North America Synthetic Engine Oils Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Full Synthetic Engine Oils, Synthetic Blend Engine Oils, High-Mileage Synthetic Engine Oils, Racing and Performance Synthetic Engine Oils, Low-SAPS and Emission-Compatible Synthetic Engine Oils, Others), By Base Oil Type (Group III and Group III+ Synthetic Base Oils, Group IV PAO Synthetic Base Oils, Group V Ester Synthetic Base Oils, GTL-Derived Synthetic Base Oils, Blended Synthetic Base Oil Formulations, Others), By Viscosity Grade (0W-16 and Lower, 0W-20, 0W-30, 5W-20, 5W-30, 5W-40, 10W-30 and 10W-40, 15W-40 and Above, Others), By Engine Type (Gasoline Engines, Diesel Engines, Hybrid Vehicle Engines, CNG and LPG Engines, Heavy-Duty Diesel Engines, Others), By End-Use Vehicle and Equipment Type (Passenger Cars, Light Commercial Vehicles, Heavy-Duty Trucks, Buses and Coaches, Two-Wheelers and Motorcycles, Off-Highway and Construction Equipment, Agricultural Equipment, Marine Engines, Stationary Engines and Power Generation, Others), By Sales Channel (OEM and Factory Fill, Aftermarket), By Country (The US, Canada, Mexico, Rest of North America) ... Read more

|

Major Players

|

North America Synthetic Engine Oils Market Statistics and Insights, 2026

- Market Size Statistics

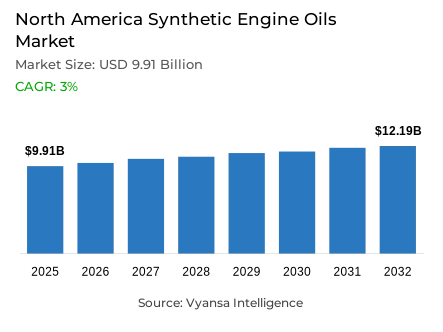

- Synthetic engine oils market size in North America was valued at USD 9.91 billion in 2025 and is estimated at USD 10.11 billion in 2026.

- The market size is expected to grow to USD 12.19 billion by 2032.

- Market to register a CAGR of around 3% during 2026-32.

- Product Type Shares

- Full synthetic engine oils grabbed market share of 55%.

- Competition

- Synthetic engine oils in North America is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 25% of the market share.

- Phillips 66 Company, Highline Warren LLC, AMSOIL INC., Exxon Mobil Corporation, Shell plc etc., are few of the top companies.

- End-Use Vehicle and Equipment Type

- Passenger Cars grabbed 55% of the market.

- Country

- The US leads with a 80% share of the North America market.

North America Synthetic Engine Oils Market Outlook

North America synthetic engine oils market covers full synthetic, synthetic blend, high-mileage, performance, and emission-compatible engine oils supplied for passenger cars, commercial vehicles, off-highway equipment, marine engines, and stationary power applications. Valued at USD 9.91 billion in 2025, USD 10.11 billion in 2026, and USD 12.19 billion by 2032, registering a CAGR of 3% during 2026-2032, synthetic engine oils market in North America supports engine protection, drain-interval optimization, fuel-economy compliance, and aftermarket positioning. North America synthetic engine oils industry remains tied to internal combustion, hybrid powertrains, and fleet service cycles.

Fuel-efficiency regulation and upgraded lubricant standards are tightening product specifications across the North America synthetic engine oils market. NHTSA finalized 2024 CAFE standards for passenger cars and light trucks for model years 2027-2031, with estimated fleet requirements reaching about 50.4 mpg by model year 2031. This increases demand for low-viscosity synthetic motor oils, advanced additive packages, and OEM-approved formulations that can reduce friction while protecting turbocharged, direct-injection, and downsized engines.

