Japan Childrenswear Market Report: Trends, Growth and Forecast (2026-2032)

Product Type (Apparel (Baby and Toddler Wear, Boys Apparel, Girls Apparel), Footwear (Boys Footwear, Girls Footwear), Accessories (Boys Accessories, Girls Accessories), Others), Age Group (Infant/Toddler (Below 2 years), Kids/Children (2 - 14 years)), Price Category (Mass, Premium), Sales Channel (Retail Offline, Retail Online) ... Read more

|

Major Players

|

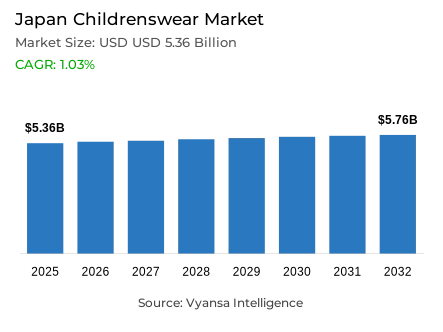

Japan Childrenswear Market Statistics and Insights, 2026

- Market Size Statistics

- Childrenswear in Japan is estimated at USD 5.36 billion in 2025.

- The market size is expected to grow to USD 5.76 billion by 2032.

- Market to register a cagr of around 1.03% during 2026-32.

- Product Type Shares

- Apparel grabbed market share of 80%.

- Competition

- More than 20 companies are actively engaged in producing childrenswear in Japan.

- Top 5 companies acquired around 35% of the market share.

- adidas Japan KK; Louis Vuitton Japan KK; TSI Holdings Co Ltd; Shimamura Co Ltd; Nishimatsuya Chain Co Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 75% of the market.

Japan Childrenswear Market Outlook

Japan childrenswear market is expected to reach around USD 5.36 billion in 2025 and is likely to rise to around USD 5.76 billion in 2032 with a compound annual growth rate of 1.03% during forcast period. Despite the falling birth rate in Japan and the increasing age of its population, it is observed that the market is quite robust, and this is essentially due to the rise in per child spending. End users are seen spending more money on quality, comfortable, and long-lasting clothing, including Japan and foreign brands such as Miki House, Jamie Kay, and William Beta, which focus on quality materials, safety, and excellent design.

The market is dominated by apparel which comprises almost 80% of the total sales and is driven by a long-term demand of functional but fashionable clothes among both boys and girls. Partnerships, including the Birthday x Disney line by Shimamura, and the introduction of Workman Kids demonstrate the increasing popularity of affordable fashion with high functionality. The emphasis on practicality and comfort in childrenswear is also highlighted through innovations in materials, including lightweight and durable fabrics used in children backpacks in Japan.

Retail offline is the most popular segment by sales channel, with approximately 75% of the market, and is backed by the fact that end users prefer to physically evaluate the quality and fit of the fabric. However, online shopping is still on the rise, and websites like ZOZOTOWN and Bebe Mall Official Online Store are promoting online interaction with the help of AI-based suggestions and social networks. This physical-digital model is likely to influence future development.

In the future, the growth of inbound tourism will be instrumental in maintaining market growth. This trend is already being exploited by luxury local brands like Miki House, which are opening airport duty-free stores and launching exclusive collections to travellers. The increased adoption of AI and online communities will also improve the shopping experience, loyalty, and accessibility, which will guarantee the stable, long-term development of the Japan childrenswear market.

Japan Childrenswear Market Growth Driver

Rising Expenditure per Child Driving Market Value Growth

A declining birth rate has not constrained the performance of the Japan childrenswear market, as steady value growth continues to be driven by higher spending per child.. In 2023, the lowest recorded number of live births in Japan was 730,000, according to the Ministry of Health, Labour and Welfare , which is less than half of the 1.5 million births in 1984.

However, families are paying more on fewer children, focusing on quality, comfort and high quality materials. This change can be seen in the increasing popularity of foreign brands like Jamie Kay and William Beta, which focus on organic cotton and sustainable fabrics. The readiness of parents to spend more on high-end, safe, and durable clothing has served to counteract the decrease in volumes, and value growth has become the key factor in the market. With the increase in disposable income per child, the premium and mid-priced segments are likely to continue their growth despite the demographic issues in Japan.

