Mexico Water Pump Market Report: Trends, Growth and Forecast (2026-2032)

By Pump Type (Centrifugal Pumps, Positive Displacement Pump), By End User (Oil & Gas, Power, Residential, Agriculture & Irrigation, Commercial Building, HVAC, Chemical, Water & Wastewater, Food & Beverage, Others) ... Read more

|

Major Players

|

Mexico Water Pump Market Statistics and Insights, 2026

- Market Size Statistics

- Water Pump in Mexico is estimated at $ 405 Million.

- The market size is expected to grow to $ 450 Million by 2032.

- Market to register a CAGR of around 1.52% during 2026-32.

- Pump Type Segment

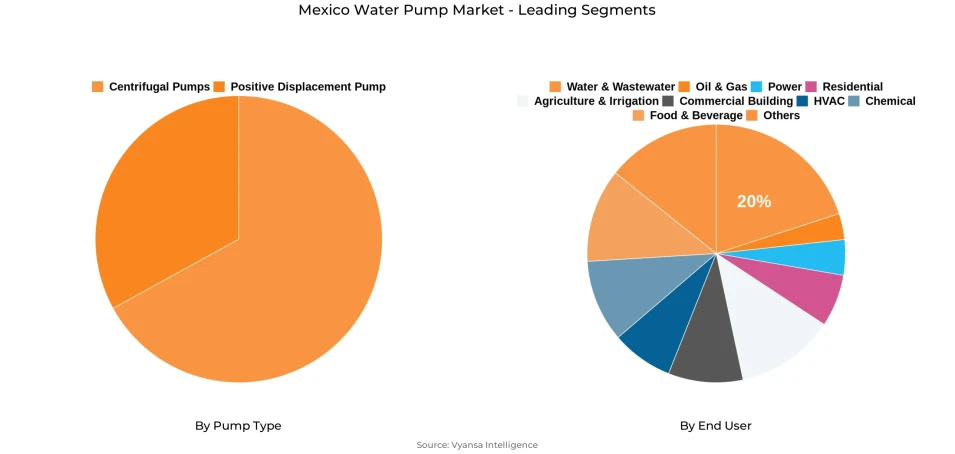

- Centrifugal Pumps continues to dominate the market.

- Competition

- More than 10 companies are actively engaged in producing Water Pump in Mexico.

- Top 5 companies acquired the maximum share of the market.

- ITT, IDEX, Dover, Flowserve, Sulzer AG etc., are few of the top companies.

- End User

- Water & Wastewater grabbed 20% of the market.

Mexico Water Pump Market Outlook

Mexico water pump market is estimated at $405 million in 2025 and it is expected to touch $450 million in 2032. Growth in the market comes from urbanization at a fast pace, with 78% of the total population concentrated in urban regions, putting more pressure on water infrastructure and boosting demand for efficient water pump solutions to serve residential, commercial, and municipal water networks. Mexican construction activity is expanding, with manufacturing levels rising by 6.3% year-on-year in 2024, further driving the demand for effective water pumps in infrastructure development.

Government policies are instrumental in driving this market growth. Mexico's National Infrastructure Fund has committed $3.5 billion over three years for water management initiatives, while the 2024-2030 National Water Plan includes major infrastructure such as aqueducts and desalination facilities. These initiatives drive long-term demand for various types of water pumps to facilitate efficient water flow and pressure control in growing urban areas.

Water & Wastewater represents the largest end-use market segment with 20% market share, which addresses the country's desperate need to upgrade obsolete water infrastructure. Mexico City loses approximately 40% of its water through leaks, and overall water losses across the country average 51%, projecting the urgent need for updated pumping systems to curtail inefficiencies and enhance water delivery.

Competition prevails in the market, with over five companies actively manufacturing water pumps in Mexico. The leader of these companies has the greatest market share, reflecting consolidation in the industry. Increased investment in intelligent water management technology and farming modernization also present new opportunities, setting the water pump market for stable growth through 2032.

