Japan Sports Nutrition Market Report: Trends, Growth and Forecast (2026-2032)

Product Type (Sports Protein Products (Protein/Energy Bars, Sports Protein Powder, Sports Protein RTD), Sports Non-Protein Products), Sales Channel (Retail Offline, Retail Online), Ingredients (Vitamins and Minerals, Proteins and Amino Acids, Carbohydrates, Probiotics, Botanicals/Herbals, Others), Functionality (Energy, Muscle growth, Hydration, Weight Management, Others), End User (Bodybuilders, Athletes, Lifestyle Users) ... Read more

|

Major Players

|

Japan Sports Nutrition Market Statistics and Insights, 2026

- Market Size Statistics

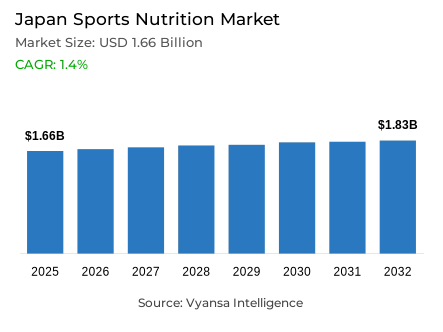

- Sports nutrition in Japan is estimated at USD 1.66 billion.

- The market size is expected to grow to USD 1.83 billion by 2032.

- Market to register a cagr of around 1.4% during 2026-32.

- Product Type Shares

- Sports protein products grabbed market share of 90%.

- Competition

- More than 10 companies are actively engaged in producing sports nutrition in Japan.

- Top 5 companies acquired around 60% of the market share.

- Morinaga & Co Ltd; Ajinomoto Co Inc; Kentai Corp; Meiji Co Ltd; Otsuka Holdings Co Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 60% of the market.

Japan Sports Nutrition Market Outlook

The Japan sports nutrition market is valued at around USD 1.66 billion in 2025 and is projected to reach around USD 1.83 billion by 2032, with a CAGR of around 1.4% during 2026-2032. The growth is supported by rising health awareness and an increase in the number of end users incorporating sports nutrition products into their daily routines. End users are recognizing the benefits of these sports nutrition products in maintaining energy levels, faster recovery, and promoting long term health benefits, which had made these products more trusted and widely used. As a result, the market is gradually shifting from professional athletes to more health conscious end users.

The sports protein products remains the backbone of the segment accounting for around 90% of total sales. Protein powders, ready to mix shakes, and energy bars continue to be popular because they provide quick nutrition and convenience for busy lifestyles. These products helps end users stay active and fit, making this segment the main strength of the market. The demand for convenient protein options, such as portable bars and drinks, will continue to shape future demand.

Retail offline channels continue to dominate, representing around 60% of the total market share. Most of the end users prefer purchasing from retail offline stores, such as pharmacies and supermarkets, where one can see the product details firsthand and get advice from experts before buying. This trust and accessibility make offline sales a key contributor of market growth.

More than ten companies are actively producing sports nutrition products in Japan, with the top five controlling around 60% of the market. Strong competition among these brands is pushing innovation in taste, nutrition, and packaging, helping sustain steady growth and support a wider range of end users across the country.

Japan Sports Nutrition Market Growth DriverSports Protein Powder Leading Market Expansion

The growing interest in personal health and wellness is helping in building end users trust in sports nutrition products. There is a growing awareness among end users about how nutrition helps in energy, recovery, and long term wellbeing. In Japan, as of on September 2024, 29.3% of individuals in the population were aged 65 and older, which suggests a transition from treatment to prevention. This group accounts for over 61% of the country's medical expenditure alone, indicating the importance of proactive nutrition in daily life. Such awareness has helped more and more end users regarding protein based products as a simple means to stay active and healthy.

This better understanding also promotes consistent consumption of sports nutrition. End users become more comfortable with these products and find them safe to add in their diet. Japan's healthcare budget reached 11.5% of GDP in 2023, reflecting the nation's strong focus on long term wellbeing. As education and transparency grow, protein supplements are being trusted as part of daily nutrition, creating a stable base of regular end users that supports sustained market growth.

Japan Sports Nutrition Market ChallengeStrict Rules Slowing Product Launches

Increasing raw material costs and the intensified competition among brands is contributing towards the slowdown in the development of this category. The total medical expenditure of Japan has reached about 43 trillion yen in 2020, revealing the high spending environment in the country that further impacts production and pricing structures. Since 2022, this has contributed to higher product costs and greater competition among branded and private label protein products. A crowded market makes it increasingly difficult for companies to achieve rapid growth while offering affordable options to health conscious end users.

Price awareness among the end users is also shaping market behavior. With general health expenditure still on the rise to reach a projected 8.17% of GDP by 2028, value sensitivity has become a defining attribute in purchase decisions. End users would look for nutrition products at a lower price level, hence slowing down the overall growth of the market. This aspect of affordability is increasingly making it necessary for brands to manage the cost and quality while sustaining trust in sports nutrition products.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Sports Nutrition Market TrendGrowing Shift Towards Plant Based Protein Options

End users are focusing on selecting protein products that can fit into their fast paced lifestyles. With the employment rate among end user aged between 25-34 has reached 87.6%, time limitations have led to strong demand for ready to drink proteins and bars. These product formulations allow end users to maintain nutritional balance, without spending extra time on preparation, demonstrating how health and convenience are becoming closely interconnected in daily routines.