Japan Childrenswear Market Challenge

Declining Birth Rate Restricting Market Sustainability

The Japan Children Wear Market is facing the greatest challange in the form of the continuous reduction in the number of children. In 2023, the Cabinet Office of Japan reported that the total fertility rate in Japan was 1.20, which is significantly lower than the replacement rate of 2.1%. This trend is narrowing the domestic end-user base and is further reinforced by population ageing, with 29.1% of the population aged 65 or above in 2024, according to the World Bank. With a declining number of children born annually, the demand of apparel is increasingly reliant on per-child expenditure and tourism as opposed to organic growth.

The pressure is mounting on independent retailers and domestic brands to maintain sales in the face of intense competition and constrained demand growth. These demographic headwinds are structural threats to long-term market sustainability, forcing brands to be innovative and diversify sales channels to remain relevant.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Childrenswear Market Trend

AI Integration and Digital Engagement Redefining Retail Landscape

The Japan Children Wear Market is being redefined by digitalisation, with brands using AI and online communities to improve their engagement and sales. As an example, Bebe Mall Official Online Store has incorporated Awoo AI, a Japan-based technology platform that examines customer behaviour and product characteristics to create intelligent suggestions and maximise search visibility. According to Awoo AI , this innovation doubled the conversion rates without changing products or prices.

At the same time, major retailers like Hankyu Department Store are establishing online communities where mothers can exchange ideas and create loyalty. Such efforts assist in discovering hidden needs, personalising experiences, and building customer relationships. Combined, AI-based analytics and community interaction is an emerging trend that modernises the Japan children apparel retail ecosystem and improves competitiveness in the digital environment.

Japan Childrenswear Market Opportunity

Inbound Tourism and Global Brand Appeal Fueling Market Expansion

The Japan Children Wear Market has a great growth potential in the recovery of inbound tourism. The Japan National Tourism Organization (JNTO) reported inbound numbers of 25 million in 2024, a significant increase over pandemic lows and nearly pre-COVID levels. This revival is paying off well to high-quality Japan children brands like Miki House. The high-end line of Miki House, the Gold Label, which is made of luxury materials and introduced in 2022, targets high-income travellers, especially Chinese and Southeast Asian ones.

Its first airport duty-free store opened in Kansai International Airport in 2023 further enhanced its visibility among international shoppers. With tourism growth projected to be on the rise, the children wear market is likely to experience increased demand by tourists who are willing to buy high quality Japan-made clothes that reflect quality and exclusivity.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Japan Childrenswear Market Segmentation Analysis

By Product Type

- Apparel

- Footwear

- Accessories

- Others

The segment with the highest share under product type is Apparel, which accounts for nearly 80% of the Japan childrenswear market. Apparel dominates due to the need for frequent wardrobe replacements as children quickly outgrow their clothes. Within this segment, girls’ apparel leads, supported by the popularity of fashion-forward designs, coordinated outfits, and the growing mini-me trend where parents and children dress in similar styles. Boys’ apparel also holds a notable share, benefiting from increased participation in school events, sports, and extracurricular activities that require functional and comfortable clothing.

Moreover, Japan parents tend to value quality, safety, and sustainability in fabrics, driving demand for premium and durable apparel. Brands offering eco-friendly materials, soft textures, and minimalist yet fashionable designs continue to thrive. The rising focus on sustainable production and innovation in kids’ fashion will further strengthen apparel’s dominant position over the forecast period.

By Sales Channel

- Retail Offline

- Retail Online

The segment with the highest share under sales channel is Retail Offline, accounting for nearly 75% of the Japan childrenswear market. Traditional retail remains strong as parents prefer to examine fabric quality, fit, and comfort before purchasing. Department stores, specialty boutiques, and apparel chains continue to attract shoppers, especially during seasonal sales and school-related purchases. Japan end users also trust established retail offlineers for reliability and consistent product standards.

However, reatil online is rapidly expanding as tech-savvy parents increasingly embrace digital shopping for its convenience and variety. retail online platforms and brand websites are enhancing user experience through virtual fitting tools, flexible return policies, and loyalty programs. Over the coming years, a more balanced omnichannel landscape is expected, where online platforms complement physical retail, ensuring accessibility, convenience, and personalized shopping experiences for families across Japan.

