India Water & Wastewater Pump Market Report: Trends, Growth and Forecast (2026-2032)

By Pump Type (Centrifugal Pumps (End Suction, Split Case, Vertical (Turbine, Axial Pump, Mixed Flow Pump), Submersible Pump), Positive Displacement Pumps (Progressing Cavity, Diaphragm, Gear Pump, Others)), By Application (Water, Wastewater), By End User (Industrial Water & Wastewater, Municipal Water & Wastewater) ... Read more

|

Major Players

|

India Water & Wastewater Pump Market Statistics and Insights, 2026

- Market Size Statistics

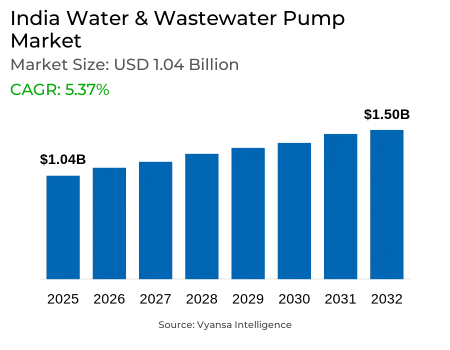

- Water & Wastewater Pump in India is estimated at $ 1.04 Billion.

- The market size is expected to grow to $ 1.5 Billion by 2032.

- Market to register a CAGR of around 5.37% during 2026-32.

- Pump Type Shares

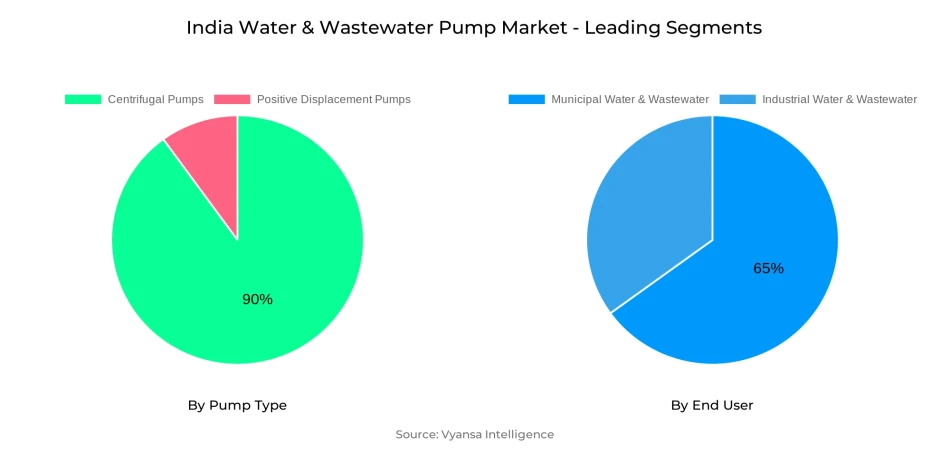

- Centrifugal Pumps grabbed market share of 90%.

