India Cardiac Biomarkers Diagnostics Market Report: Trends, Growth and Forecast (2026-2032)

By Product (Reagents & Kits, Instruments/Analyzers, Consumables & Accessories), By Biomarker Type (Troponin (Cardiac Troponin I (cTnI), Cardiac Troponin T (cTnT), High-Sensitivity Troponin (hs-cTn)), Creatine Kinase-MB (CK-MB), Myoglobin, BNP and NT-proBNP, Other Cardiac Biomarkers), By Application (Acute Coronary Syndrome (ACS), Myocardial Infarction (MI), Congestive Heart Failure (CHF), Chest Pain/Emergency Triage, Risk Stratification & Prognosis, Other Cardiac Conditions), By Testing Location (Laboratory Testing, Point-of-Care Testing (POCT)), By End User (Hospitals, Diagnostic Laboratories, Emergency Departments, Cardiac/Specialty Clinics, Ambulatory Care Centers, Others), By Technology (Chemiluminescence Immunoassay, Fluorescence Immunoassay, ELISA, Lateral Flow/Rapid Immunoassay, Other Assay Technologies), By Sample Type (Whole Blood, Plasma, Serum), By Region (North, East, West, South) ... Read more

|

Major Players

|

India Cardiac Biomarkers Diagnostics Market Statistics and Insights, 2026

- Market Size Statistics

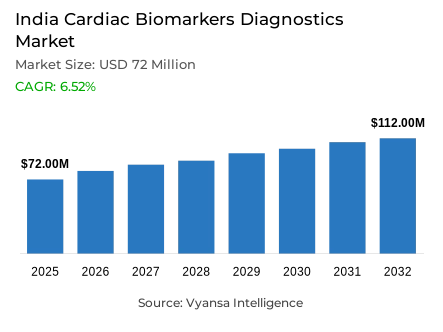

- Cardiac biomarkers diagnostics market size in India was valued at USD 72 million in 2025 and is estimated at USD 78 million in 2026.

- The market size is expected to grow to USD 112 million by 2032.

- Market to register a CAGR of around 6.52% during 2026-32.

- Product Shares

- Reagents & kits grabbed market share of 55%.

- Competition

- More than 10 companies are actively engaged in producing cardiac biomarkers diagnostics in India.

- Top 5 companies acquired around 60% of the market share.

- BioMérieux, Thermo Fisher Scientific, Ortho Clinical Diagnostics, Roche Diagnostics, Abbott Laboratories etc., are few of the top companies.

- Biomarker Type

- Troponin grabbed 55% of the market.

India Cardiac Biomarkers Diagnostics Market Outlook

The India cardiac biomarkers diagnostics market was valued at USD 72 million in 2025, establishing a commercially purposeful and structurally supported foundation within one of South Asia's most rapidly evolving clinical diagnostics ecosystems. Projected to advance from USD 78 million in 2026 to USD 112 million by 2032, the sector registers a compound annual growth rate of 6.52% across the forecast horizon a steady and well supported expansion trajectory reflecting the convergence of a deepening national cardiovascular disease burden, accelerating clinical awareness of timely biomarker assessment value, and the progressive integration of cardiac biomarkers diagnostics into acute care, emergency, and primary healthcare workflows across both public and private healthcare delivery networks. This growth path reflects a market advancing on durable structural foundations rather than episodic demand surges.

The product architecture defining this market's commercial structure is anchored in the consumables category, where reagents and kits command approximately 55% of total market share. This dominant position reflects the inherently recurring nature of diagnostic consumable demand where every test cycle across hospitals, centralized laboratories, and emergency care settings generates continuous replenishment requirements that sustain a commercially stable and predictable revenue base independently of capital equipment procurement timing. This consumables concentration creates a market structure whose revenue foundation is insulated from episodic institutional budget cycles, deriving its commercial resilience instead from the high frequency, operationally essential procurement activity that routine cardiac biomarker testing volumes generate across India's expanding diagnostic network.

The biomarker architecture reinforces the clinical primacy of troponin as the category's dominant testing paradigm, with troponin accounting for approximately 55% of total biomarker type market share. This leadership reflects the deep clinical familiarity, extensive real-world validation, and broad protocol integration that have established troponin as the reference biomarker across chest pain evaluation, myocardial infarction rule in and rule out workflows, and acute coronary syndrome management pathways in India's hospital and emergency care settings. As testing volumes expand and clinical confidence in high sensitivity assay platforms deepens, troponin's structural market authority is being progressively reinforced rather than challenged creating a demand concentration dynamic that sustains the segment's commercial leadership across both centralized and near patient diagnostic environments.

