India Software-Defined Vehicle Platforms Market Report: Trends, Growth and Forecast (2026-2032)

By Component (Software, Services), By Software Application Domain (ADAS & Autonomous Driving Software, Infotainment & Digital Cockpit Software, Powertrain Control Software, Chassis & Vehicle Dynamics Software, Body & Comfort Software, Cross-Vehicle Enablers (Platform Infrastructure) (Vehicle OS & Middleware, OTA Update Management, Cybersecurity, DevOps & Toolchains)), By Deployment Mode (On-Board (Embedded), Cloud-Based, Hybrid (On-Board + Cloud)), By End-User (Automotive OEMs, Tier-1 Suppliers, Fleet Operators & Mobility Service Providers), By Vehicle Type (Passenger Vehicles, Commercial Vehicles), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Software-Defined Vehicle Platforms Market Statistics and Insights, 2026

- Market Size Statistics

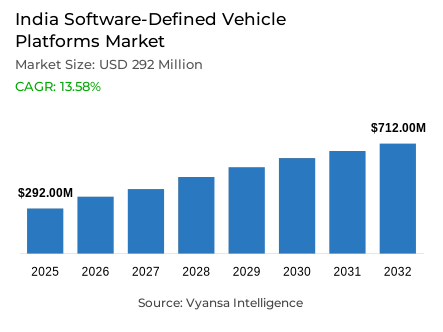

- Software-defined vehicle platforms market size in India was valued at USD 292 million in 2025 and is estimated at USD 332 million in 2026.

- The market size is expected to grow to USD 712 million by 2032.

- Market to register a CAGR of around 13.58% during 2026-32.

- Software Application Domain Shares

- Adas & autonomous driving software grabbed market share of 40%.

- Competition

- Software-defined vehicle platforms in India is currently being catered to by more than 10 companies.

- Top 5 companies acquired around 20% of the market share in 2026.

- Bosch Limited, HARMAN INTERNATIONAL (INDIA) PRIVATE LIMITED, Mahindra & Mahindra Limited, Qualcomm Technologies Inc. (Snapdragon® Digital Chassis™), Mobileye Global Inc. (Mobileye EyeQ™ System-on-Chip) etc., are few of the top companies.

- Deployment Mode

- On-board (embedded) grabbed 60% of the market.

India Software-Defined Vehicle Platforms Market Outlook

Automotive platforms are moving from distributed electronic-control architecture toward software-led vehicle design, where operating systems, middleware, ADAS software, digital cockpit software, OTA update management, cybersecurity, and cloud integration determine vehicle differentiation. India software-defined vehicle (SDV) platforms market covers the software stack and engineering layer used by OEMs, Tier-1 suppliers, mobility operators, and vendors. India software-defined vehicle (SDV) platforms market was valued at USD 292 million in 2025 and is projected to reach USD 332 million in 2026 and USD 712 million by 2032, registering a CAGR of 13.58% during 2026-2032.

Electrification, connected mobility, digital cockpits, and ADAS readiness are strengthening demand for software-defined vehicle platforms in India. The PM E-DRIVE scheme supports battery EVs, charging infrastructure, testing-agency upgrades, e-buses, e-trucks, e-ambulances, and demand incentives, creating a policy channel for software-rich electric mobility deployment. This widens the addressable base for vehicle operating system India, connected vehicle software India, OTA vehicle software updates, and automotive cybersecurity platforms across OEM programs.

Industrial impact is visible in procurement models as suppliers shift from hardware-only modules to integrated software, semiconductor, cloud, and engineering packages. SIAM reported that passenger vehicles posted their highest-ever FY2024-25 sales of 4.3 million units, while utility vehicles contributed 65% of total PV sales, strengthening the volume base for feature-rich platforms. India software-defined vehicle (SDV) platforms industry gains from this shift as SUVs and EVs absorb more ADAS, infotainment, telematics, and centralized E/E architecture content per vehicle.

Supplier positioning is moving toward production-ready domain architectures, cockpit compute, vehicle data platforms, and embedded-cloud toolchains. India software-defined vehicle (SDV) platforms market benefits as OEMs localize platform engineering, while global technology vendors deepen India-specific collaborations. India software-defined vehicle (SDV) platforms industry is entering 2026 with stronger demand visibility, rising platform modularity, and higher competitive intensity across embedded software, silicon, middleware, and automotive cloud layers.

