioned juice formulations, which focus on the transparency of fruit content, minimal processing, and clean ingredient lists, which are consistent with preventive health behaviours that are becoming more ingrained in Peruvian end user behaviour and household purchasing habits.

Peru Juice Market ChallengeFood Price Inflation Undermining Nectar Competitiveness

The increasing prices and price pressure makes it harder to keep the competitive pricing of sweeter and more processed forms of juice, and thus makes companies less significant in the daily household baskets. According to the National Institute of Statistics and Informatics (INEI), the national end user price index rose by 0.30% month-on-month and 1.10% in January-April. This long-term inflationary condition limits the flexibility of prices of manufacturers and restricts the ability to invest in promotion.

In the same release, INEI reports that the food and non-alcoholic beverages division increased 0.94% in Lima Metropolitana in April 2025, which puts strain on the input costs of fruits and the shelf prices. This climate constrains the ability to make aggressive promotions, especially of nectars that have both affordability and poorer health images than lighter, hydrating products. The structural disadvantages of cost escalation force the traditional nectar formats to re-formulate to lower-cost ingredients or downsize the packs, and at the same time, face end user drift to the high-end 100% juice and natural positioning that attracts higher prices due to wellness associations.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Peru Juice Market TrendHeightened Advertising Enforcement Driving Transparent Label and Claim Practices

Marketing and labeling are under increased scrutiny, forcing juice brands to be more careful with naturalness claims, imagery, and implied benefits. According to Indecopi, it has already launched 13 sanctioning processes associated with hidden advertising and misleading practices since the beginning of its monitoring activities, with enforcement cases involving significant financial fines. This regulatory alertness subjects marketing communication tactics and packaging claims substantiation to immediate compliance demands.

Indecopi, in the same communication, quotes an example where a fine of 47 UIT, which is equivalent to S/ 251,450 was paid, thus showing the actual compliance cost of ambiguous commercial communication. In the case of juice portfolios, this regulatory environment hastens the transition to open fruit-based communications, more explicit nutrition indicators, and reduced suggestive imagery that can be questioned under the truth-in-advertising provisions. Tougher enforcement imposes strategic burdens on substantiation of claims, redesign of packaging, and review of marketing communications, and at the same time, it provides competitive advantages to brands that exhibit genuine transparency and evidence-based positioning in accordance with regulatory expectations and end user trust conditions.

Peru Juice Market OpportunityExpanding Modern and Convenience Retail Creating New On-the-Go Juice Occasions

The fast emergence of convenience-based retail establishes strong channels to establish new juice occasions based on mobility, impulse, and smaller portions. According to INEI, commercial activity rose by 3.90% in March 2025, indicating a favourable climate in the retail formats that focus on speed and proximity. This retail growth creates new sales touchpoints and consumption occasions outside of the traditional large-pack household purchases, thus facilitating format innovation and occasion-based positioning strategies.

With the growth of convenience stores and contemporary retail presence, brands gain additional high-frequency touchpoints to market ready-to-drink juices, cold-pressed products, and functional shots in accordance with urban lifestyles. This channel momentum helps portfolio experimentation beyond the conventional large-pack purchases and helps premium propositions to achieve visibility via grab-and-go placement and tight assortments to reach young, time-starved end user. The contemporary retail growth enables the brands to seize the impulse moments, experiment with new formats, and create the high-end positioning with the help of convenience-based channels that facilitate the increased per-unit pricing and faster trial creation in the context of the changing urban retail environment in Peru.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Peru Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the Peru juice market, where Nectars grabbed a market share of 51%. Despite its lead, this segment faces a steep decline as end user move toward healthier and more affordable alternatives. High sugar content and increasing prices for raw materials have made nectars less attractive for daily household consumption, leading many shoppers to trade down to juice drinks or shift toward 100% juice variants for perceived health benefits.

To stabilize demand, the category is seeing a rise in reconstituted 100% juices, which offer a more premium positioning at a relatively accessible price point. AJE Group has been a key driver in scaling these natural options through its extensive sales network. As the forecast period progresses, the focus is expected to shift away from traditional nectars toward functional and clean-label beverages that better align with the modern Peruvian end user’s preference for well-being and authenticity.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 85% of the market. Traditional retail, specifically small local grocers, remains the cornerstone of the market due to its deep penetration in neighborhoods and the popularity of frequent, small-sized purchases. These stores are vital for the volume sales of affordable juice drinks and single-serve formats, serving as the primary touchpoint for a large demographic across both urban and rural regions of Peru.

While traditional grocers lead in volume, convenience stores are emerging as the most dynamic channel. Chains like Tambo and Oxxo are rapidly expanding, capturing impulse purchases from younger, time-conscious urban end user. This shift reflects a broader trend toward immediacy and mobility, where "grab-and-go" juice formats are becoming a key growth driver. By 2032, the off-trade channel is expected to remain dominant, increasingly supported by these modern convenience formats and a more diversified retail landscape.

List of Companies Covered in Peru Juice Market

The companies listed below are highly influential in the Peru juice market, with a significant market share and a strong impact on industry developments.

- Zand SAC

- Industrias San Miguel

- Processed Food SAC

- Ajeper SA

- Arca Continental Lindley SA

- Laive SA

- Gloria SA Grupo

- Food Pack SAC

- Terrafertil Peru SAC

- P&D Andina Alimentos SA

Competitive Landscape

Peru’s juice market in 2025 is led by AJE Group, which reinforces its dominance through affordability, extensive traditional channel penetration, and agile portfolio reallocation toward juice drinks and reconstituted 100% juice, offsetting nectar decline. Zand Sac is the most dynamic challenger, premiumising the category via Zuma cold pressed juices and functional shots that resonate with wellness driven consumers and modern retail shoppers. Nectars are structurally weakening due to sugar perceptions and reduced price competitiveness, while 100% variants gain relative visibility as natural alternatives. Indirect competition from bottled water, flavoured waters, and reduced sugar carbonates is intensifying. Key differentiation opportunities lie in clean label transparency, regulatory compliant communication, functional premium innovation beyond Lima, and expanded convenience channel presence aligned with on the go consumption.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Peru Juice Market Policies, Regulations, and Standards

- Peru Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Peru Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Peru 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Peru Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Peru Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Peru Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Peru Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Ajeper SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Arca Continental Lindley SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laive SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gloria SA, Grupo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Food Pack SAC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Zand SAC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Industrias San Miguel

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Processed Food SAC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Terrafertil Peru SAC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- P&D Andina Alimentos SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ajeper SA

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.