The forward outlook is defined by four converging structural forces the escalating national cardiovascular and non communicable disease burden that sustains institutional demand for timely cardiac diagnostic testing, the progressive regulatory formalization of in vitro diagnostic approval pathways under CDSCO that elevates quality standards while extending commercialization timelines, the technology transition toward high sensitivity troponin assay platforms that is reshaping clinical expectations for detection sensitivity and decision speed, and the large scale expansion of India's public health infrastructure encompassing 1,80,906 Ayushman Arogya Mandirs operationalized as of October 2025 that creates a structurally significant and geographically distributed decentralized demand base for near patient cardiac biomarker testing over the forecast period.

India Cardiac Biomarkers Diagnostics Market Growth DriverEscalating National Disease Burden Sustains Structural Cardiac Diagnostic Testing Demand

The escalating and institutionally documented cardiovascular and non communicable disease burden across India represents the primary structural driver of cardiac biomarker diagnostic demand functioning as a persistent clinical imperative that sustains institutional investment in timely rule in and rule out testing infrastructure across emergency departments, acute care units, and diagnostic networks confronting the country's most consequential population health challenge. This disease driven demand dynamic transcends cyclical healthcare budget fluctuations, reflecting a durable clinical necessity whose volume generation is structurally anchored in the irreducible requirement for accurate, fast cardiac event diagnosis across a patient population whose cardiovascular risk profile is deepening with demographic aging, lifestyle epidemiological transition, and expanding chronic disease identification through public screening programs.

The quantitative evidence validating this demand dynamic is documented with precision by the Press Information Bureau. Non communicable diseases account for over 66% of all deaths in India establishing the structural scale of the disease burden that cardiac biomarker testing is operationally positioned to address across the country's healthcare system. The breadth of at risk population visibility is further confirmed by treatment coverage data: 42.01 million people had received treatment for hypertension and 25.27 million for diabetes as of March 2025 collectively representing 89.7% of the national initiative target and confirming that a large and growing cohort of high cardiovascular risk individuals is actively engaged with India's formal healthcare system. These population health metrics validate a disease burden of sufficient scale and institutional visibility to sustain structural cardiac biomarker testing demand growth over the forecast period.

India Cardiac Biomarkers Diagnostics Market ChallengeRegulatory Formalization Elevates Compliance Thresholds and Extends Commercialization Timelines

The progressive formalization and structural strengthening of India's regulatory approval framework for in vitro diagnostics under CDSCO represents the most consequential supply side challenge confronting cardiac biomarker assay developers and suppliers creating systematic documentation, validation, and submission planning burdens that extend commercialization timelines, elevate pre market evidence requirements, and constrain the pace at which next generation cardiac biomarker assays reach clinical deployment across healthcare settings where structural demand is expanding. For smaller and mid tier market participants, this regulatory navigation burden creates an asymmetric competitive disadvantage relative to established diagnostics corporations with dedicated Indian regulatory affairs infrastructure and established compliance management systems.

The regulatory specificity of this challenge is established with authority by CDSCO and ICMR. All medical devices with the exception of Class A non sterile and non measuring devices remain under the active CDSCO licensing regime, imposing structured authorization obligations that compound across multi assay development pipelines and demand sustained regulatory team investment from commercialization stage manufacturers. The ICMR CDSCO framework's development and notification of nine draft standard evaluation protocols for in vitro diagnostic performance assessment communicated in their March 2025 notification further elevates the evidentiary quality threshold that cardiac diagnostic developers must meet with precision before achieving market authorization. As regulatory infrastructure matures and protocol standardization advances, compliance management capability is becoming an increasingly decisive competitive differentiator that shapes market access velocity and commercialization investment requirements over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Cardiac Biomarkers Diagnostics Market TrendHigh Sensitivity Troponin Adoption Reshapes Clinical Diagnostic Expectations

The accelerating clinical adoption and international regulatory validation of high sensitivity troponin assay platforms represents the defining technological trend reshaping India's cardiac biomarkers diagnostics market fundamentally elevating the analytical sensitivity threshold at which cardiac injury detection occurs and enabling earlier, more accurate acute myocardial infarction assessment that compresses clinical decision timelines, improves patient triage efficiency, and progressively raises institutional expectations for diagnostic platform performance across both centralized laboratory and near patient testing environments. This technological transition is moving the competitive differentiation axis beyond assay throughput and workflow compatibility into the domain of detection limit performance, rapid rule out protocol confidence, and point of care deployment accessibility dimensions that are redefining assay selection criteria at the institutional level across India's evolving diagnostic landscape.