India Software-Defined Vehicle Platforms Market Growth Driver

Platform Consolidation Accelerates OEM Demand

Connected EV programs and premium SUV demand are accelerating platform-level procurement as OEMs seek software reuse across ADAS, infotainment, powertrain, and telematics domains. India software-defined vehicle (SDV) platforms market benefits from this shift because common software stacks lower integration duplication and help automakers convert hardware platforms into upgradeable digital products. India software-defined vehicle (SDV) platforms industry also gains from stronger demand for automotive middleware, OTA workflows, and centralized vehicle computing. This strengthens supplier qualification and platform-roadmap visibility for 2026 programs.

SIAM analysis of the Vahan database shows that total EV registrations reached 1.97 million units in FY2024-25, up from 1.68 million units in FY2023-24, while electric passenger vehicle registrations crossed 1 lakh units. This expanding EV installed base improves demand capture for software-defined electric vehicles, battery management software, connected cockpit software, and secure update infrastructure, particularly among OEMs building multi-model EV portfolios with shared digital architectures and scalable lifecycle management.

India Software-Defined Vehicle Platforms Market Challenge

Software Complexity Pressures Launch Timelines

Software integration complexity is constraining deployment timelines as OEMs migrate from distributed ECU models to centralized, service-oriented architectures. India software-defined vehicle (SDV) platforms market faces execution risk where legacy platforms, safety validation, cybersecurity assurance, and supplier toolchain fragmentation increase engineering workload. India software-defined vehicle (SDV) platforms industry must therefore balance feature velocity with functional safety, version control, diagnostics, and regulatory-grade traceability across vehicle programs.

Microsoft states that SDVs require a new approach to vehicle software and hardware architecture, and identifies software integration complexity, higher development expenses, and delayed start-of-production timelines as industry challenges. This bottleneck raises platform qualification costs, slows software release cadence, and limits adoption by OEMs that lack mature DevOps for automotive software, AUTOSAR Adaptive capability, and cross-domain testing environments for embedded SDV platforms. It also raises dependency on specialized validation partners, secure software bill of materials processes, and reusable reference architectures for program-scale delivery within compressed timelines.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Software-Defined Vehicle Platforms Market Trend

Middleware Standardization Reframes Vehicle Architecture

AUTOSAR Adaptive, Android Automotive, and service-oriented middleware are becoming practical deployment tools rather than concept-layer architecture choices. India software-defined vehicle (SDV) platforms market is shifting toward reusable software layers that support app ecosystems, domain controllers, and OTA-enabled feature expansion. India software-defined vehicle (SDV) platforms industry benefits as middleware suppliers convert engineering complexity into scalable integration modules for OEM launch programs.

Vector reported that Mahindra’s Electric Origin Platform integrates MICROSAR Adaptive with Android Automotive and offers more than 50 apps at launch through a fully interconnected vehicle architecture. This development strengthens platform standardization, validates SDV platform trends in Indian automotive industry, and improves competitive positioning for vendors supplying automotive middleware platform, vehicle abstraction layer, DevOps for automotive software, and software lifecycle management across production-intent electric SUVs. It also raises demand for automotive operating system India expertise and secure OTA update governance across suppliers, supporting faster cross-vehicle software reuse and launch discipline.

India Software-Defined Vehicle Platforms Market Opportunity

Connected Lifecycle Services Expand Supplier Upside

Connected-vehicle lifecycle services create supplier upside beyond initial vehicle production because OEMs need persistent connectivity, secure diagnostics, telemetry, subscription enablement, and remote software governance after sale. India software-defined vehicle (SDV) platforms market can capture this layer through cloud connectivity, fleet data intelligence, OTA software deployment, vehicle data analytics India, and managed automotive cybersecurity services that extend platform value across operating years.

