Germany Fire Pump Market Report: Trends, Growth and Forecast (2026-2032)

By Pump Type (Centrifugal Pumps (Overhung Pumps, Vertical Inline, Horizontal End Suction), Split Case Pumps (Single/Two Stage, Multi Stage)), Positive Displacement Pumps (Diaphragm Pumps, Piston Pumps), By Mode of Operation (Diesel Fire Pump, Electric Fire Pump, Others), By End-User (Residential, Commercial, Industrial) ... Read more

|

Major Players

|

Germany Fire Pump Market Statistics and Insights, 2026

- Market Size Statistics

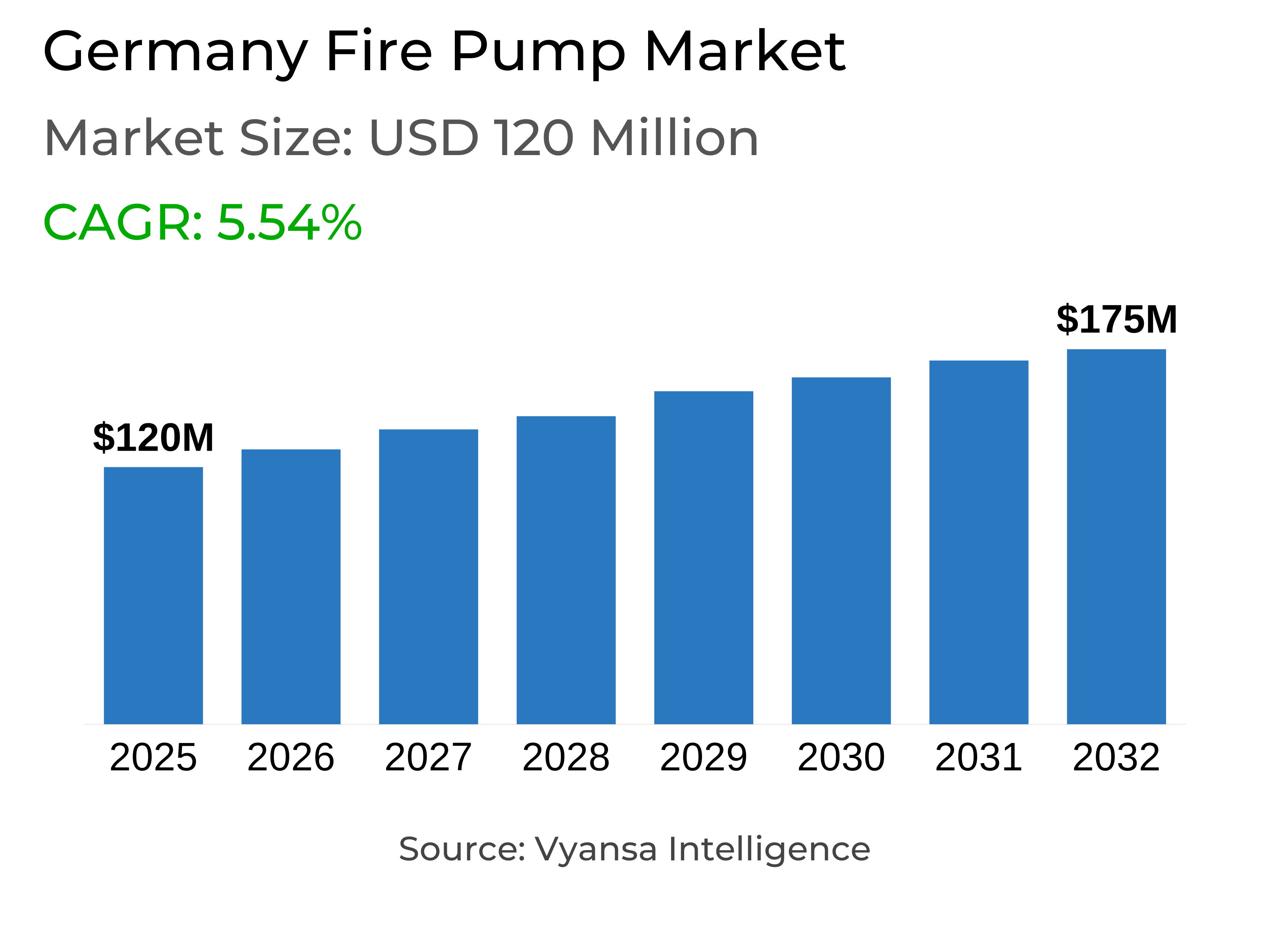

- Fire Pump in Germany is estimated at $ 120 Million.

