Netherlands Juice Market Report: Trends, Growth and Forecast (2026-2032)

By Category (100% Juice (Not from Concentrate, Reconstituted), Juice Drinks (up to 24% Juice), Nectars (High Concentration (40% to 50% fruit content), Medium Concentration (30% to 39% fruit content), Low Concentration (25% to 29% fruit content)), Vegetable Juice, Fruit and Vegetable Blends), By Nature (Conventional, Organic), By Packaging Material (Plastic, Glass, Metal, Others), By Packaging Type (PET Bottles, Aseptic Packages (Cartons), Glass Bottles, Metal Cans, Disposable Cups & Pouches), By Sales Channel (Off-Trade (Hypermarkets/ Supermarkets, Retail Outlets, Convenience Stores, Online Platforms), On-Trade) ... Read more

|

Major Players

|

Netherlands Juice Market Statistics and Insights, 2026

- Market Size Statistics

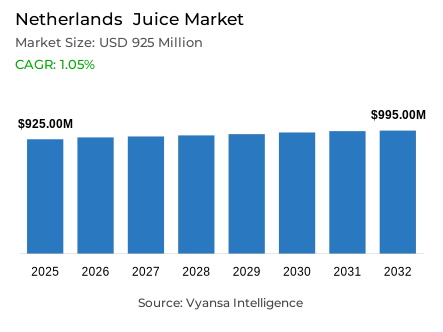

- Juice market size in Netherlands was estimated at USD 925 million in 2025.

- The market size is expected to grow to USD 995 million by 2032.

- Market to register a CAGR of around 1.05% during 2026-32.

- Category Shares

- 100% juice grabbed market share of 51%.

- Competition

- More than 15 companies are actively engaged in producing juice in Netherlands .

- Top 5 companies acquired around 65% of the market share.

- Spadel Nederland BV, Coca-Cola Enterprises Nederland BV, Menken Drinks BV, Riedel Drankenindustrie BV, Albert Heijn BV etc., are few of the top companies.

- Sales Channel

- Off-trade grabbed 75% of the market.

Netherlands Juice Market Outlook

The Netherlands juice market is already in a phase of volume loss with price spikes and health issues redefining end user demand. The market is estimated to be USD 925 million in 2025 and is expected to increase to USD 995 million by 2032 with a CAGR of about 1.05% within the 2026-32 period. Although total value has been positive because of large price gains that have been mainly caused by a global orange shortage and unfavorable weather in Brazil and the EU, overall consumption pressure is still under pressure as shoppers rethink their habits.

Sugar content is being questioned more by health-conscious end users, and many are moving to lower-sugar options like flavoured water and RTD tea. However, there is a less but better trend that favors high-end segments; upmarket, healthy positioning products like Innocent have been more resilient because shoppers are ready to pay higher prices on beverages that meet their nutritional requirements. Moreover, new growth opportunities are anticipated to be offered by innovations in functional juices, including protein-fortified or gut-health-focused ones.

The landscape is also being influenced by regulatory changes. By 2027, the Dutch government plans to seal a tax loophole so that juices with low levels of dairy which brands like Riedel have used to evade soft-drink taxes will be subject to the same high tax rates as ordinary juice. This legislative shift will likely even the playing field but will continue to strain volume sales throughout the category.

The Off-Trade channel is very much anchored on distribution and still dominates. Supermarkets continue to be the main place of buying large-format juices when people go shopping once a week. Meanwhile, retail e-commerce is becoming popular among heavy users who enjoy price discounts and convenience of bulk-buying. Brands are also concentrating on functional advantages and clear labeling to win back health-conscious Dutch end users to be competitive.

Netherlands Juice Market Growth DriverHealth Focus Lifts Premium Juice Demand

The health consciousness is still driving the demand of the high-end and functional juice products. According to official statistics, 51% of adults aged 20 and above in the Netherlands were overweight in 2023, which shows that the issue of diet and sugar intake is a common concern. end users thus selectively buy juices that are promoted as natural or nutrient-enriched, and are willing to pay more to buy health-conscious juices. This health burden creates a structural need to position better-for-you juice in different income groups and demographic groups.

This behaviour change is supported by government dietary guidelines. The World Health Organization recommends that free sugars should be less than 10% of daily energy consumption, which makes traditional high-sugar juices less appealing. Brands that focus on no-added-sugar or gut-health ingredients are, therefore, in a better position to gain growth among health-conscious end users. The shift in demand due to health provides favourable conditions to the innovation of premium juice, as brands can differentiate based on functional benefits, clear nutrition communication, and evidence-based positioning. This trend underpins the long-term value growth in the Netherlands juice market despite the general volume pressure due to price sensitivity and health-motivated substitution to lower-sugar beverage substitutes.