Mexico Water Pump Market Growth Driver

Growing Urbanization and Infrastructure Development Driving Market Growth

Mexico is witnessing fast urbanization with 78% of the population residing in urban areas, putting heavy pressure on water infrastructure systems. Infrastructure development in the country is speeding up with manufacturing volumes of construction going up by 6.3% year-over-year during the first nine months of 2024, as spurred by specialized construction activities and civil engineering works. This urbanization has direct implications in terms of demand for sound water pumping solutions for supporting residential complexes, commercial premises, and municipal water distribution networks.

Government programs further reinforce this trend, with USD 3.5 billion distributed by Mexico's National Infrastructure Fund in water management development programs for the next three years. The 2024-2030 National Water Plan also launches strategic infrastructure projects such as aqueducts, desalination, and flood defense works in several states. These projects create long-term demand for various configurations of water pumps to guarantee efficient water flow, pressure regulation, and an assured supply system in growing cities.

Mexico Water Pump Market Challenge

Aging Water Infrastructure and Distribution Losses

Mexico has critical problems with deteriorating water infrastructure that generates high water losses along distribution systems. Mexico City alone loses around 40% of its water from leaking pipes and system deficiencies, posing a significant operational issue. Across the country, the average non-revenue water percentage increases to 51%, highlighting huge inefficiencies in water delivery systems. This generates pressing needs for infrastructure renewal and modernization across municipal water networks.

The weakening infrastructure has a direct effect on service quality, as 55% of Mexicans get water only intermittently based on census figures. Such infrastructure constraints compel municipalities to spend money on replacement pumping systems and improved distribution networks. Moreover, years of neglect have accumulated a backlog of maintenance that needs urgent attention, especially in urban centers where water demand keeps increasing while supply systems are not capable of providing sufficient service levels.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Mexico Water Pump Market Trend

Smart Water Management Technology Integration

Mexico advances rapidly toward digital water management systems with significant technology adoption across municipalities and utilities. The rollout of one million smart water meters across Mexico over a 10-year period represents a major technological transformation in water measurement and monitoring. Leading utilities like Servicios de Agua y Drenaje de Monterrey achieve overall water savings of 17%, with some sectors reaching 37% through smart pressure, flow, and consumption monitoring systems.

Digital agriculture projects grow over 30,000 hectares benefiting 4,000 producers, with implementation scheduled for Sinaloa and other states by 2024. The farming industry, which accounts for 76% of Mexico's water consumption, enjoys IoT-based monitoring systems that enhance water efficiency and minimize waste. Such technology provides new market opportunities in smart pumping solutions that are integrated into digital management systems, possessing real-time monitoring, predictive maintenance, and optimized performance features.

Mexico Water Pump Market Opportunity

Agricultural Modernization and Water Efficiency Programs

Mexico inaugurates the National Irrigation Technology Program with investment of 51.8 billion pesos (around USD 2.6 billion) to irrigate more than 200,000 hectares of farmland in 13 irrigation districts. The program supports no less than 225,000 agricultural producers and is expected to save as much as 50% of water use through implementation of new irrigation technologies. This project diverts 2.8 billion cubic meters of water - equivalent to three times Mexico City's usage - away from agriculture and into human consumption purposes.

Agriculture uses 76% of Mexico's overall water usage, so making improvements to efficiency is imperative to national water security. Technification of irrigation systems is the target of government programs, with more than 5.2 billion pesos spent in 2025 alone on modernization. All these investments make for tremendous opportunities for sophisticated pumping solutions that enable precision irrigation, less water wastage, and enhanced productivity of crops while addressing sustainability goals for water resource management.

| Report Coverage | Details |

|---|---|

| Market Forecast | 2026-32 |

| USD Value 2025 | $ 405 Million |

| USD Value 2032 | $ 450 Million |

| CAGR 2026-2032 | 1.52% |

| Largest Category | Centrifugal Pumps segment leads the market |

| Top Drivers | Growing Urbanization and Infrastructure Development Driving Market Growth |

| Top Challenges | Aging Water Infrastructure and Distribution Losses |

| Top Trends | Smart Water Management Technology Integration |

| Top Opportunities | Agricultural Modernization and Water Efficiency Programs |

| Key Players | ITT, IDEX, Dover, Flowserve, Sulzer AG, KSB, Xylem, Grundfos, Ebara, SPX Flow and Others. |