Tata Communications stated that its MOVE platform will support JLR’s next-generation software-defined vehicles with continuous connectivity and intelligent services across 120 countries. This supplier-led connectivity model opens market access for Indian platform operators serving global OEM programs from India-based delivery centers. It also strengthens localization potential for connected vehicle platform opportunities in India, especially where mobility service providers, commercial fleets, and premium EV makers require cross-border connectivity management and secure vehicle data orchestration. This expands demand capture for platform integrators linking embedded software with cloud-native mobility operations at scale.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Software-Defined Vehicle Platforms Market Segmentation Analysis

By Software Application Domain

- ADAS & Autonomous Driving Software

- Infotainment & Digital Cockpit Software

- Powertrain Control Software

- Chassis & Vehicle Dynamics Software

- Body & Comfort Software

- Cross-Vehicle Enablers (Platform Infrastructure)

- Vehicle OS & Middleware

- OTA Update Management

- Cybersecurity

- DevOps & Toolchains

ADAS and autonomous driving software lead software application domain with 40% share because safety automation is becoming a core differentiator in premium EVs, SUVs, and feature-rich passenger vehicles. India software-defined vehicle (SDV) platforms market sees ADAS software absorbing higher platform value through perception, sensor fusion, driver monitoring, embedded compute, validation, and safety software integration. India software-defined vehicle (SDV) platforms industry gains pricing support as ADAS content requires tightly coupled hardware-software stacks.

Mahindra’s BE 6 and XEV 9e specification lists ADAS L2+ with Mobileye EyeQ6, an 8 MP camera, 51 TOPS, 220k DMIPS, and a next-generation domain architecture with Ethernet backbone. This production-linked deployment supports ADAS software platform India demand by proving that autonomous driving middleware, crash avoidance software, adaptive cruise control software, and connected cockpit functions are moving into Indian OEM platforms rather than remaining imported feature bundles. It sharpens supplier selection around safety validation and update continuity across models.

By Deployment Mode

- On-Board (Embedded)

- Cloud-Based

- Hybrid (On-Board + Cloud)

On-board embedded deployment holds 60% share because safety-critical and latency-sensitive functions still require deterministic vehicle-side execution. India software-defined vehicle (SDV) platforms market remains anchored in embedded compute for ADAS, cockpit rendering, powertrain control, chassis functions, body control, secure gateways, and diagnostic routines. Cloud-based SDV platforms are growing, yet embedded SDV platforms retain control-critical relevance where connectivity loss cannot interrupt vehicle operation.

Qualcomm reported that Mahindra’s BE 6 and XEV 9e represent the first Indian deployment of the next-generation Snapdragon Cockpit Platform and Snapdragon Auto 5G Modem-RF solution. This strengthens on-board platform adoption by combining cockpit compute, in-vehicle AI, 5G connectivity, and real-time OTA readiness within the vehicle. It also improves supplier positioning for semiconductor, software stack virtualization, domain controller software, and cloud-connected vehicles that depend on resilient embedded execution. For OEM sourcing, this preserves demand for validated in-vehicle platforms with upgradeable software and long lifecycle support across model generations securely.

List of Companies Covered in India Software-Defined Vehicle Platforms Market

The companies listed below are highly influential in the India software-defined vehicle platforms market, with a significant market share and a strong impact on industry developments.

- Bosch Limited

- HARMAN INTERNATIONAL (INDIA) PRIVATE LIMITED

- Mahindra & Mahindra Limited

- Qualcomm Technologies Inc. (Snapdragon® Digital Chassis™)

- Mobileye Global Inc. (Mobileye EyeQ™ System-on-Chip)

- KPIT Technologies Limited

- Vector Informatik India Pvt. Ltd.

- Tata Elxsi Limited

- Tata Passenger Electric Mobility Limited

- Microsoft Corporation India (Pvt) Ltd (Microsoft Azure)

Market News & Updates

- Tata Elxsi Limited, 2026:

Tata Elxsi launched DevStudio.ai, a multi-agent, ASPICE-aligned GenAI platform for automotive software engineering. The platform supports requirements, architecture, coding, testing, qualification, and traceability across the software development lifecycle. The update supports Indian SDV development across body, chassis, infotainment, and software-defined vehicle architectures.