Economic impact is concentrated in factory-fill approvals, service-fill procurement, lubricant distributors, quick-lube networks, repair workshops, and fleet maintenance programs. North America synthetic engine oils industry benefits when suppliers align Group III, PAO-based, and ester-enhanced formulations with SAE viscosity grades, API licensing, and OEM warranty requirements. The North America synthetic engine oils market also improves inventory value for retailers because full synthetic engine oils carry stronger premium positioning than conventional oils and support differentiated shelf, workshop, and e-commerce strategies.

Hybrid vehicle growth, aging light-vehicle fleets, and stricter oil-performance transitions are shaping the 2026 trajectory. Suppliers are prioritizing GF-7-ready labels, 0W-16 and 0W-20 grades, high-mileage synthetic motor oil, and engine-cleanliness claims to defend demand as electrification changes oil-change frequency. The North America synthetic engine oils market is moving toward specification-led competition, where brand trust, certification visibility, distributor reach, and workshop recommendation strength determine supplier positioning.

North America Synthetic Engine Oils Market Growth Driver

Aging Fleets Tighten Service-Fill Demand

Aging vehicle parc dynamics are expanding service-fill demand because older engines require consistent oil-change discipline, stronger wear protection, and higher confidence in deposit control. The North America synthetic engine oils market gains from this maintenance intensity as vehicle owners, independent workshops, and fleet operators prioritize premium lubricants that can support longer ownership cycles. North America synthetic engine oils industry also benefits from high-mileage synthetic motor oil adoption, especially where repair avoidance, engine durability, warranty-aligned service practices, and recurring workshop purchase orders influence procurement and replenishment.

The average age of U.S. light vehicles reached 12.8 years in 2025, while the operating fleet expanded to 289 million light vehicles. This directly supports aftermarket lubricant throughput because larger, older fleets create recurring demand across quick-lube centers, auto parts retailers, dealerships, and independent repair shops, strengthening demand capture for synthetic oil suppliers.

North America Synthetic Engine Oils Market Challenge

Electrification and Specification Complexity Restrain Conversion

Electrification and longer recommended service intervals are creating a volume-side constraint for the synthetic engine oils market in North America. Battery electric vehicles do not require engine oil, while hybrids operate internal combustion engines differently and may extend certain service cycles. This shifts lubricant demand toward premium performance, OEM-approved synthetic lubricants, and hybrid vehicle synthetic lubricants, but it also narrows the addressable volume pool for suppliers dependent on conventional oil-change frequency.

Data from the U.S. Energy Information Administration indicates that about 22% of U.S. light-duty vehicles sold in 2025 were hybrid, battery electric, or plug-in hybrid vehicles, up from 20% in 2024. The shift complicates stocking decisions for distributors and service centers because procurement must balance GF-7 synthetic motor oils for modern ICE platforms with slower engine-oil demand from BEVs, creating sharper competition for available service-fill opportunities and visibility across retail, workshop, and fleet maintenance channels in 2026.

Unlock Market Intelligence

Explore the market potential with our data-driven report

North America Synthetic Engine Oils Market Trend

Low-Viscosity Standards Redefine Product Mix

Low-viscosity lubricant specification is reshaping the North America synthetic engine oils market as automakers pursue fuel economy, low-speed pre-ignition control, oxidation resistance, and timing-chain wear protection. API SQ and ILSAC GF-7 are pushing formulators toward lower-friction base oils, advanced additive technology, and clearer certification labeling. North America synthetic engine oils industry is therefore shifting from broad viscosity coverage toward standards-led product differentiation and stronger OEM-approved synthetic engine oils. This supports premium pricing discipline across synthetic motor oils market channels and stronger workshop recommendation consistency through regional 2026 service menus.

Infineum reported that first licensing of API-approved ILSAC GF-7 gasoline engine oils started on March 31, 2025, with GF-7A linked to the Starburst mark and GF-7B linked to the Shield mark for SAE 0W-16 oils. This accelerates shelf conversion and service-center training because distributors must align inventory, packaging, and recommendation systems with updated oil-quality identifiers while supporting low-viscosity synthetic engine oils.

