New Zealand Sports Nutrition Market Report: Trends, Growth and Forecast (2026-2032)

Product Type (Sports Protein Products (Protein/Energy Bars, Sports Protein Powder, Sports Protein RTD), Sports Non-Protein Products), Sales Channel (Retail Offline, Retail Online), Ingredients (Vitamins and Minerals, Proteins and Amino Acids, Carbohydrates, Probiotics, Botanicals/Herbals, Others), Functionality (Energy, Muscle growth, Hydration, Weight Management, Others), End User (Bodybuilders, Athletes, Lifestyle Users) ... Read more

|

Major Players

|

New Zealand Sports Nutrition Market Statistics and Insights, 2026

- Market Size Statistics

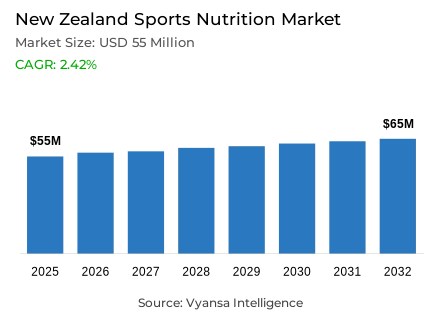

- Sports nutrition in New Zealand is estimated at USD 55 million.

- The market size is expected to grow to USD 65 million by 2032.

- Market to register a cagr of around 2.42% during 2026-32.

- Product Type Shares

- Sports protein products grabbed market share of 90%.

- Competition

- More than 10 companies are actively engaged in producing sports nutrition in New Zealand.

- Top 5 companies acquired around 55% of the market share.

- Axis Labs Inc; Red Seal Natural Health Ltd; Cytosport Inc; Vitaco Health NZ Ltd; Naturalac Nutrition Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 65% of the market.

New Zealand Sports Nutrition Market Outlook

The New Zealand sports nutrition market is estimated at around USD 55 million in 2025 and is projected to reach around USD 65 million by 2032, expanding at a CAGR of around 2.42% during 2026-2032. The market continues to grow as more end users focus on fitness, health, and overall wellbeing. The rising interest in nutrition based products after the pandemic has expanded the end user base beyond athletes, now many end users use these products to improve strength, recovery, and immunity.

The sports protein products dominate the market with around 90% share, supported by strong demand for protein powders and other items based on proteins. The well developed dairy industry of the country allows easy access to whey and casein, thereby keeping supply steady and production cost effective. The growing use of these products in everyday fitness routines ensures the segment's continued strength during the forecast period.

By sales channel, the retail offline segment leads with around 65% of total sales. Most end users still prefer to buy from supermarkets, pharmacies, and specialty stores offering product visibility and trust in quality. Though retail online sales are growing, retail offline remains the main source of purchase due to its convenience factor and personal assurance it carries.

Competition in the market remains strong, with more than 10 companies actively involved in production. The top five players account for around 55% of the total market share, showing a moderate level of concentration. Despite this, the presence of smaller local brands keeps the market competitive and encourages continued product innovation and category development.

New Zealand Sports Nutrition Market Growth DriverRising Focus on Wellness Expands Sports Nutrition Market

Post pandemic, end users are now becoming more focused towards improving their health, fitness, and immunity. This has increased the usage of sports nutrition products beyond its traditional end users such as athletes and bodybuilders. For most end users, sports nutrition products support their daily routine, from pre-workout to recovery, with each stage having its formulation and product. According to the Ministry of Business, Innovation and Employment (MBIE), New Zealand domestic sports nutrition and weight management market was valued at around USD 94.36 million in 2022, showing stable long term expansion. This rising understanding of nutrition’s role in overall wellbeing is leading to steady and balanced growth across all categories.

Additionally, while end users continue to seek products that improve focus, energy, and sleep, companies are expanding their product lines to meet these evolving needs. Nutrition surveys by the Ministry of Health show that 70% of adults now report being mindful of the food they consume every day, indicating strong awareness of nutrition and wellness across the country. This ongoing health focus is laying a lasting foundation of demand that is supporting both volume and value growth for sports nutrition in the country.

New Zealand Sports Nutrition Market ChallengeHeavy Segmentation Creating Market Saturation

The country's strong dairy sector gives manufacturers easy access to whey and casein ingredients. However, this abundance has also led to a fragmented sports nutrition market, with many local players entering the space. Such conditions have encouraged the entry of a large number of local manufacturers, which have in turn resulted in a very strong competition within the sports protein category. According to MBIE, the expansion of this sector is supported by a large number of small scale manufacturers, that makes product differentiation very hard to achieve and this continues to puts pressure on pricing. It is hard for smaller companies to gain visibility in stores that have been already dominated by established players.

At the same time, the end users have a strong preference for locally manufactured products, which limits the market share of imported products. According to data from MBIE, domestic dairy processing capacity has grown more rapidly than demand, further feeding oversupply in protein ingredients. This environment has resulted in a crowded market where innovation is harder to achieve, forcing companies to compete within a price sensitive segment filled with similar dairy based products.

Unlock Market Intelligence

Explore the market potential with our data-driven report

New Zealand Sports Nutrition Market TrendRising Interest in Plant Based Protein Alternatives

As market is undergoes a transition, a growing number of end users are opting for plant based protein products instead of conventional dairy based products. End users who are concerned about sustainability and environmental impact are making these purchasing decisions, with many looking to reduce their dairy consumption. According to the MPI, plant proteins already accounts for about 40% of adults daily protein intake, clearly showing end users movement toward multiple sources of protein. This is creating momentum for new innovations in the segment.