- The market size is expected to grow to $ 175 Million by 2032.

- Market to register a CAGR of around 5.54% during 2026-32.

- Pump Type Segment

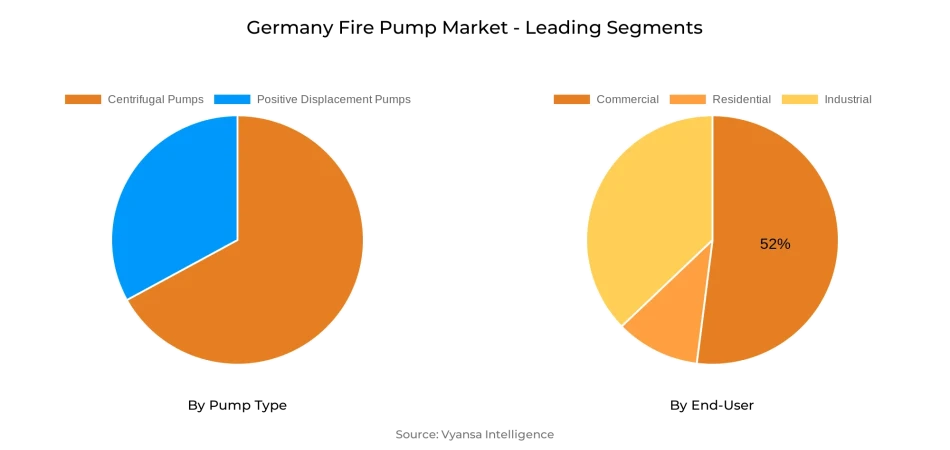

- Centrifugal Pumps continues to dominate the market.

- Competition

- More than 10 companies are actively engaged in producing Fire Pump in Germany.

- Top 5 companies acquired the maximum share of the market.

- WILO SE, Ebara Corporation, ITT Goulds Pumps, Flowserve Corporation, Pentair PLC etc., are few of the top companies.

- End-User

- Commercial grabbed 52% of the market.

Germany Fire Pump Market Outlook

The Germany Fire Pump Market is estimated to be approximately USD 120 million in 2025 and is expected to grow gradually to USD 175 million by the year 2032. This market growth is furthered by Germany's stringent fire safety standards, which require adherence to DIN standards in all states and municipalities. With career fire departments operating in large cities and more than 22,000 volunteer services responding to over one million emergencies each year, the significance of dependable fire pump systems is solidly rooted in the nation's infrastructure.

Centrifugal pumps lead the way in market dominance as a result of their efficiency, reliability, and compatibility with high-capacity fire suppression systems. Their extensive application within commercial and industrial buildings, as well as strong supply chains and servicing networks, guarantees that they are the solution of choice. Positive displacement pumps, though found in niche applications, play only a niche role. This overwhelming dependence on centrifugal technology solidifies their ongoing dominance in new installations and replacement market demand.

Among the end users, commercial use has the largest proportion at 52% in 2025, which indicates high compliance needs of office buildings, shopping complexes, and hotels. Such buildings, given their size and occupancy rates, continually invest in sophisticated fire protection equipment to ensure human and asset safety. Meanwhile, the residential segment is growing at the fastest rate due to tighter building codes, energy-efficient home policies, and government-sponsored renovation programs.

In the future, Germany's plans to modernize its infrastructure, industrial development driven by automation, and integration of intelligent building systems are likely to open new avenues for sophisticated fire pumps. With greater focus on digital monitoring, predictive maintenance, and compliance-driven demand, the market will continue to experience stable long-term growth through 2032.

Germany Fire Pump Market Growth Driver

Regulatory Mandates Strengthen Market Expansion

Germany's stringent fire protection codes continue to prompt uptake of sophisticated pumping systems in all types of construction. Conformance with DIN standards is legally required throughout the country, with varying state requirements assuring broad implementation. Urban areas of over 100,000 residents are required to have professional fire departments, with smaller communities depending on over 22,000 volunteer fire departments. With German fire services dealing with over 1 million emergency responses every year, the essential nature of trustworthy fire protection infrastructure is firmly rooted. Institutional systems provide steady demand for equipment that ensures speedy response and working efficiency.