The international regulatory validation momentum of this trend is documented with authority by the FDA whose approval precedents directly influence clinical awareness, technology adoption confidence, and product development investment priorities within India's diagnostic community. The Atellica IM High Sensitivity Troponin I assay received a substantial equivalence decision on 25 July 2024, confirming regulatory acceptance of next generation central laboratory high sensitivity platforms. The i STAT hs TnI cartridge with the i STAT 1 System received a substantial equivalence decision on 3 January 2025, extending high sensitivity troponin capability into portable near patient testing configurations directly relevant to India's expanding decentralized care infrastructure. As Indian providers increasingly evaluate cardiac biomarker platforms through the lens of faster turnaround and stronger rule out confidence, high sensitivity assay adoption is expected to deepen its penetration across India's hospital and emergency care networks over the forecast period.

India Cardiac Biomarkers Diagnostics Market OpportunityPublic Health Infrastructure Expansion Creates a Scalable Decentralized Demand Base

The large scale and institutionally committed expansion of India's public health infrastructure encompassing primary care facilities, integrated public health laboratories, and critical care networks across district and sub district geographies represents the market's most commercially scalable and structurally durable opportunity, providing a geographically distributed and progressively better equipped institutional demand base whose conversion into active cardiac biomarker testing volume is being systematically enabled by government infrastructure investment, diagnostic capacity development, and the progressive integration of near patient testing platforms into decentralized care delivery workflows. This opportunity extends the market's addressable commercial footprint well beyond its current metropolitan concentration unlocking demand from healthcare settings that are acquiring both the infrastructure and the clinical mandate to expand cardiac diagnostic capabilities.

The quantitative scale of this public health infrastructure opportunity is established with precision by the Ministry of Health and Family Welfare. A total of 1,80,906 Ayushman Arogya Mandirs were operationalized across the country as of October 31, 2025 establishing a vast first contact care network whose geographic reach creates a substantial institutional base for near patient cardiac biomarker testing, referral screening, and earlier identification of patients requiring advanced cardiac assessment. Complementing this primary care expansion, the PM ABHIM infrastructure development plan updated in July 2025 incorporates 744 Integrated Public Health Laboratories and 621 Critical Care Blocks, building the secondary and tertiary care diagnostic infrastructure that enables structured cardiac biomarker testing protocol adoption across district hospital and emergency care networks. Suppliers combining compact platform design, CDSCO compliant assay certification, and accessible deployment economics tailored to public sector procurement environments will capture disproportionate value from this structurally significant opportunity over the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

India Cardiac Biomarkers Diagnostics Market Segmentation Analysis

By Product

- Reagents & Kits

- Instruments/Analyzers

- Consumables & Accessories

The segment with highest market share under the Product Category is Reagents & Kits, accounting for approximately 55% of the total market. This dominant position reflects the deep structural alignment between consumable product economics and the operational requirements of cardiac biomarker testing where the inherently recurring nature of reagent and kit consumption across every diagnostic test cycle generates continuous, high frequency procurement demand that sustains a commercially stable revenue base across hospitals, reference laboratories, and emergency care settings regardless of capital equipment investment timing. With more than half of total market value concentrated within a single product category, reagents and kits define the commercial priorities, procurement relationship dynamics, and revenue generation architecture of the India cardiac biomarkers diagnostics market.

The structural leadership of this segment is further anchored in the demand predictability that routine clinical testing volumes create across India's expanding diagnostic network. Unlike capital equipment whose procurement follows episodic institutional budget cycles, reagent and kit consumption scales directly and consistently with diagnostic testing frequency creating a revenue generation dynamic whose commercial resilience is structurally insulated from short cycle purchasing variability. As cardiac biomarker testing volumes expand across both public and private healthcare settings driven by growing disease burden visibility, improving clinical awareness, and infrastructure investment across district and primary care networks reagent and kit consumption will compound in direct proportion to broader testing adoption. The segment's structural centrality to procurement patterns, revenue stability, and commercial market development is expected to remain comprehensively intact over the forecast period.

