Nigeria Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade), By Region (North Central, North East, North West, South East, Others) ... Read more

|

Major Players

|

Nigeria Juice Market Statistics and Insights, 2026

- Market Size Statistics

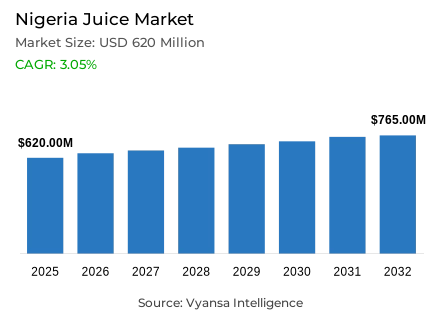

- Juice market size in Nigeria was estimated at USD 620 million in 2025.

- The market size is expected to grow to USD 765 million by 2032.

- Market to register a CAGR of around 3.05% during 2026-32.

- Category Shares

- Nectars grabbed market share of 45%.

- Competition

- More than 15 companies are actively engaged in producing juice in Nigeria.

- Top 5 companies acquired around 85% of the market share.

- New Age Beverages Ltd, Ranona Ltd, Fumman Foods Industries Nigeria Ltd, CHI Ltd, Coca-Cola Nigeria Ltd etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 90% of the market.

Nigeria Juice Market Outlook

The Nigeria juice market is in a stage of tentative recovery as end user adjust to a new price reality after the drastic contraction of 2024. The market is estimated to be USD 620 million in 2025 and USD 765 million in 2032 with a CAGR of about 3.05% in the 2026-32 forecast period. Although inflation and weak purchasing power are still issues, the unit price growth moderation and the growing child population in Nigeria are likely to result in healthy volume growth in the next few years.

The category remains dependent on health and social status. Juice is still an elegant substitute to carbonates especially during family get-togethers, religious festivals, and social functions. Although the adults are shifting towards fresh fruit to control the expenses, parents continue to give preference to packaged juice to children because of the perceived vitamins. The current market share of nectars is 45%, although the transition to cheaper juice beverages and smaller, school-friendly packaging is the main driver of the stabilization of the volume.

Innovation will target local sourcing and niche markets like not-from-concentrate (NFC) juice. With imported concentrates becoming costly due to currency depreciation, manufacturers are seeking to exploit the agricultural potential of Nigeria to create fresher, more authentic local juices. New trends in plant waters, pulpy beverages, and smoothies are also becoming popular among urbanites who are health conscious. The market leaders like CHI Ltd and Coca-Cola (Five Alive) are changing by offering more portable PET formats and balancing high-end products with mid-end accessibility.

The sales is well established in the retail business, with off-trade channels taking 90% of the market. Local grocers and kiosks are still the main points of sale because of their closeness to residential zones and the possibility to sell single-serving packs at affordable prices. But the most vibrant channel is the supermarkets, which are providing a broader range of high quality and imported products to the middle-income end user. These organised retail formats, which are backed by the increasing e-commerce platforms, will be instrumental in the long-term growth of the market as the economy improves.

Nigeria Juice Market Growth DriverRapid Population Growth Anchoring Family and Occasion-Led Juice Demand

The large and growing population of Nigeria supports a large pool of end user of juices, despite the constrained budgets. UNFPA estimates that the total population of the country will be 237.5 million by 2025, which will support the stable household demand of school-friendly packs and juice served at family events, where it is viewed as a symbol of hospitality and care. Parents still consider juice as a healthier choice over most of the sugary soft drinks and thus its role in family consumption events is still maintained despite the economic constraints on discretionary spending.

UNFPA also indicates that the annual doubling rate of the population is 24.8 years, which highlights the rate at which the end user base is being replenished by young families. This population trend grounds consumption on children and events, allowing the shopper to protect juice purchases by choosing low-cost pack sizes and extending the use instead of abandoning the category. The large population base and high rate of demographic renewal create a strong structural demand of juice based on family events, child feeding, and social hospitality settings, which contributes to category stability amid economic instability and affordability issues.

Nigeria Juice Market ChallengeCurrency Depreciation Elevating Input Costs and Retail Price Sensitivity

Packaged juice continues to be primarily cost driven by imported inputs, and the weakness of the currency makes it even harder to absorb the imported inputs. According to the Central Bank of Nigeria, the average exchange rate at the Nigerian Foreign Exchange Market stood at NGN 1,581.06 per USD in the second quarter of 2025, as compared to NGN 1,384.12 in the second quarter of 2024; this has significantly raised the cost of land, packaging materials, and processing equipment. As a result, the depreciation of currency generates a long-term inflationary strain on the cost of production and retail prices.

Due to the high unit costs, manufacturers and retailers are faced with unending affordability constraints. Shoppers who are price-sensitive restrict their purchases, switch to cheaper juice drinks, and buy less often, and the high-end one-hundred-percent juice is hard to justify compared to fresh fruit. This weakness in category recovery forces brands to defend margins by reducing pack-size and tightening route-to-market performance. The cost inflation based on currency puts structural limits on volume growth and premiumisation strategies, restricting the ability of manufacturers to increase higher-margin segments in the economically constrained end user environment in Nigeria.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Nigeria Juice Market TrendPack-Size Rationalisation and Occasion-Led Buying Reshaping Consumption Patterns

The challange of price pressure is still affecting the way the Nigerians buy packaged juice and the category is starting to act as a luxury item instead of a daily commodity. According to the Central Bank of Nigeria, the average exchange rate at the Nigerian Foreign Exchange Market is NGN 1,581.06 to the USD in the second quarter of 2025, which indicates that the cost pressure on imported inputs utilized in packaged beverages remains. This perpetuated currency weakness continues to pose affordability issues that redefine consumption patterns to more discriminating purchasing behaviour.