- Tata Elxsi Limited, 2026:

Tata Elxsi and JSW Motors established the JNEXT Technology Center in Pune to support connected and software-defined mobility programs in India. Tata Elxsi will implement the connected vehicle platform and unified customer experience app for JSW Motors’ upcoming vehicles. The update supports local SDV engineering, cloud platforms, OTA frameworks, and connected mobility services.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Software-Defined Vehicle (SDV) Platforms Market Policies, Regulations, and Standards

- India Software-Defined Vehicle (SDV) Platforms Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Software-Defined Vehicle (SDV) Platforms Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Component

- Software- Market Insights and Forecast 2022-2032, USD Million

- Services- Market Insights and Forecast 2022-2032, USD Million

- By Software Application Domain

- ADAS & Autonomous Driving Software- Market Insights and Forecast 2022-2032, USD Million

- Infotainment & Digital Cockpit Software- Market Insights and Forecast 2022-2032, USD Million

- Powertrain Control Software- Market Insights and Forecast 2022-2032, USD Million

- Chassis & Vehicle Dynamics Software- Market Insights and Forecast 2022-2032, USD Million

- Body & Comfort Software- Market Insights and Forecast 2022-2032, USD Million

- Cross-Vehicle Enablers (Platform Infrastructure)- Market Insights and Forecast 2022-2032, USD Million

- Vehicle OS & Middleware- Market Insights and Forecast 2022-2032, USD Million

- OTA Update Management- Market Insights and Forecast 2022-2032, USD Million

- Cybersecurity- Market Insights and Forecast 2022-2032, USD Million

- DevOps & Toolchains- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode

- On-Board (Embedded)- Market Insights and Forecast 2022-2032, USD Million

- Cloud-Based- Market Insights and Forecast 2022-2032, USD Million

- Hybrid (On-Board + Cloud)- Market Insights and Forecast 2022-2032, USD Million

- By End-User

- Automotive OEMs- Market Insights and Forecast 2022-2032, USD Million

- Tier-1 Suppliers- Market Insights and Forecast 2022-2032, USD Million

- Fleet Operators & Mobility Service Providers- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type

- Passenger Vehicles- Market Insights and Forecast 2022-2032, USD Million

- Commercial Vehicles- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North- Market Insights and Forecast 2022-2032, USD Million

- East- Market Insights and Forecast 2022-2032, USD Million

- West- Market Insights and Forecast 2022-2032, USD Million

- South- Market Insights and Forecast 2022-2032, USD Million

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Component

- Market Size & Growth Outlook

- India ADAS & Autonomous Driving Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Infotainment & Digital Cockpit Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Powertrain Control Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Chassis & Vehicle Dynamics Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Body & Comfort Software Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Cross-Vehicle Enablers (Platform Infrastructure) Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Software Application Domain- Market Insights and Forecast 2022-2032, USD Million

- By Deployment Mode- Market Insights and Forecast 2022-2032, USD Million

- By End-User- Market Insights and Forecast 2022-2032, USD Million

- By Vehicle Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Semiconductor & Computing Platform Providers

- Qualcomm Technologies Inc. (Snapdragon® Digital Chassis™)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mobileye Global Inc. (Mobileye EyeQ™ System-on-Chip)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Qualcomm Technologies Inc. (Snapdragon® Digital Chassis™)

- Vehicle OS, Middleware & Enabler Platform Providers

- KPIT Technologies Limited

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vector Informatik India Pvt. Ltd.

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tata Elxsi Limited

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- KPIT Technologies Limited

- Tier-1 Suppliers with SDV Platform Capabilities

- Bosch Limited

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HARMAN INTERNATIONAL (INDIA) PRIVATE LIMITED

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bosch Limited

- OEMs with Proprietary SDV Platforms

- Mahindra & Mahindra Limited

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tata Passenger Electric Mobility Limited

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mahindra & Mahindra Limited

- Cloud & Technology Platform Providers

- Microsoft Corporation India (Pvt) Ltd (Microsoft Azure)

- Business Description

- Service Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Microsoft Corporation India (Pvt) Ltd (Microsoft Azure)

- Semiconductor & Computing Platform Providers

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Component |

|

| By Software Application Domain |

|

| By Deployment Mode |

|

| By End-User |

|

| By Vehicle Type |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.