India Digestive Remedies Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Paediatric Digestive Remedies (Paediatric Diarrhoeal Remedies, Paediatric Indigestion & Heartburn Remedies, Paediatric Laxatives, Paediatric Motion Sickness Remedies), Diarrhoeal Remedies, IBS Treatments, Indigestion & Heartburn Remedies (Antacids, Antiflatulents, Digestive Enzymes, H2 Blockers, Proton Pump Inhibitors), Laxatives, Motion Sickness Remedies), By Age Group (Children & Adolescents (01-17 years), Adults (18-65 years), Geriatric (65+ years)), By Sales Channel (Retail Online, Retail Offline (Hospitals, Clinics, Pharmacies)), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Digestive Remedies Market Statistics and Insights, 2026

- Market Size Statistics

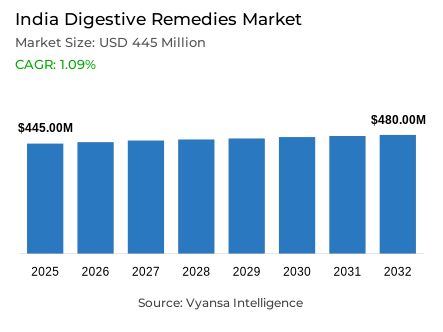

- Digestive remedies market size in India was valued at USD 445 million in 2025 and is estimated at USD 450 Million in 2026.

- The market size is expected to grow to USD 480 million by 2032.

- Market to register a CAGR of around 1.09% during 2026-32.

- Product Type Shares

- Indigestion & heartburn remedies grabbed market share of 75%.

- Competition

- More than 10 companies are actively engaged in producing digestive remedies in India.

- Top 5 companies acquired around 75% of the market share.

- TTK Healthcare Ltd, Piramal Enterprises Ltd, Cadila Healthcare Ltd, GSK Consumer Healthcare, Dabur India Ltd etc., are few of the top companies.

- Sales Channel

- Retail offline grabbed 90% of the market.

India Digestive Remedies Market Outlook

The India digestive remedies market size was valued at USD 445 million in 2025 and is projected to grow from USD 450 million in 2026 to USD 480 million by 2032, exhibiting a CAGR of around 1.09% during the forecast period. Growth is supported by climate-related health stress and lifestyle patterns that keep digestive discomfort common across the country. The India Meteorological Department reports that 2024 is the warmest year recorded in India since 1901, with the annual mean land surface air temperature 0.65°C above the long-term average and 459 heat-wave-related deaths recorded during the year.

Extreme summer conditions and dehydration episodes continue to increase demand for digestive remedies across both urban and rural areas. Heat exposure often leads to stomach upset and diarrhoeal illness, which supports the regular use of oral rehydration salts and quick-relief products. Within product categories, indigestion and heartburn remedies account for about 75% of the category, reflecting the widespread occurrence of acidity, gas, and heartburn linked to irregular meals, outside food consumption, and busy daily routines.

At the same time, preventive wellness and traditional health practices are shaping consumer behaviour. The Government of India reports that the Ayush Research Portal hosts more than 43,000 studies as of February 2025, highlighting the growing role of holistic healthcare and lifestyle-based health management. Improving dietary awareness also influences purchasing patterns, as MoSPI data shows calorie intake among the lowest-income groups rising to 1,688 Kcal in rural India and 1,696 Kcal in urban India in 2023-24, encouraging some consumers to try diet correction and preventive care before using digestive remedies.

Distribution remains heavily dependent on traditional retail channels. Retail offline accounts for about 90% of sales, as consumers often purchase digestive treatments for immediate relief from symptoms such as acidity, diarrhoea, and bloating. However, digital access is expanding rapidly, with 86.3% of households having internet access and 85.5% owning a smartphone, while 24.5% of households make online purchases according to the 2025 telecom survey. This growing connectivity is gradually increasing digital visibility and repeat purchase opportunities for digestive remedies.

India Digestive Remedies Market Growth DriverExtreme Summer Conditions Keep Rapid Relief in Demand

India’s digestive remedies market gets a strong push from extreme summer conditions and dehydration-linked health episodes. The India Meteorological Department states that 2024 is the warmest year recorded in India since 1901, with the annual mean land surface air temperature standing 0.65°C above the long-term average. The same report records 459 heat-wave-related deaths in 2024 and shows heatwave conditions spreading across east, north, and central India during key summer months.

