Norway Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

Norway Juice Market Statistics and Insights, 2026

- Market Size Statistics

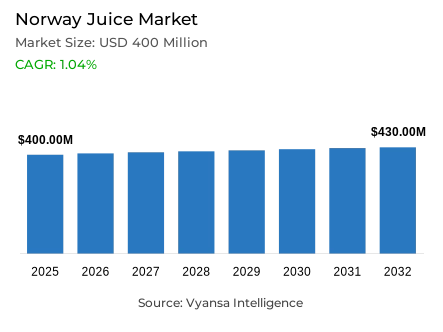

- Juice market size in Norway was estimated at USD 400 million in 2025.

- The market size is expected to grow to USD 430 million by 2032.

- Market to register a CAGR of around 1.04% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 85%.

- Competition

- More than 20 companies are actively engaged in producing juice in Norway.

- Top 5 companies acquired around 70% of the market share.

- Rema 1000 Norge AS, Froosh AS, Synnøve Finden AS, Sunniva Drikker AS, Bama Gruppen AS etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 75% of the market.

Norway Juice Market Outlook

The Norway juice market is going through a difficult phase characterized by high price fluctuations and changing end user behavior. The market is estimated to be USD 400 million in 2025 and will increase to USD 430 million in 2032 with a CAGR of about 1.04% between 2026 and 2032. Although the high prices of raw materials, especially oranges, have strained the volume sales, the market has been sustained by the high cultural demand of high-quality breakfast staples and natural products.

The future innovation is driven by health and convenience. Even though high prices are still an issue, the increasing health awareness is driving the demand of not-from-concentrate 100% juices and cold-pressed versions. The end user are also demanding functional advantages, like ginger that gives them energy or guava that gives them energy in a natural way, as a healthier substitute to the conventional energy drinks. The emergence of on-the-go smoothies and juice shots also indicates the demands of busy end user who want to have fast and healthy products.

The current market leader is Sunniva Drikker AS, which is still innovating with seasonal products like pressed apple juice of Hardanger. Nevertheless, the most dynamic growth is observed in the case of the private-label brands. Rema 1000 has become one of the players by providing competitive and value-oriented juices as well as high-end lines that replicate the feel of freshly squeezed fruit. To reduce the risks of supply caused by extreme weather and plant diseases, large suppliers like Bama are diversifying their sourcing of fruits in various countries.

The retail sector is highly concentrated in terms of sales with off-trade channels taking 75% of the market. The market is dominated by discounters such as Kiwi and Rema 1000 which control more than half of all sales due to their large store networks and low-price strategy. Although physical stores are still the most popular, e-commerce is the most rapidly expanding one. Social media like Oda is gaining popularity because people are finding it convenient to shop online and have a variety of products at a low price.

Norway Juice Market Growth DriverValue-Focused Grocery Retail Sustaining Routine Juice Purchases

Norway end user are highly value-oriented, and they prefer cheap juice and own-label products despite branded price increases. Statistics Norway reported that food and non-alcoholic beverage prices increased by 3.6% in January 2026 compared to January 2025, continuing to strain household budgets and forcing end user to switch to less expensive juice drinks and store brands. This continued price sensitivity supports value-based buying behavior and supports penetration of the private-label across the juice categories.

This value-seeking behaviour is directly connected with purchasing channels. The grocery-retail turnover grew by 7.1% between the fifth reporting period of 2024 and the same period of 2025, indicating a high dependence on everyday grocery formats. In these stores, household juice is bought in price ladders and regular promotions to make breakfast and lunch boxes. Retailers use own-labeled products to maintain shelf prices at competitive levels and maintain margins, thus sustaining a consistent, habitual buying behavior despite increasing input prices. The power of the value-retail channel provides a favourable environment to the positioning of low-price juice and the growth of the private-label products in the price-sensitive end user environment of Norway.

Norway Juice Market ChallengeElevated Food Inflation Pressuring Margins and Premium Volume

Increased cost of living limits the capacity of juice brands to absorb raw-material and packaging costs without losing volume. According to Statistics Norway, the end user price index increased by 3.2% in the twelve months between December 2024 and December 2025, with food and non-alcoholic beverages increasing at a higher rate of 5.2%. As the prices of everyday goods rise faster than wages, end user reduce discretionary expenditure and switch non-concentrate juices to less expensive blends or buy less often.

This inflationary background also increases competition in retailer prices, constraining the speed at which suppliers can restore margins following input shocks like fruit-price spikes. The resulting pressure strains the promotional budgets and significantly raises the risk of innovation. Manufacturers have to strike a balance between ensuring that the prices of their products remain affordable to the household and ensuring that the quality and freshness indicators that make the purchase of juice worthwhile over buying whole fruit or water substitutes. The gap between general and food inflation generates severe affordability constraints in the juice categories, limiting the premiumisation policies and limiting the pricing flexibility of manufacturers in the competitive retail market of Norway.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Norway Juice Market TrendStricter Recycling Mandates Embedding Sustainability as a Packaging Imperative

Sustainability is no longer a marketing boost but a viable packaging necessity. In the Waste Regulations, the Norway Environment Agency has placed increased recycling requirements. Starting in 2025, manufacturers will be required to have 47% of plastic packaging waste recycled, increasing to 30% and including 2024. The regulation increases to 52% by 2030, which will force beverage brands to thoroughly examine cartons, caps, labels, and secondary packaging systems to ensure compliance.