This pattern indicates a constant shift towards the functionality in eating behavior. Many end users, especially young professionals are looking for easy and portable nutrition products that fit into their long working hours and limited leisure time. The government has also reported the decrease in walking activity with respect to the national fitness goals, which further creates the demand for accessible nutrition products for these younger end users. These lifestyle patterns further creates the demand for simple and effective protein formats that fit naturally into the daily routine of busy end users.

Japan Sports Nutrition Market OpportunityInnovation in Convenient, On the Go Nutrition Formats

A strong link between sports nutrition and complete nutrition can be seen emerging throughout the Japan. As of 2024, 93.4% of the population did not meet WHO's healthy diet indicators, which means a huge deficit in balanced nutrition. This situation is encouraging the growth of all in one nutritional products that combine proteins, vitamins, and other key nutrients. Such combinations meet the needs of both fitness focused and health conscious end users who want comprehensive daily nourishment.

In tune with this demographic demand in Japan, where 29.3% of its population is aged 65 and above, and many seek easy yet balanced health solutions, around 30% of those over 75 now need daily support with shopping and meal preparation, creating further demand for ready, nutrient complete options. All these factors combined create clear space for innovation and long term growth in Japan's evolving sports nutrition sector.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Sports Nutrition Market Segmentation Analysis

By Product Type

- Sports Protein Products

- Sports Non-Protein Products

The sports protein products segment accounts for around 90% of the market's total sales. This leading position is maintained through increased adoption by end users, who depend on protein products to keep them fit and healthy. In this category, protein powders and ready to drink products are the most popular forms due to their ease of use and convenience in terms of quick nutrition. Thus, these products are very useful in end users routine for maintaining daily fitness and energy, and therefore this remains the dominant segment in the market.

The segment also draws additional growth from protein and energy bars, which are easy to carry and can fit into busy routines, allowing end users to have appropriate nutrition at any time. Due to their wide use, trusted quality, and availability of many product options, sports protein products represent the key strength of the sports nutrition market.

By Sales Channel

- Retail Offline

- Retail Online

The retail offline sales channel holds the highest share in the market, holding around 60% share of the overall sales. This big share comes from end users who prefer to buy sports nutrition products directly from stores. Physical shops, such as pharmacies, supermarkets, and specialty stores, allow the end user to check the details of the product, compare brands, and seek advice before purchasing. With these benefits, retail offline purchases have become a trusted choice for most end users.

Moreover, retail offline stores provide end users with easy access and confidence in whatever they purchase. The presence of a product and assistance from staff at stores is what gives end users the trust to make repeated purchases. In store promotions and product displays also help in attracting more end users. For these reasons, retail offline continues to serve as the leading sales channel, and it remains the major point through which end users purchase sports nutrition products.

List of Companies Covered in Japan Sports Nutrition Market

The companies listed below are highly influential in the Japan sports nutrition market, with a significant market share and a strong impact on industry developments.

- Morinaga & Co Ltd

- Ajinomoto Co Inc

- Kentai Corp

- Meiji Co Ltd

- Otsuka Holdings Co Ltd

- Asahi Group Foods Ltd

- THG Nutrition Ltd

- DNS Inc

- Morinaga Milk Industry Co Ltd

- Hamada Confect Co Ltd

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Japan Sports Nutrition Market Policies, Regulations, and Standards

4. Japan Sports Nutrition Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Japan Sports Nutrition Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Sports Protein Products- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Protein/Energy Bars- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Sports Protein Powder- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Sports Protein RTD- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Sports Non-Protein Products- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Sales Channel

5.2.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Ingredients

5.2.3.1. Vitamins and Minerals- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Proteins and Amino Acids- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Carbohydrates- Market Insights and Forecast 2022-2032, USD Million

5.2.3.4. Probiotics- Market Insights and Forecast 2022-2032, USD Million

5.2.3.5. Botanicals/Herbals- Market Insights and Forecast 2022-2032, USD Million

5.2.3.6. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Functionality

5.2.4.1. Energy- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Muscle growth- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Hydration- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Weight Management- Market Insights and Forecast 2022-2032, USD Million

5.2.4.5. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By End User

5.2.5.1. Bodybuilders- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Athletes- Market Insights and Forecast 2022-2032, USD Million

5.2.5.3. Lifestyle Users- Market Insights and Forecast 2022-2032, USD Million

5.2.6.By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Japan Protein Products Sports Nutrition Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Ingredients- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Functionality- Market Insights and Forecast 2022-2032, USD Million

6.2.4.By End User- Market Insights and Forecast 2022-2032, USD Million

7. Japan Non-Protein Products Sports Nutrition Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Ingredients- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Functionality- Market Insights and Forecast 2022-2032, USD Million

7.2.4.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Meiji Co Ltd

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Otsuka Holdings Co Ltd

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.Asahi Group Foods Ltd

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.THG Nutrition Ltd

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.DNS Inc

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Morinaga & Co Ltd

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.Ajinomoto Co Inc

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Kentai Corp

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Morinaga Milk Industry Co Ltd

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. Hamada Confect Co Ltd

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Sales Channel |

|

| By Ingredients |

|

| By Functionality |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.