North America Synthetic Engine Oils Market Opportunity

Hybrid and High-Mileage Platforms Open Premium White Space

Hybrid and high-mileage service-fill platforms create underpenetrated premium demand because these vehicles still need engine protection but require clearer lubricant matching. The North America synthetic engine oils market can capture value through hybrid vehicle synthetic lubricants, high-mileage synthetic motor oil, and advanced additive technology positioned for engine cleanliness, friction control, and longer oil drain interval lubricants. North America synthetic engine oils industry can also improve market access by aligning quick-lube menus with OEM-approved synthetic engine oils.

Valvoline states that Restore & Protect is a premium full synthetic motor oil available in SAE 0W-16, 0W-20, 5W-20, and 5W-30, and says it removes up to 100% of engine deposits with continuous use. This supports product-tier expansion because suppliers can differentiate on performance claims rather than only viscosity, strengthening pricing power across aftermarket and workshop channels through bundled education, product finders, distributor support, technician training programs, and inventory discipline for 2026 efficient channel uptake.

North America Synthetic Engine Oils Market Country Analysis

By Country

- The US

- Canada

- Mexico

- Rest of North America

The US holds 75% share by country because its vehicle parc, service-center density, retail lubricant availability, and fleet maintenance base are materially larger than Canada and Mexico. Demand concentration is supported by nationwide quick-lube chains, auto parts retailers, dealership networks, and independent workshops that convert OEM specifications into recurring service-fill purchases. The country also anchors supplier launches, GF-7 packaging transitions, and premium synthetic motor oil merchandising across North American automotive lubricants.

In January 2026 that U.S. auto sales rose about 2% in 2025 to roughly 16 million vehicles, with gas-powered trucks, SUVs, and hybrids driving most demand. This vehicle-mix profile strengthens lubricant procurement because ICE and hybrid platforms continue to need engine oil, while large U.S. service networks improve market access for Exxon Mobil Corporation, Shell plc, Valvoline Global Operations, Castrol Ltd, Chevron Corporation, and other listed suppliers across 2026 service-fill channels and inventory planning discipline.

Unlock Market Intelligence

Explore the market potential with our data-driven report

North America Synthetic Engine Oils Market Segmentation Analysis

By Product Type

- Full Synthetic Engine Oils

- Synthetic Blend Engine Oils

- High-Mileage Synthetic Engine Oils

- Racing and Performance Synthetic Engine Oils

- Low-SAPS and Emission-Compatible Synthetic Engine Oils

- Others

Full Synthetic Engine Oils hold 55% share under Product Type because performance expectations are concentrated around thermal stability, oxidation resistance, fuel efficiency, turbocharged engine oil compatibility, and high-mileage protection. The North America synthetic engine oils market favors full synthetic engine oil because OEM service recommendations, premium aftermarket oils, and longer-drain positioning make this product class more attractive for workshops, retailers, and fleet service providers. North America synthetic engine oils industry also uses full synthetic lines to strengthen brand differentiation.

Mobil lists Mobil 1 Extended Performance with 25,000 miles of protection and grades including 0W-20, 5W-20, 5W-30, and 10W-30, while its broader motor oil portfolio includes synthetic Euro and supercar formulations. This specification breadth supports full synthetic demand because suppliers can address mainstream vehicles, high-mileage engines, performance cars, and European OEM applications through one premium product architecture for synthetic oil demand in passenger vehicles and commercial fleet operations in service.

By End-Use Vehicle and Equipment Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy-Duty Trucks

- Buses and Coaches

- Two-Wheelers and Motorcycles

- Off-Highway and Construction Equipment

- Agricultural Equipment

- Marine Engines

- Stationary Engines and Power Generation

- Others

Passenger Cars hold 55% share under end-use vehicle and equipment type because the category generates dense service-fill frequency, broad SAE viscosity coverage, and strong aftermarket attachment through quick-lube centers, dealerships, and auto parts retailers. Passenger car motor oil demand is supported by gasoline vehicles, hybrids, turbocharged direct-injection engines, and aging private-use fleets. North America synthetic engine oils industry therefore treats passenger cars as the anchor for retail shelf planning and workshop recommendation systems.