- Competition

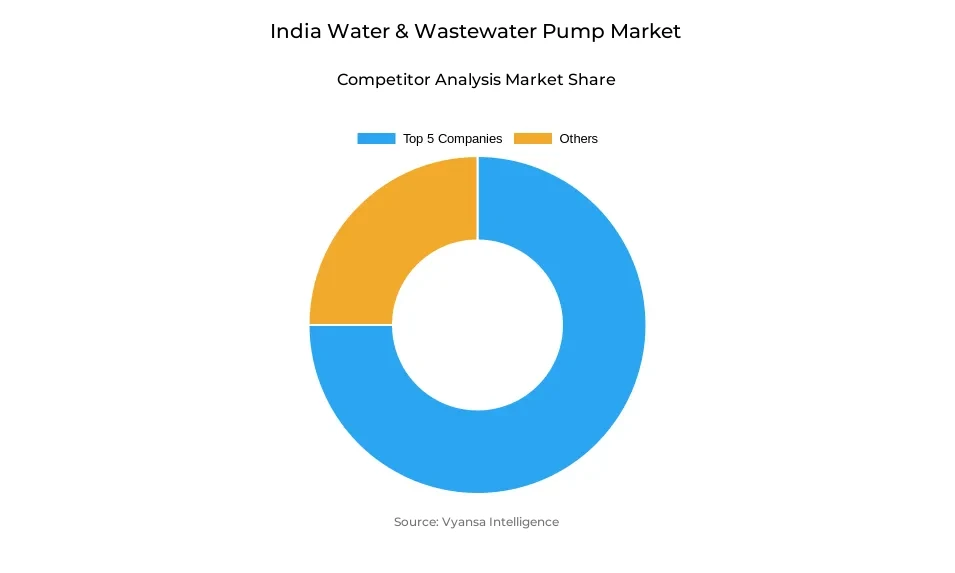

- More than 10 companies are actively engaged in producing Water & Wastewater Pump in India.

- Top 5 companies acquired the maximum share of the market.

- ITT, IDEX, Dover, Flowserve, Sulzer AG etc., are few of the top companies.

- End User

- Municipal Water & Wastewater grabbed 65% of the market.

India Water & Wastewater Pump Market Outlook

India's water and wastewater pump market is also growing robustly on account of increasing sewage flow and the sheer necessity for treatment facilities. India produces 72,368 MLD of municipal wastewater per day, but only 28% gets treated before it is released, making it a huge opportunity. Pumps have a pivotal role in conveying the sewage to treatment plants and maintaining seamless operation during peak flows and monsoon overflows. In terms of value, the market stands at USD 1.04 billion in 2025 and is expected to grow to USD 1.5 billion by 2032.

Government investment in sewage infrastructure and treatment plant upgrades is driving pump installations faster. Collector line expansion and new pumping stations have raised the demand for centrifugal pumps, which currently hold 90% market share for their adaptability and affordability. Suppliers are improving multi-stage and submersible designs to ensure efficiency, making them suitable for changing head and flow conditions in municipal and industrial applications.

Demand from the end-user is mostly focused in municipal applications, which represented 65% of the market in 2025. The segment's leadership is owed to India's widespread urban sanitation networks and big treatment plants dealing with increasing volumes of wastewater. Industrial consumers are on the other hand becoming the most rapidly expanding category, using pumps for onsite effluent recycling and treatment to achieve discharge requirements. The trend is propelling consistent uptake of smart and rugged pumping technologies.

The drive for sustainable infrastructure is also driving digitalization. IoT-based systems, variable-speed drives, and predictive monitoring are assisting operators in reducing energy consumption by as much as 15% and enhancing pump reliability. Moreover, with almost 80% of wastewater considered reusable for industry and irrigation, high-end pumps for distribution of treated water are aiding resource recovery, aligning the demand for pumps with India's overall water security strategy.

India Water & Wastewater Pump Market Growth Driver

Rapid Urban Wastewater Generation Driving Demand for High-Capacity Pumps

The high-flow generation of city wastewater—72,368 MLD daily—necessitates strong pumping solutions since merely 28% of this amount is treated prior to release into lakes and rivers. Such a shortfall emphasizes the importance of dependable, high-capacity pumps for moving sewage to water treatment facilities so that systems are prepared to manage flow overruns during rush hours and monsoons.

Government spending on sewage lines and treatment plant modernizations adds to pump installations. Collector line extension programs and new pumping station construction increase demand for energy-saving centrifugal pumps that provide reliable operation under diversified head and flow applications.

India Water & Wastewater Pump Market Challenge

Limited Treatment Capacity and Strain on Aging Pumping Infrastructure

India's installed capacity for sewage treatment is 31,841 MLD, covering only 44% of urban wastewater produced, with considerable amounts still unprocessed. Land shortages and aging infrastructure hinder the integration of new treatment plants, adding to the burden on existing pump networks.