Netherlands Juice Market ChallengeExcise Tax and Citrus Costs Pressure Volumes

Market players are faced with significant structural cost pressures. The Netherlands has had a flat excise tax of €0.2613 per litre on virtually all non-alcoholic beverages, such as fruit juices, since January 2024, which is a significant increase over the previous rate of €0.0883 per litre that was in place before 2024. This high tax directly increases the cost of juice products, squeezes the margins of manufacturers, and decreases end user affordability at the same time. The cost pressures of regulation impose long-term pricing pressures throughout the category.

At the same time, world supply shocks tighten margins even more. Unfavorable weather and drought in major orange-producing areas have significantly increased the cost of raw materials. Together, increased commodity prices and taxation have the most adverse effects on mainstream orange-juice-based products. Orange-based low-end 100% juices experience decreases in volume, whereas only high-end or niche juices show relative stability. The interplay between fiscal policy and commodity volatility generates two structural headwinds. Manufacturers are forced to deal with rising input prices and absorb taxation, forcing them to respond strategically by reformulating, premiumising, diversifying their fruits, and optimising their supply chains to ensure they remain competitive in the competitive cost environment in the Netherlands.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Netherlands Juice Market TrendOn-Trade and E-Commerce Reshape Consumption

Out-of-home channels are taking off in the Netherlands juice market. According to Dutch statistics, foodservice turnover in Q3 2025 will be 4.6% higher than in the prior year. This is indicative of the increasing popularity of fresh, made-to-order juice products in cafes and restaurants, which are becoming on-trade channels that are becoming more important distribution channels and consumption-occasion drivers outside of the traditional retail formats.

This trend is further supported by digital ordering. In late 2024, Dutch retail e-commerce turnover grew 12.5% year-on-year, growing online purchasing as a normalised beverage procurement channel. Practically, juice brands are expanding into on-trade and online platforms, leveraging them to sell customisable, freshly pressed juices in line with the wider increases in out-of-home beverage consumption. Channel evolution opens strategic opportunities to brands that can build an omnichannel presence, format to on-trade service, and use digital commerce infrastructure to access convenience-oriented, health-conscious end users seeking fresh and high-quality alternatives in changing Dutch consumption trends.

Netherlands Juice Market OpportunityFunctional and Sustainable Innovation Drive Value

Health and sustainability-based product innovation provides significant growth potential. Juice can also differentiate by incorporating functional ingredients like vitamins, fibre, and probiotics to respond to end user wellness trends. Health claims approved by EFSA allow some juices that are fortified with plant sterols to be promoted as heart-healthy, which allows premium positioning and clinical differentiation in competitive retail markets. Functional innovation helps brands to rebrand juice as an active wellness product, which was previously a breakfast staple.

There are other competitive advantages of environmental factors. The Dutch government is shifting towards more stringent beverage-packaging laws, such as new excise laws on drinks with dairy starting in 2027. Companies that invest in sustainable packaging and emphasize sustainability-related credentials can build loyalty among the environmentally conscious customers. This regulatory shift balances competition and provides differentiation opportunities to manufacturers who are committed to sustainability. Brands with lower sugar levels and authentic nutritional value and sustainability will rejuvenate category appeal, take premium positions, and create defensible competitive positions in the Netherlands health-conscious, sustainability-oriented market that is estimated to grow to USD 995 million by 2032.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Netherlands Juice Market Segmentation Analysis

By Category

- 100% Juice

- Not from Concentrate

- Reconstituted

- Juice Drinks (up to 24% Juice)

- Nectars

- High Concentration (40% to 50% fruit content)

- Medium Concentration (30% to 39% fruit content)

- Low Concentration (25% to 29% fruit content)

- Vegetable Juice

- Fruit and Vegetable Blends

The segment that has the largest share in the category division is 100% Juice, which has a market share of 51%. This category is now split between reconstituted juices, which are exposed to extreme price pressures due to the rise in the cost of orange concentrate, and not-from-concentrate alternatives that are proving more resilient. Whereas mainstream reconstituted products suffer a high volume loss because of price sensitivity, premium not-from-concentrate brands are stable because of their appeal to lifestyle-oriented demographics who do not consider price as a factor in their purchasing decisions.

The 100% juice segment is an area where innovation is important to the future stability. With end users shifting towards less traditional fruit-sugar associations, manufacturers are considering naturally low-sugar options and functional additions like protein or gut-health probiotics. The segment will shift the traditional breakfast item into an active wellness product by positioning 100% juice as a natural carrier of functional wellness benefits. This repositioning allows the segment to retain majority market share even in the face of broader volume pressures, and attract health-conscious end users who are willing to pay a premium to purchase functionally differentiated juice products that provide real nutritional value beyond simple fruit content.