By Biomarker Type

- Troponin

- Cardiac Troponin I (cTnI)

- Cardiac Troponin T (cTnT)

- High-Sensitivity Troponin (hs-cTn)

- Creatine Kinase-MB (CK-MB)

- Myoglobin

- BNP and NT-proBNP

- Other Cardiac Biomarkers

The segment with highest market share under the Biomarker Type is Troponin, accounting for approximately 55% of the total market. This dominant position confirms troponin's structural centrality within India's acute cardiac diagnostic pathways where its established clinical sensitivity, extensive real world validation evidence, and deep integration into myocardial infarction assessment, chest pain evaluation, and acute coronary syndrome management protocols make it the reference biomarker of choice across emergency departments, intensive care units, and acute care settings nationwide. With more than half of total market value anchored in troponin based testing, the segment defines the clinical, commercial, and technological agenda of the India cardiac biomarkers diagnostics market establishing the assay performance benchmarks and institutional protocol standards against which all biomarker testing innovations are evaluated.

The structural leadership of troponin is being actively reinforced by the accelerating global regulatory validation of high sensitivity assay platforms that are expanding its clinical utility beyond conventional central laboratory applications into near patient and point of care testing environments a technology trajectory whose commercial implications are directly relevant to India's evolving diagnostic infrastructure. As Indian healthcare providers increasingly evaluate cardiac biomarker platforms through the lens of faster turnaround, stronger rule out diagnostic confidence, and more efficient emergency care workflow integration, troponin's clinical authority across both established and next generation testing formats positions it as the unambiguous beneficiary of the market's technological evolution. The biomarker's structural market dominance as the primary driver of testing volume, product selection, and clinical protocol development is expected to deepen over the forecast period.

List of Companies Covered in India Cardiac Biomarkers Diagnostics Market

The companies listed below are highly influential in the India cardiac biomarkers diagnostics market, with a significant market share and a strong impact on industry developments.

- BioMérieux

- Thermo Fisher Scientific

- Ortho Clinical Diagnostics

- Roche Diagnostics

- Abbott Laboratories

- Quidel Corporation

- Danaher Corporation/Beckman Coulter

- Siemens Healthineers

- Randox Laboratories

- Bio-Rad Laboratories

Market News & Updates

- Siemens Healthineers, 2026:

Siemens Healthineers’ official India pages position High-Sensitivity Troponin I as the latest addition to its cardiac menu for earlier myocardial infarction diagnosis, and its India point-of-care cardiac section highlights first results in as fast as 14 minutes with subsequent results in as fast as four minutes. This is highly relevant for India because faster, high-sensitivity troponin workflows can improve chest-pain triage in busy hospitals and emergency settings, supporting wider uptake of advanced cardiac biomarker testing as providers look for quicker, more scalable rule-in and rule-out pathways.

- QuidelOrtho, 2026:

QuidelOrtho’s official India page is promoting the QUIDEL TRIAGETRUE High Sensitivity Troponin I Test for quantitative determination of troponin I in whole blood and plasma on the TRIAGE METERPRO platform. This matters for the India cardiac biomarkers diagnostics market because a portable high-sensitivity troponin option can help extend advanced myocardial infarction testing beyond large central laboratories, supporting adoption in decentralised and acute-care settings where turnaround time, workflow simplicity, and instrument footprint are major commercial drivers.

Frequently Asked Questions

Related Report

- Market Segmentation

- Research Scope

- Research Methodology

- Definitions and Assumptions

- Executive Summary

- India Cardiac Biomarkers Diagnostics Market Policies, Regulations, and Standards