Unlock Market Intelligence

Explore the market potential with our data-driven report

Mexico Water Pump Market Segmentation Analysis

By Pump Type

- Centrifugal Pumps

- Positive Displacement Pump

The most significant market share under pump type is taken by Centrifugal Pumps, which dominate the Mexican water pump market. Centrifugal pumps remain at the forefront for their versatility, dependability, and affordability across a wide range of applications from municipal water supply to industrial use. Their straightforward design, minimal maintenance needs, and capacity for high volumes make them the first choice for the majority of water pumping needs.

The centrifugal pump category continues its dominance via widespread usage in infrastructure developments, farm irrigation networks, and municipal water treatment plants. Growing construction activity in Mexico, with 6.3% annual growth in manufacturing volumes, fuels continuous demand for these pumping solutions. Furthermore, the continuing development of irrigation districts and water infrastructure projects strengthens the market share of centrifugal pumps as the dominant technology for effective management of water through multiple industries.

By End User

- Oil & Gas

- Power

- Residential

- Agriculture & Irrigation

- Commercial Building

- HVAC

- Chemical

- Water & Wastewater

- Food & Beverage

- Others

The most dominant market share under End User is in Water & Wastewater, which captured 20% of the market. This market dominates as a result of Mexico's urgent necessity for water infrastructure development and wastewater treatment growth. The Water & Wastewater segment is fueled by huge government investments, such as USD 3.5 billion disbursed through Mexico's National Infrastructure Fund for water management initiatives.

Power Generation is the most rapidly growing End User segment at a CAGR of 4.83%. The power generation industry, despite accounting for merely 5% of Mexico's total water consumption, generates considerable pump demand for cooling systems for thermal plants. The growth of energy infrastructure in Mexico and demand for effective cooling solutions in fossil fuel-fired power plants generate increasing demand for customized pumping equipment, making it the fastest growing market segment.

Top Companies in Mexico Water Pump Market

The top companies operating in the market include ITT, IDEX, Dover, Flowserve, Sulzer AG, KSB, Xylem, Grundfos, Ebara, SPX Flow, etc., are the top players operating in the Mexico Water Pump Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Mexico Water Pump Market Policies, Regulations, and Standards

4. Mexico Water Pump Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Mexico Water Pump Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Pump Type

5.2.1.1. Centrifugal Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Overhung Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1.1. Vertical Line- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1.2. Horizontal End Suction- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Split Case Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.1. Single/Two Stage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.2. Multi Stage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Vertical Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.1. Turbine- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.2. Axial- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.3. Mixed Flow- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Submersible Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4.1. Solid Handling- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4.2. Non-Solid Handling- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Positive Displacement Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Diaphragm Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Piston Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.3. Gear Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.4. Lobe Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.5. Progressive Cavity Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.6. Screw Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.7. Vane Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.8. Peristaltic Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.9. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By End User

5.2.2.1. Oil & Gas- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Power- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Residential- Market Insights and Forecast 2022-2032, USD Million

5.2.2.4. Agriculture & Irrigation- Market Insights and Forecast 2022-2032, USD Million

5.2.2.5. Commercial Building- Market Insights and Forecast 2022-2032, USD Million

5.2.2.6. HVAC- Market Insights and Forecast 2022-2032, USD Million

5.2.2.7. Chemical- Market Insights and Forecast 2022-2032, USD Million

5.2.2.8. Water & Wastewater- Market Insights and Forecast 2022-2032, USD Million

5.2.2.9. Food & Beverage- Market Insights and Forecast 2022-2032, USD Million

5.2.2.10. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Competitors

5.2.3.1. Competition Characteristics

5.2.3.2. Market Share & Analysis

6. Mexico Centrifugal Pump Water Pump Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By End User- Market Insights and Forecast 2022-2032, USD Million

7. Mexico Positive Displacement Pump Water Pump Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Flowserve

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Sulzer AG

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.KSB

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Xylem

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Grundfos

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.ITT

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.IDEX

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Dover

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Ebara

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. SPX Flow

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Pump Type |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.