This trend is reflected in juice by lighter packs, better recyclability, and clearer messages on disposal at the shelf. The producers work in closer cooperation with producer-responsibility organisations and retailers to ensure compliant collection and reporting systems. Since price-sensitive end user are comparing prices between branded and own-label juice, sustainability improvements that do not increase shelf prices can preserve brand credibility and avoid making healthier juices seem wasteful. Sustainability demands by regulators provide operational necessities to packaging innovation and at the same time provide differentiation opportunities by environmental-responsibility positioning in line with Norway end user values and compliance requirements.

Norway Juice Market OpportunityGrowing Online Grocery Penetration Supporting Premium Juice Expansion

Retail online offers juice brands avenues to market more expensive not-from-concentrate and cold-pressed lines that do not fare well on price-led shelves. According to Statistics Norway, online trade turnover increased by 6.2%, between NOK 8,120,000,000 in the fifth reporting period of 2024 and NOK 8,625,000,000 in the fifth reporting period of 2025. This expansion is an indicator of rising shopper acceptance of home delivery and planned basket shopping, which provides favourable conditions to position premium products.

Since online baskets are not as limited by shelf-space, retailers can include broader assortments, multipacks, and seasonal editions, particularly when it comes to bulk purchases and frequent replenishment. This allows the brands to combine wellness cues like fresh taste and no-concentrate positioning with convenience, which attracts time-starved end user. Search and recommendation tools enable the targeting of price levels by the private-label and branded players to enhance conversion without the need to discount all the time. The expansion of e-commerce channels allows the premium juice positioning by providing better storytelling, more detailed nutritional data, and convenience-focused formats, which will contribute to the long-term category value development.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Norway Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the Norway juice market, where 100% Juice grabbed a market share of 85%. This overwhelming dominance is driven by a deep-seated end user preference for natural, high-quality products, particularly for traditional breakfast occasions. Despite significant price increases—with some orange juice prices doubling recently—shoppers continue to prioritize 100% juice variants over lower-content juice drinks because of their perceived health benefits and lack of artificial additives.

Innovation within this segment is moving toward premiumization and functional health. Brands are launching cold-pressed options and "not-from-concentrate" blends that include ingredients like ginger or carrot to appeal to wellness-focused end user. While budget-conscious shoppers are increasingly turning to high-quality private label versions from retailers like Rema 1000, the overall 100% juice category remains the cornerstone of the market, as authenticity and purity continue to outweigh pure price sensitivity for the majority of Norway households.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 75% of the market. This leadership is largely sustained by the powerful presence of discounters, which account for more than 50% of total sales. Retailers such as Kiwi and Rema 1000 have successfully captured the market by offering competitive pricing and frequent seasonal promotions, making juice a staple item in weekly grocery trips. Their extensive physical network ensures that juice remains highly accessible to end user across all regions of Norway.

While traditional retail leads in volume, the digital landscape is evolving rapidly. Retail e-commerce has emerged as the most dynamic sales channel, with leaders like Oda reporting significant revenue growth. Tech-savvy end user are increasingly drawn to the convenience and price transparency offered by online platforms. However, because price remains a top priority for Norway shoppers, the off-trade dominance is expected to persist through 2032, supported by the strong value propositions of both discount chains and expanding online grocery services.

List of Companies Covered in Norway Juice Market

The companies listed below are highly influential in the Norway juice market, with a significant market share and a strong impact on industry developments.

- Rema 1000 Norge AS

- Froosh AS

- Synnøve Finden AS

- Sunniva Drikker AS

- Bama Gruppen AS

- Norgesgruppen ASA

- Coop Norge Handel AS

- Orkla Foods Norge AS

- Coca-Cola European Partners Norge AS

- Multibev AS

Competitive Landscape

Norway’s juice market in 2025 is led by Sunniva Drikker AS, which maintains category leadership through a strong presence in 100% and reconstituted juices, seasonal local variants, and broad breakfast positioning, despite share pressure from rising orange costs. Bama remains influential in not from concentrate 100% juice, leveraging sourcing diversification to manage supply volatility. Rema 1000 Norge is the most dynamic competitor, expanding private label share with competitively priced core lines and premium not from concentrate offerings, benefiting from discounter dominance. Indirect competition from smoothies, juice shots, and energy alternatives is rising amid health and convenience trends. Key differentiation opportunities lie in functional fortification, local provenance, sustainable packaging, premium fresh positioning, and leveraging e-commerce growth while defending value leadership in discounters.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Norway Juice Market Policies, Regulations, and Standards

- Norway Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Norway Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Norway 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Norway Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Norway Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Norway Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Norway Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Sunniva Drikker AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bama Gruppen AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Norgesgruppen ASA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coop Norge Handel AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Orkla Foods Norge AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rema 1000 Norge AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Froosh AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Synnøve Finden AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coca-Cola European Partners Norge AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Multibev AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sunniva Drikker AS

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.