Recurrent power outages and monsoon inflow events complicate plant operation, producing flow oscillations that degrade pumps and add to maintenance requirements. Operators must contend with the double challenge of maximizing pump reliability while dealing with fluctuating influent loads and strict discharge regulations.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Water & Wastewater Pump Market Trend

Adoption of IoT-Enabled Smart Pumps and Variable-Speed Drives

Operators are increasingly using IoT-capable and variable-speed drives to correlate pump output with actual sewage inflow in real time, cutting energy usage and mechanical wear. Pilot projects in large metros have reported as much as 15% in energy savings through smart controls that adjust pump speed according to actual load conditions.

Digital monitoring platforms make predictive maintenance possible, notifying technicians of vibration or pressure deviation prior to failure. This trend increases uptime and pump longevity, consistent with India's efforts at building sustainable, low-emission infrastructure.

India Water & Wastewater Pump Market Opportunity

Expanding Wastewater Reuse Unlocking Demand for Specialized Pumping Solutions

With 80% of urban wastewater deemed treatable and reusable for non-potable applications—such as irrigation and industrial processes—there is a clear opportunity to turn sewage into a resource. Reusing 8,603 MCM of treated effluent could irrigate over 1.38 Mha of land, yielding 28 million MT of horticultural produce and saving INR 50 million in fertilizer costs.

Distribution pumps for treated water facilitate decentralized reuse strategies and lower freshwater withdrawals while improving water security. Expanding these systems promotes investments in corrosion-resistant pumps that are specialized for nutrient-dense effluent streams.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Water & Wastewater Pump Market Segmentation Analysis

By Pump Type

- Centrifugal Pumps

- Positive Displacement Pumps

The most market-leading segment under Pump Type is Centrifugal Pumps, which are ruling the roost with a simple structure, minimal maintenance, and high-volume flow capability. Centrifugal pumps captured 90% of the market in 2024, led by use in water supply, irrigation, and wastewater treatment applications.

Manufacturers concentrate on multi-stage and submersible centrifugal pumps to address varied head demands. Improvements in impeller design as well as materials contribute to increased efficiency and longevity, positioning centrifugal pumps as the go-to option for most municipal and industrial applications.

By End User

- Industrial Water & Wastewater

- Municipal Water & Wastewater

The most high-market-share segment under End User is Municipal Water & Wastewater, which indicates widespread urban sanitation networks and big-scale treatment plants. The dominance of this segment is due to the fact that treating increasing volumes of sewerage in urban areas and adhering to environment regulations are necessary.

Industrial Water & Wastewater is the fastest-growing end-use segment, with factories and processing units investing in specific effluent treatment and recycling. Use of pumps for on-site treatment enables industries to save on freshwater intake and comply with discharge norms, leading to a growth rate of 7.79% in this segment.

Top Companies in India Water & Wastewater Pump Market

The top companies operating in the market include ITT, IDEX, Dover, Flowserve, Sulzer AG, KSB, Xylem, Grundfos, Ebara, SPX Flow, etc., are the top players operating in the India Water & Wastewater Pump Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. India Water & Wastewater Pump Market Policies, Regulations, and Standards

4. India Water & Wastewater Pump Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. India Water & Wastewater Pump Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Pump Type

5.2.1.1. Centrifugal Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. End Suction- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Split Case- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Vertical- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.1. Turbine- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.2. Axial Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3.3. Mixed Flow Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.4. Submersible Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Positive Displacement Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Progressing Cavity- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Diaphragm- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.3. Gear Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Application

5.2.2.1. Water- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Wastewater- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By End User

5.2.3.1. Industrial Water & Wastewater- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Municipal Water & Wastewater- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. India Centrifugal Water & Wastewater Pump Market Statistics, 2020-2030F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

7. India Positive Displacement Water & Wastewater Pump Market Statistics, 2020-2030F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Application- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By End User- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Flowserve Corporation

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Ebara Corporation

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.WILO SE

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Sulzer Limited

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.Grundfos Holding A/S

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.Xylem Inc.

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.KSB SE & Co. KGaA

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.Kirloskar Brothers Limited (KBL)

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Franklin Electric

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. Pentair PLC

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Pump Type |

|

| By Application |

|

| By End User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.