At the same time, plant based proteins are still developing in terms of texture and taste, but the increasing demand pushes manufacturers to work on product quality. According to MPI 2023 report, government initiatives for sustainable food production support the development of plant based protein. The shift of moving toward plant based protein is expected to be much stronger in the coming years, as awareness spreads and experience of end users improves with the usage of protein products.

New Zealand Sports Nutrition Market OpportunityStrong Growth Potential for Protein/Energy Bars

The growing demand for protein and energy bars provides a clear path for the expansion of the sports nutrition market. The end users are more attracted to these products due to their enhanced taste, variety, and convenience. Over the last couple of years, manufacturers have launched several new flavors and textures, making protein and energy bars more suitable for daily consumption. According to MBIE this broad sports nutrition category has maintained a strong compound annual growth rate of 8-12% over the last ten years, reflecting overall momentum across protein formats. This steady rise in everyday use of the protein and energy bars signals toward a promising path for expansion.

Meanwhile, sports protein RTD products have shown limited innovation in taste and texture development. With fewer updates and weaker appeal, sports protein RTD is expected to see slower growth. This would give a clear chance for manufacturers to invest more in the development and refinement of their protein and energy bars to capture stronger market performance in the coming years.

Unlock Market Intelligence

Explore the market potential with our data-driven report

New Zealand Sports Nutrition Market Segmentation Analysis

By Product Type

- Sports Protein Products

- Sports Non-Protein Products

Sports protein products dominate the market, accounting for around 90% of total sports nutrition sales. This strong position comes from the high popularity of protein powders, which are widely used by end users to support fitness goals, muscle recovery, and active lifestyles. Further, the strong dominance of the segment is supported by New Zealand's strong dairy base, which provides easy access to whey and casein ingredients which are generally used in the production of protein. This availability has encouraged continuous product development and steady demand across the nation.

At the same time, interest in protein based products from both regular end users engaged in fitness activities and to the sports professionals supports the large market share of this category. The growing focus on health and performance has made protein products a part of daily routines, thus making it the most favored and reliable product in the sports nutrition market from 2026 to 2032.

By Sales Channel

- Retail Offline

- Retail Online

The retail offline channel dominates the market with around 65% share of the overall sales. A majority of end user still prefer to purchase from retail offline outlets like supermarkets, pharmacies, and speciality stores. These outlets give end users a chance to check labels, compare ingredients of various products, and take advice from staff at the outlet. Such levels of trust built through direct interaction make end users confident about product quality and safety, especially for those products that are related to health like protein powders and energy bars.

At the same time, regular discounts and attractive in-store displays offered by retail offline stores attract end users. The wide availability of products across cities and towns keeps retail offline shopping convenient and reliable. While retail online sales are certainly on the rise, retail offline remains strong due to the habit of end user doing in-store shopping and the assurance of it gives to health conscious end users.

List of Companies Covered in New Zealand Sports Nutrition Market

The companies listed below are highly influential in the New Zealand sports nutrition market, with a significant market share and a strong impact on industry developments.

- Axis Labs Inc

- Red Seal Natural Health Ltd

- Cytosport Inc

- Vitaco Health NZ Ltd

- Naturalac Nutrition Ltd

- Glanbia Performance Nutrition Pty Ltd

- Tasti Products Ltd

- Integria Healthcare (NZ) Ltd

- Brittain Wynyard & Co Ltd

- Cookie Time Ltd

Market News & Updates

- Vitaco Health NZ, 2024:

Vitaco Health NZ Ltd launched a new women-focused sports nutrition brand called ATHENA Sports Nutrition in 2024.

- Tasti Products Ltd, 2023:

Introduced a protein packed muesli range ("Tasti Toasted Protein Nut Muesli") with 12 g protein per serve, targeting active consumers at breakfast.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. New Zealand Sports Nutrition Market Policies, Regulations, and Standards

4. New Zealand Sports Nutrition Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. New Zealand Sports Nutrition Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Sports Protein Products- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Protein/Energy Bars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Sports Protein Powder- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Sports Protein RTD- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Sports Non-Protein Products- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sales Channel

5.2.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Ingredients

5.2.3.1. Vitamins and Minerals- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Proteins and Amino Acids- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Carbohydrates- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Probiotics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Botanicals/Herbals- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Functionality

5.2.4.1. Energy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Muscle growth- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Hydration- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Weight Management- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By End User

5.2.5.1. Bodybuilders- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Athletes- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Lifestyle Users- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. New Zealand Protein Products Sports Nutrition Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Ingredients- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Functionality- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By End User- Market Insights and Forecast 2022-2032, USD Million

7. New Zealand Non-Protein Products Sports Nutrition Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Ingredients- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Functionality- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Vitaco Health NZ Ltd

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Naturalac Nutrition Ltd

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.Glanbia Performance Nutrition Pty Ltd

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Tasti Products Ltd

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Integria Healthcare (NZ) Ltd

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Axis Labs Inc

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.Red Seal Natural Health Ltd

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Cytosport Inc

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Brittain Wynyard & Co Ltd

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. Cookie Time Ltd

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Sales Channel |

|

| By Ingredients |

|

| By Functionality |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.