By Sales Channel

- Off-Trade

- Hypermarkets/ Supermarkets

- Retail Outlets

- Convenience Stores

- Online Platforms

- On-Trade

The segment that has the largest share in the sales-channel division is the Off-Trade that takes about 75% of the total market sales. The main driver in this channel is supermarkets, and Dutch families usually buy 1-litre and 1.5-litre cartons as a part of routine weekly shopping. Despite slight distribution-share softening of supermarkets as unit prices increase, they continue to be key purchasing touchpoints to mainstream brands like Riedel, and they dominate by offering wide access, promotion, and end user shopping behavior.

The retail e-commerce is the most rapidly expanding sub-channel in the off-trade sector, and it is especially attractive to regular buyers who stock up on preferred brand units. Online shopping is a good alternative to end users who want to stock up during price promotions in the Dutch market. With the ongoing improvement of digital infrastructure and the desire of end users to have improved value propositions, the off-trade channel, namely online supermarkets, will remain the foundation of juice distribution in the Netherlands, offering convenience, competitive pricing, and wide product range to facilitate long-term category accessibility up to the 2032 forecast horizon.

List of Companies Covered in Netherlands Juice Market

The companies listed below are highly influential in the Netherlands juice market, with a significant market share and a strong impact on industry developments.

- Spadel Nederland BV

- Coca-Cola Enterprises Nederland BV

- Menken Drinks BV

- Riedel Drankenindustrie BV

- Albert Heijn BV

- Bickery Food Group BV

- Jumbo Supermarkten BV

- Fruity King Vers Sap BV

- Heinz BV, HJ

- Aldi Nederland BV

Competitive Landscape

Netherlands juice market is characterised by declining volumes, cost inflation, and health-driven shifts, with Riedel remaining the category leader through its portfolio of mainstream brands but struggling amid orange price spikes and tax-related reformulations that have diluted consumer appeal. Its strategy of launching lower-juice, dairy-containing variants to mitigate tax pressures highlights defensive positioning rather than demand-led innovation. In contrast, Innocent, distributed by Bickery Food Group, demonstrates relative resilience, leveraging a premium, health-oriented smoothie and juice shot positioning that attracts less price-sensitive consumers. Private label and mainstream reconstituted 100% juice face the steepest declines, while indirect competition from flavoured water, RTD tea, and functional beverages intensifies. Differentiation opportunities lie in credible low-sugar formulations, gut health functionality, transparent pricing, and authentic premium positioning beyond tax optimisation tactics.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- Netherlands Juice Market Policies, Regulations, and Standards

- Netherlands Juice Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- Netherlands Juice Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Category

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- Not from Concentrate- Market Insights and Forecast 2022-2032, USD Million

- Reconstituted- Market Insights and Forecast 2022-2032, USD Million

- Juice Drinks (up to 24% Juice)- Market Insights and Forecast 2022-2032, USD Million

- Nectars- Market Insights and Forecast 2022-2032, USD Million

- High Concentration (40% to 50% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Medium Concentration (30% to 39% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Low Concentration (25% to 29% fruit content)- Market Insights and Forecast 2022-2032, USD Million

- Vegetable Juice- Market Insights and Forecast 2022-2032, USD Million

- Fruit and Vegetable Blends- Market Insights and Forecast 2022-2032, USD Million

- 100% Juice- Market Insights and Forecast 2022-2032, USD Million

- By Nature

- Conventional- Market Insights and Forecast 2022-2032, USD Million

- Organic- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material

- Plastic- Market Insights and Forecast 2022-2032, USD Million

- Glass- Market Insights and Forecast 2022-2032, USD Million

- Metal- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type

- PET Bottles- Market Insights and Forecast 2022-2032, USD Million

- Aseptic Packages (Cartons)- Market Insights and Forecast 2022-2032, USD Million

- Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

- Metal Cans- Market Insights and Forecast 2022-2032, USD Million

- Disposable Cups & Pouches- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- Hypermarkets/ Supermarkets - Market Insights and Forecast 2022-2032, USD Million

- Retail Outlets - Market Insights and Forecast 2022-2032, USD Million

- Convenience Stores- Market Insights and Forecast 2022-2032, USD Million

- Online Platforms- Market Insights and Forecast 2022-2032, USD Million

- On-Trade- Market Insights and Forecast 2022-2032, USD Million

- Off-Trade- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Category

- Market Size & Growth Outlook

- Netherlands 100% Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Netherlands Juice Drinks (up to 24% Juice) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Netherlands Nectars Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Netherlands Vegetable Juice Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Netherlands Fruit and Vegetable Blends Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- By Quantity Sold in Million Litres

- Market Segmentation & Growth Outlook

- By Nature- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Material- Market Insights and Forecast 2022-2032, USD Million

- By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Riedel Drankenindustrie BV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Albert Heijn BV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bickery Food Group BV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Jumbo Supermarkten BV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fruity King Vers Sap BV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Spadel Nederland BV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coca-Cola Enterprises Nederland BV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Menken Drinks BV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Heinz BV HJ

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aldi Nederland BV

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Riedel Drankenindustrie BV

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Category |

|

| By Nature |

|

| By Packaging Material |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.