- India Cardiac Biomarkers Diagnostics Market Dynamics

- Growth Factors

- Challenges

- Trends

- Opportunities

- India Cardiac Biomarkers Diagnostics Market Statistics, 2022-2032F

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Product

- Reagents & Kits- Market Insights and Forecast 2022-2032, USD Million

- Instruments/Analyzers- Market Insights and Forecast 2022-2032, USD Million

- Consumables & Accessories- Market Insights and Forecast 2022-2032, USD Million

- By Biomarker Type

- Troponin- Market Insights and Forecast 2022-2032, USD Million

- Cardiac Troponin I (cTnI)- Market Insights and Forecast 2022-2032, USD Million

- Cardiac Troponin T (cTnT)- Market Insights and Forecast 2022-2032, USD Million

- High-Sensitivity Troponin (hs-cTn)- Market Insights and Forecast 2022-2032, USD Million

- Creatine Kinase-MB (CK-MB)- Market Insights and Forecast 2022-2032, USD Million

- Myoglobin- Market Insights and Forecast 2022-2032, USD Million

- BNP and NT-proBNP- Market Insights and Forecast 2022-2032, USD Million

- Other Cardiac Biomarkers- Market Insights and Forecast 2022-2032, USD Million

- Troponin- Market Insights and Forecast 2022-2032, USD Million

- By Application

- Acute Coronary Syndrome (ACS)- Market Insights and Forecast 2022-2032, USD Million

- Myocardial Infarction (MI)- Market Insights and Forecast 2022-2032, USD Million

- Congestive Heart Failure (CHF)- Market Insights and Forecast 2022-2032, USD Million

- Chest Pain/Emergency Triage- Market Insights and Forecast 2022-2032, USD Million

- Risk Stratification & Prognosis- Market Insights and Forecast 2022-2032, USD Million

- Other Cardiac Conditions- Market Insights and Forecast 2022-2032, USD Million

- By Testing Location

- Laboratory Testing- Market Insights and Forecast 2022-2032, USD Million

- Point-of-Care Testing (POCT)- Market Insights and Forecast 2022-2032, USD Million

- By End User

- Hospitals- Market Insights and Forecast 2022-2032, USD Million

- Diagnostic Laboratories- Market Insights and Forecast 2022-2032, USD Million

- Emergency Departments- Market Insights and Forecast 2022-2032, USD Million

- Cardiac/Specialty Clinics- Market Insights and Forecast 2022-2032, USD Million

- Ambulatory Care Centers- Market Insights and Forecast 2022-2032, USD Million

- Others- Market Insights and Forecast 2022-2032, USD Million

- By Technology

- Chemiluminescence Immunoassay- Market Insights and Forecast 2022-2032, USD Million

- Fluorescence Immunoassay- Market Insights and Forecast 2022-2032, USD Million

- ELISA- Market Insights and Forecast 2022-2032, USD Million

- Lateral Flow/Rapid Immunoassay- Market Insights and Forecast 2022-2032, USD Million

- Other Assay Technologies- Market Insights and Forecast 2022-2032, USD Million

- By Sample Type

- Whole Blood- Market Insights and Forecast 2022-2032, USD Million

- Plasma- Market Insights and Forecast 2022-2032, USD Million

- Serum- Market Insights and Forecast 2022-2032, USD Million

- By Region

- North

- East

- West

- South

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product

- Market Size & Growth Outlook

- India Reagents & Kits Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Biomarker Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Testing Location- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Sample Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Instruments/Analyzers Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Biomarker Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Testing Location- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Sample Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- India Consumables & Accessories Market Statistics, 2022-2032

- Market Size & Growth Outlook

- By Revenues in USD Million

- Market Segmentation & Growth Outlook

- By Biomarker Type- Market Insights and Forecast 2022-2032, USD Million

- By Application- Market Insights and Forecast 2022-2032, USD Million

- By Testing Location- Market Insights and Forecast 2022-2032, USD Million

- By End User- Market Insights and Forecast 2022-2032, USD Million

- By Technology- Market Insights and Forecast 2022-2032, USD Million

- By Sample Type- Market Insights and Forecast 2022-2032, USD Million

- By Region- Market Insights and Forecast 2022-2032, USD Million

- Market Size & Growth Outlook

- Competitive Outlook

- Company Profiles

- Roche Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Abbott Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Quidel Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Danaher Corporation/Beckman Coulter

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Siemens Healthineers

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- bioMérieux

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thermo Fisher Scientific

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ortho Clinical Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Randox Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bio-Rad Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Roche Diagnostics

- Company Profiles

- Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product |

|

| By Biomarker Type |

|

| By Application |

|

| By Testing Location |

|

| By End User |

|

| By Technology |

|

| By Sample Type |

|

| By Region |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.