The US passenger cars averaged 14.5 years in service in 2025, even as car registrations fell below 100 million for the first time since the early 1970s. This aging parc supports synthetic engine oil for passenger cars because older engines require consistent deposit control, wear protection, and viscosity stability, strengthening premium service-fill conversion despite slower new-car replacement and reinforcing demand from high-mileage maintenance cycles and regional service menu planning.

Various Market Players in North America Synthetic Engine Oils Market

The companies mentioned below are highly active in the North America synthetic engine oils market, occupying a considerable portion of the market and shaping industry progress.

- Phillips 66 Company

- Highline Warren LLC

- AMSOIL INC.

- Exxon Mobil Corporation

- Shell plc

- Valvoline Cummins Private Limited

- Castrol Ltd

- Chevron Corporation

- Lucas Oil Products Inc.

- Calumet Inc.

- Safety-Kleen Systems Inc.

- Old World Industries LLC

Market News & Updates

- Valvoline Cummins Private Limited, 2025:

Valvoline stated in Canada that its motor oil portfolio was GF-7 ready as new ILSAC GF-7 and API SQ lubricant standards took effect on March 31, 2025. The update aligns its North American service-fill offering with newer gasoline-engine requirements. It supports workshop and retail inventory conversion toward current low-viscosity, specification-compliant synthetic engine oils.

- AMSOIL INC., 2025:

AMSOIL updated its synthetic motor oil positioning in June 2025 with specialized formulations including 100% Synthetic Hybrid Motor Oil and OE 100% Synthetic Motor Oil that meet or exceed ILSAC GF-7 and API SQ standards. The update adds hybrid-focused and OE service-fill options for North American vehicles, supporting specification-led aftermarket demand across passenger cars and hybrid powertrains.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- North America Synthetic Engine Oils Market Policies, Regulations, and Standards

- North America Synthetic Engine Oils Market Production (Thousand Liters) Trend 2022-2032

- North America Synthetic Engine Oils Market Production (Thousand Liters) Trend By Product Type

- Full Synthetic Engine Oils

- Synthetic Blend Engine Oils

- High-Mileage Synthetic Engine Oils

- Racing and Performance Synthetic Engine Oils

- Low-SAPS and Emission-Compatible Synthetic Engine Oils

- Company Wise Production Plants and Statistics

- Installed Production Capacity

- Actual Production

- Planned Production Target

- North America Synthetic Engine Oils Market Production (Thousand Liters) Trend By Product Type

- North America Synthetic Engine Oils Market Pricing Analysis 2022-2032

- North America Synthetic Engine Oils Market Pricing Trend (USD/ Thousand Liters) 2022-2032

- North America Synthetic Engine Oils Market Pricing Trend (USD/ Thousand Liters) By Countries 2022-2032

- The US

- Canada

- Mexico

- North America Synthetic Engine Oils Market Pricing Trend (USD/Liter) By Product Type 2022-2032

- Full Synthetic Engine Oils

- Synthetic Blend Engine Oils

- High-Mileage Synthetic Engine Oils

- Racing and Performance Synthetic Engine Oils

- Low-SAPS and Emission-Compatible Synthetic Engine Oils

- North America Synthetic Engine Oils Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- North America Synthetic Engine Oils Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume Sold in Thousand Liters

- Market Segmentation & Growth Outlook

- By Product Type

- Full Synthetic Engine Oils- Market Insights and Forecast 2022-2032, USD Million

- Synthetic Blend Engine Oils- Market Insights and Forecast 2022-2032, USD Million

- High-Mileage Synthetic Engine Oils- Market Insights and Forecast 2022-2032, USD Million

- Racing and Performance Synthetic Engine Oils- Market Insights and Forecast 2022-2032, USD Million

- Low-SAPS and Emission-Compatible Synthetic Engine Oils- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Base Oil Type

- Group III and Group III+ Synthetic Base Oils- Market Insights and Forecast 2022-2032, USD Million