This climate stress directly supports demand for diarrhoeal remedies, especially oral rehydration salts and fast-relief hydration products. In India, these products fit both urban and rural need because consumers look for quick support during heat exposure, dehydration, and stomach upset. As a result, summer weather remains a clear demand driver for digestive remedies rather than a short-lived seasonal spike.

India Digestive Remedies Market ChallengePreventive Self-Care Reduces Dependence on Quick-Fix OTCs

The challenge with digestive remedies in India is the increasing popularity of preventive wellness and traditional self-care. In fact, as per the Government of India website in February 2025, the Ayush Research Portal has over 43,000 studies. The Prime Minister’s review of the sector also emphasizes preventive healthcare and holistic/integrated health. This increases the credibility of non-allopathic wellness options for the consumer to take care of their digestive well-being.

At the same time, MoSPI’s 2025 nutrition release shows calorie intake among the bottom 5% improves to 1,688 Kcal in rural India and 1,696 Kcal in urban India in 2023-24, up from 1,607 and 1,623 Kcal in 2022-23. As diet awareness and everyday health management improve, some consumers try food correction and traditional options before standard OTC remedies, which creates a restraint for routine antacid and antiflatulent use.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Digestive Remedies Market TrendConvenience-Led Formats Move Closer to the Consumer

A clear trend in India is the move towards convenient, portable, and digitally discoverable digestive care. The Ministry of Statistics and Programme Implementation (MoSPI) has released a report, published by the MoSPI Communications and Multimedia Statistics Division (CMS), which indicates that 86.3% of Indian households have internet access at home, 85.5% of households own at least one smartphone and 24.5% of households made an online purchase of goods within 30 days prior to the date of the survey. These three statistics illustrate how connected consumers are, how much they compare products before making a purchase and how confident they feel purchasing everyday items through digital channels.

The growing availability of sachets, chewable remedies, ready-to-drink liquids and other easy formats that fit into busy lifestyles will aid the development of the market for digestive remedy-related products. The trend is not only about making products more accessible; it is also about using packaging that makes relief (acidity, bloating or indigestion) easier to carry; completing product information faster and enabling easier access to products at any time (e.g., at the moment of relieving symptoms of acidity, bloating or indigestion).

India Digestive Remedies Market OpportunityDigital Commerce Opens Wider Reach for Everyday Relief Brands

A major opportunity in India lies in expanding digestive remedies through digital commerce and wider online access. The Government of India states that ONDC already spreads across 616+ cities and has more than 7.64 lakh sellers and service providers as of January 2025. MoSPI also reports that 24.5% of households make online purchases of goods in the 30 days before the 2025 telecom survey. Together, these figures show a broader digital route-to-market for everyday OTC categories.

This matters for digestive remedies because many purchases are immediate, repeat-led, and convenience-driven. Brands that combine trusted relief with easy online visibility, small packs, and rapid replenishment can reach more consumers beyond traditional urban chemist networks. In a category built on urgency and repeat need, stronger digital reach creates a practical expansion opportunity across both established and emerging consumption centres.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Digestive Remedies Market Segmentation Analysis

By Product Type

- Paediatric Digestive Remedies

- Paediatric Diarrhoeal Remedies

- Paediatric Indigestion & Heartburn Remedies

- Paediatric Laxatives

- Paediatric Motion Sickness Remedies

- Diarrhoeal Remedies

- IBS Treatments

- Indigestion & Heartburn Remedies

- Antacids

- Antiflatulents

- Digestive Enzymes

- H2 Blockers

- Proton Pump Inhibitors

- Laxatives

- Motion Sickness Remedies

The segment has the highest share around product type under indigestion & heartburn remedies, with about 75% market share. This segment stays ahead because acidity, gas, and heartburn are common everyday complaints in India, especially among consumers dealing with irregular meals, outside food, and busy work routines. The strong presence of trusted brands, easy OTC familiarity, and multiple convenient formats also keep this category widely accepted across age groups.

The segment also benefits from India’s convenience-led buying pattern. MoSPI’s CMS: Telecom 2025 shows that 24.5% of households make online purchases of goods in the 30 days before the survey, while 86.3% of households have internet access within household premises. This supports better visibility and faster repeat purchase of quick-relief products, which helps indigestion & heartburn remedies remain the leading product type.