List of Companies Covered in Japan Childrenswear Market

The companies listed below are highly influential in the Japan childrenswear market, with a significant market share and a strong impact on industry developments.

- adidas Japan KK

- Louis Vuitton Japan KK

- TSI Holdings Co Ltd

- Shimamura Co Ltd

- Nishimatsuya Chain Co Ltd

- Fast Retailing Co Ltd

- Miki House Co Ltd

- Mizuno Corp

- Goldwin Inc

- Nike Japan Co Ltd

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Japan Childrenswear Market Policies, Regulations, and Standards

4. Japan Childrenswear Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Japan Childrenswear Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in USD Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Product Type

5.2.1.1. Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Baby and Toddler Wear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Boys Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Girls Apparel- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Boys Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Girls Footwear- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Boys Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Girls Accessories- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Age Group

5.2.2.1. Infant/Toddler (Below 2 years)- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Kids/Children (2 - 14 years)- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By Price Category

5.2.3.1. Mass- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Premium- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Sales Channel

5.2.4.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.5.By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. Japan Apparel Childrenswear Market Statistics, 2022-2032

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in USD Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Japan Footwear Childrenswear Market Statistics, 2022-2032

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in USD Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Japan Accessories Childrenswear Market Statistics, 2022-2032

8.1. Market Size & Growth Outlook

8.1.1.By Revenues in USD Million

8.2. Market Segmentation & Growth Outlook

8.2.1.By Age Group- Market Insights and Forecast 2022-2032, USD Million

8.2.2.By Price Category- Market Insights and Forecast 2022-2032, USD Million

8.2.3.By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Competitive Outlook

9.1. Company Profiles

9.1.1.Shimamura Co Ltd

9.1.1.1. Business Description

9.1.1.2. Product Portfolio

9.1.1.3. Collaborations & Alliances

9.1.1.4. Recent Developments

9.1.1.5. Financial Details

9.1.1.6. Others

9.1.2.Nishimatsuya Chain Co Ltd

9.1.2.1. Business Description

9.1.2.2. Product Portfolio

9.1.2.3. Collaborations & Alliances

9.1.2.4. Recent Developments

9.1.2.5. Financial Details

9.1.2.6. Others

9.1.3.Fast Retailing Co Ltd

9.1.3.1. Business Description

9.1.3.2. Product Portfolio

9.1.3.3. Collaborations & Alliances

9.1.3.4. Recent Developments

9.1.3.5. Financial Details

9.1.3.6. Others

9.1.4.Miki House Co Ltd

9.1.4.1. Business Description

9.1.4.2. Product Portfolio

9.1.4.3. Collaborations & Alliances

9.1.4.4. Recent Developments

9.1.4.5. Financial Details

9.1.4.6. Others

9.1.5.Mizuno Corp

9.1.5.1. Business Description

9.1.5.2. Product Portfolio

9.1.5.3. Collaborations & Alliances

9.1.5.4. Recent Developments

9.1.5.5. Financial Details

9.1.5.6. Others

9.1.6.adidas Japan KK

9.1.6.1. Business Description

9.1.6.2. Product Portfolio

9.1.6.3. Collaborations & Alliances

9.1.6.4. Recent Developments

9.1.6.5. Financial Details

9.1.6.6. Others

9.1.7.Louis Vuitton Japan KK

9.1.7.1. Business Description

9.1.7.2. Product Portfolio

9.1.7.3. Collaborations & Alliances

9.1.7.4. Recent Developments

9.1.7.5. Financial Details

9.1.7.6. Others

9.1.8.TSI Holdings Co Ltd

9.1.8.1. Business Description

9.1.8.2. Product Portfolio

9.1.8.3. Collaborations & Alliances

9.1.8.4. Recent Developments

9.1.8.5. Financial Details

9.1.8.6. Others

9.1.9.Goldwin Inc

9.1.9.1. Business Description

9.1.9.2. Product Portfolio

9.1.9.3. Collaborations & Alliances

9.1.9.4. Recent Developments

9.1.9.5. Financial Details

9.1.9.6. Others

9.1.10. Nike Japan Co Ltd

9.1.10.1. Business Description

9.1.10.2. Product Portfolio

9.1.10.3. Collaborations & Alliances

9.1.10.4. Recent Developments

9.1.10.5. Financial Details

9.1.10.6. Others

10. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Price Category |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.