- Group IV PAO Synthetic Base Oils- Market Insights and Forecast 2022-2032, USD Million

- Group V Ester Synthetic Base Oils- Market Insights and Forecast 2022-2032, USD Million

- GTL-Derived Synthetic Base Oils- Market Insights and Forecast 2022-2032, USD Million

- Blended Synthetic Base Oil Formulations- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Viscosity Grade

- 0W-16 and Lower- Market Insights and Forecast 2022-2032, USD Million

- 0W-20- Market Insights and Forecast 2022-2032, USD Million

- 0W-30- Market Insights and Forecast 2022-2032, USD Million

- 5W-20- Market Insights and Forecast 2022-2032, USD Million

- 5W-30- Market Insights and Forecast 2022-2032, USD Million

- 5W-40- Market Insights and Forecast 2022-2032, USD Million

- 10W-30 and 10W-40- Market Insights and Forecast 2022-2032, USD Million

- 15W-40 and Above- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Engine Type

- Gasoline Engines- Market Insights and Forecast 2022-2032, USD Million

- Diesel Engines- Market Insights and Forecast 2022-2032, USD Million

- Hybrid Vehicle Engines- Market Insights and Forecast 2022-2032, USD Million

- CNG and LPG Engines- Market Insights and Forecast 2022-2032, USD Million

- Heavy-Duty Diesel Engines- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By End-Use Vehicle and Equipment Type

- Passenger Cars- Market Insights and Forecast 2022-2032, USD Million

- Light Commercial Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Heavy-Duty Trucks- Market Insights and Forecast 2022-2032, USD Million

- Buses and Coaches- Market Insights and Forecast 2022-2032, USD Million

- Two-Wheelers and Motorcycles- Market Insights and Forecast 2022-2032, USD Million

- Off-Highway and Construction Equipment- Market Insights and Forecast 2022-2032, USD Million

- Agricultural Equipment- Market Insights and Forecast 2022-2032, USD Million

- Marine Engines- Market Insights and Forecast 2022-2032, USD Million

- Stationary Engines and Power Generation- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- OEM and Factory Fill- Market Insights and Forecast 2022-2032, USD Million

- Aftermarket- Market Insights and Forecast 2022-2032, USD Million

- By Country

- The US

- Canada

- Mexico

- Rest of North America

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- The US Synthetic Engine Oils Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume Sold in Thousand Liters

- Market Segmentation & Growth Outlook

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Base Oil Type- Market Insights and Forecast 2022-2032, USD Million

- By Viscosity Grade- Market Insights and Forecast 2022-2032, USD Million

- By Engine Type- Market Insights and Forecast 2022-2032, USD Million

- By End-Use Vehicle and Equipment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Canada Synthetic Engine Oils Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume Sold in Thousand Liters

- Market Segmentation & Growth Outlook

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Base Oil Type- Market Insights and Forecast 2022-2032, USD Million

- By Viscosity Grade- Market Insights and Forecast 2022-2032, USD Million

- By Engine Type- Market Insights and Forecast 2022-2032, USD Million

- By End-Use Vehicle and Equipment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Mexico Synthetic Engine Oils Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Volume Sold in Thousand Liters

- Market Segmentation & Growth Outlook

- By Product Type- Market Insights and Forecast 2022-2032, USD Million

- By Base Oil Type- Market Insights and Forecast 2022-2032, USD Million

- By Viscosity Grade- Market Insights and Forecast 2022-2032, USD Million

- By Engine Type- Market Insights and Forecast 2022-2032, USD Million

- By End-Use Vehicle and Equipment Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Exxon Mobil Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shell plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Valvoline Cummins Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Castrol Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Chevron Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Phillips 66 Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Highline Warren LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AMSOIL INC.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lucas Oil Products Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Calumet Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Safety-Kleen Systems Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Old World Industries LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Exxon Mobil Corporation

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Base Oil Type |

|

| By Viscosity Grade |

|

| By Engine Type |

|

| By End-Use Vehicle and Equipment Type |

|

| By Sales Channel |

|

| By Country |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.