By Sales Channel

- Retail Online

- Retail Offline

- Hospitals

- Clinics

- Pharmacies

The segment has the highest share around sales channel under retail offline, with about 90% of the market. This channel leads because digestive remedies are often bought for immediate relief, and consumers still value the speed, trust, and pharmacist guidance available through chemists, pharmacies, and nearby stores. For acidity, diarrhoea, and bloating, instant availability matters more than delayed delivery in many purchase situations.

Even so, online access is growing. MoSPI’s CMS: Telecom 2025 shows that 24.5% of households make online purchases of goods in the 30 days before the survey. That signals rising digital comfort, but not enough to displace store-based buying in a symptom-led category. As a result, Retail Offline continues to dominate because it combines urgent access, familiarity, and stronger purchase confidence.

List of Companies Covered in India Digestive Remedies Market

The companies listed below are highly influential in the India digestive remedies market, with a significant market share and a strong impact on industry developments.

- TTK Healthcare Ltd

- Piramal Enterprises Ltd

- Cadila Healthcare Ltd

- GSK Consumer Healthcare

- Dabur India Ltd

- Abbott India Ltd

- Cipla Ltd

- Pfizer Ltd

- Himalaya Drug Co The

- Wallace Pharmaceuticals Pvt Ltd

Competitive Landscape

In 2025, the competitive landscape of digestive remedies in India remained led by GSK Consumer Healthcare, which holds a 43.4% retail value share, followed by Dabur India Ltd with 18.7%. GSK maintains its strong leadership primarily through its flagship brand Eno, a widely trusted household remedy for acidity and indigestion that benefits from strong brand recognition, continuous product innovation and an extensive distribution network across both urban and rural markets. The brand has also strengthened its accessibility through quick commerce platforms such as Zepto, Swiggy Instamart and Blinkit, supporting its dominance in the category. Meanwhile, Dabur India Ltd holds a notable position due to its strong portfolio of herbal and traditional digestive solutions, which align with the growing consumer preference for natural remedies. Overall demand for digestive remedies continues to be supported by rising heatwave conditions increasing the use of oral rehydration salts, as well as sedentary lifestyles, unhealthy diets and hectic work schedules that contribute to digestive discomfort. However, the category also faces competition from traditional home remedies such as ajwain, ginger and cumin, alongside increasing consumer interest in probiotics and holistic wellness solutions aimed at improving long-term gut health.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Digestive Remedies Market Policies, Regulations, and Standards

- India Digestive Remedies Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Digestive Remedies Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product Type

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Diarrhoeal Remedies- Market Insights and Forecast 2022-2032, USD Million

- IBS Treatments- Market Insights and Forecast 2022-2032, USD Million

- Indigestion & Heartburn Remedies- Market Insights and Forecast 2022-2032, USD Million

- Antacids- Market Insights and Forecast 2022-2032, USD Million

- Antiflatulents- Market Insights and Forecast 2022-2032, USD Million

- Digestive Enzymes- Market Insights and Forecast 2022-2032, USD Million

- H2 Blockers- Market Insights and Forecast 2022-2032, USD Million

- Proton Pump Inhibitors- Market Insights and Forecast 2022-2032, USD Million

- Laxatives- Market Insights and Forecast 2022-2032, USD Million

- Motion Sickness Remedies- Market Insights and Forecast 2022-2032, USD Million

- Paediatric Digestive Remedies- Market Insights and Forecast 2022-2032, USD Million

- By Age Group

- Children & Adolescents (01-17 years)- Market Insights and Forecast 2022-2032, USD Million

- Adults (18-65 years)- Market Insights and Forecast 2022-2032, USD Million

- Geriatric (65+ years)- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel

- Retail Online- Market Insights and Forecast 2022-2032, USD Million

- Retail Offline- Market Insights and Forecast 2022-2032, USD Million

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Clinics- Market Insights and Forecast 2022-2032, USD Million

- Pharmacies- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Growth Outlook

- India Paediatric Digestive Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Diarrhoeal Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India IBS Treatments Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Indigestion & Heartburn Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Laxatives Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Motion Sickness Remedies Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Age Group- Market Insights and Forecast 2022-2032, USD Million

- By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- GSK Consumer Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dabur India Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Abbott India Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cipla Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pfizer Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TTK Healthcare Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Piramal Enterprises Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cadila Healthcare Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Himalaya Drug Co The

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Wallace Pharmaceuticals Pvt Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GSK Consumer Healthcare

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Age Group |

|

| By Sales Channel |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.