Households, in turn, save juice in budgets by down-trading and increased spend control. Customers choose small cartons and single-serving packages to use in school, extend their consumption to a longer time, and save larger amounts of purchases to use during celebrations and religious holidays. Adult end user who are conscious of costs and seeking nutrients are turning to fresh fruit, making packaged juice most resilient in low-end, child-oriented packaging. This is a tendency towards occasion-based consumption and format flexibility, which is strategic adjustment to economic pressures, where brands need to optimise pack-size portfolios and positioning strategies around preserved high-value consumption occasions.

Nigeria Juice Market OpportunityLocal Sourcing Strategies Mitigating FX Risk and Enabling Premium Differentiation

The cost pressure caused by currency provides a definite chance to the brands to minimize the exposure to imported concentrates and packaging inputs. As the foreign exchange market average is NGN 1,581.06 per USD in the second quarter of 2025, locally sourced fruit and domestic processing will be viable as a buffer against volatility and enhance cost management of packaged juice portfolios. This localisation approach has two advantages: cost stability and premium positioning by local provenance stories.

This transition favors two value-creation directions at the same time. Brands can stabilise prices of affordable juice drinks that serve families, and create premium space around not-from-concentrate juices and locally rooted plant waters that focus on freshness and clean labels. UNFPA projects that the population of Nigeria will reach 237.5 million in 2025 with a doubling time of 24.8 years, which gives it a size to develop both segments through child packs and multipacks to serve gatherings. Local sourcing allows brands to reduce foreign exchange risk and differentiate based on authenticity, freshness, and domestic economic contribution stories, thus establishing sustainable competitive advantages in the import-based beverage market of Nigeria.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Nigeria Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment has the highest share around the category in the Nigeria juice market, where Nectars grabbed a market share of 45%. This segment maintains its lead by successfully balancing the demand for a "juice" positioning with a price point that is more accessible than 100% pure juice. Nectars are particularly favored for social ceremonies and family hospitality, where they serve as a symbol of status. However, this segment has faced pressure from high production costs, leading many households to downtrade to smaller pack sizes to manage their budgets.

While nectars dominate, juice drinks (up to 24% juice) have become the most dynamic growth driver due to their extreme affordability and child-centric appeal. Parents often choose these as default options for school lunchboxes. Looking forward, as health consciousness rises, there is significant potential for the 100% juice segment to reclaim ground through locally sourced, not-from-concentrate variants that target upper-income end user seeking premium, authentic alternatives to reconstituted blends.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment has the highest share around the Sales Channel is Off-Trade, which grabbed 90% of the market. This dominance highlights the importance of home-based consumption and the role of traditional retail in Nigerian daily life. Small local grocers and neighborhood kiosks are the backbone of this channel, providing essential proximity for both planned purchases and impulse buys of single-serve cartons. Their ability to cater to daily cash flow realities by offering smaller, lower-priced units has kept the category resilient during periods of high inflation.

In contrast, modern supermarkets are the most dynamic sub-channel, expanding their footprint closer to residential areas to attract middle-class urbanites. These outlets offer a broader assortment of premium brands and bulk-purchase options for events. E-commerce is also gaining a foothold among higher-income end user who value the convenience of home delivery for heavy multipacks. While on-trade consumption remains a smaller niche, the off-trade retail environment will continue to be the primary engine of the USD 765 million market through 2032.

List of Companies Covered in Nigeria Juice Market

The companies listed below are highly influential in the Nigeria juice market, with a significant market share and a strong impact on industry developments.

- New Age Beverages Ltd

- Ranona Ltd

- Fumman Foods Industries Nigeria Ltd

- CHI Ltd

- Coca-Cola Nigeria Ltd

- FMCG Distribution Ltd

- Cway Food & Beverages Co Nig Ltd

- Frutta Juice & Services Ltd

- Vital Products Ltd

- Niyya Food & Drinks Co Ltd

Competitive Landscape

Nigeria’s juice market in 2025 is led by CHI Ltd, leveraging strong brand equity (Chi/Chivita) and breadth across reconstituted 100% juice, nectars, and child-focused formats (incl. licensed Capri-Sun), but facing share pressure as consumers downtrade. Coca-Cola Nigeria is the most dynamic branded challenger as Five Alive rebounds, supported by superior route-to-market and marketing scale. Value-oriented juice drinks (≤24% juice) are the core volume battleground, with brands such as Zico competing on affordability and small packs, while premium 100% juice and nectars remain constrained by high prices and substitution toward fresh fruit. Indirect competitors include carbonates and low-cost refreshment drinks, plus fresh fruit consumption for “nutrition.” Differentiation opportunities centre on locally sourced not-from-concentrate propositions, credible reduced-sugar/clean-label claims, portable school formats, and wider access via supermarkets and e-commerce for multipacks and event-led purchases.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Nigeria Juice Market Policies, Regulations, and Standards

- Nigeria Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Nigeria Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North Central

- North East

- North West

- South East

- Others

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Nigeria 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Nigeria Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Nigeria Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Nigeria Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Nigeria Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- CHI Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coca-Cola Nigeria Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- FMCG Distribution Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cway Food & Beverages Co Nig Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Frutta Juice & Services Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- New Age Beverages Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ranona Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fumman Foods Industries Nigeria Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vital Products Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Niyya Food & Drinks Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CHI Ltd

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.