Building codes also reinforce this demand by mandating detailed fire protection measures, including compartmentalization, emergency exits, and strict fire resistance levels. The industrial base, supported by widespread robotics and automation, further elevates the need for sophisticated fire protection. In 2023, 49% of German manufacturers with more than 250 employees used industrial robots, underscoring the complex industrial environment where advanced fire pumping systems remain indispensable.

Germany Fire Pump Market Challenge

High Costs and Skilled Workforce Shortages Impede Growth

The high capital investment for sophisticated fire pump solutions creates substantial hurdles, especially for small and medium enterprises. The cost of building in Germany has increased exponentially, with the average cost per single-family residence jumping from €200,000 in 2010 to almost €390,000 by 2024, a 95% gain. This increase has a trickle-down effect on larger infrastructure investments, with most smaller players unwilling to invest in high-quality fire protection gear due to the prohibitive cost. As such, the initial cost confines system adoption within price-conscious market niches.

Aside from cost issues, integration complexity across disparate building management platforms creates other challenges. Labor expenses increased 2.5% in early 2024 over the previous quarter, adding to installation and maintenance challenges. Adding to this, shortages of qualified technicians create delays in deployments and system maintenance. Others put off investments in high-strength solutions, valuing short-term savings over long-term protection. While regulations are strict, these cost and labor considerations create persisting reluctance to embracing premium-grade fire pump systems.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany Fire Pump Market Trend

Digitalization and Smart Technologies Redefine Fire Safety

The digitization of solutions is revolutionizing Germany's fire protection sector, converting conventional suppression systems into smart safety networks. Intelligent fire pumps with IoT sensors, predictive analytics, and automated procedures provide round-the-clock system monitoring and real-time data capturing. The sophisticated systems provide remote monitoring, automatic testing, and proactive scheduling of maintenance, moving strategies from reactive to predictive safety management. Their contribution to optimized operations and emergency response is fueling consistent uptake among contemporary infrastructure initiatives utilizing cutting-edge technologies.

Regulatory policies are supporting this trend toward comprehensive safety management. The Buildings Energy Act (GEG) mandates non-residential buildings with more than 290 kWh heating systems to equip with building automation platforms that meet DIN V 18599-11:2018-09 standards. Combined with industrial automation's estimated 10.88% compound annual growth rate through 2032, these regulations boost the demand for connected safety solutions. Fire pump systems seamlessly integrated into larger building automation networks are becoming increasingly the norm, boosting Germany's market position as a pioneer for intelligent fire protection technology.

Germany Fire Pump Market Opportunity

Infrastructure Modernization Unlocks Market Potential

The extensive large-scale modernization programs in Germany open tremendous potential for fire protection system installation. The government initiated a €500 billion infrastructure program over 12 years, with €57 billion allocated for climate measures and €18.9 billion for building renovations in 2024 alone. Such investments not only foster energy transition objectives but also facilitate extensive fire safety system upgrades throughout new and existing buildings. Mass urban developments and modernization plans present fertile ground for broader implementation of sophisticated pumping technologies.

The industrial automation market is yet another prime opportunity, worth €7.72 billion in 2024 and expected to rise to €14.84 billion by 2032. Germany is Europe's leader in automation, boasting 429 robots per 10,000 workers, and has high-value industrial complexes that need extensive fire protection. Policies requiring 65% of the heating system to be renewable energy promote system retrofits that have new safety features added. Along with smart city and digitalization initiatives, these elements pose enormous opportunities for integrated fire pump uptake throughout Germany's changing infrastructure environment.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany Fire Pump Market Segmentation Analysis

By Pump Type

- Centrifugal Pumps

- Positive Displacement Pumps

Among pump type segment, centrifugal pumps continue to hold the top spot and enjoy the highest market share in the Germany Fire Pump Market. They are most widely used due to their efficiency, reliability, and proven capability to perform consistently in a variety of conditions. These units are best suited for large-scale fire-fighting requirements, with the high flow rates needed for commercial and industrial operations. With their established technology base and widespread availability, their stronghold on the market is further enhanced.

Centrifugal pumps are also subject to operational ease, less maintenance requirements, and high compatibility with installed fire safety equipment. German fire brigades, backed by reliable supply chains and high-strength servicing networks, have high preference for these systems due to the high trust they have in them. Positive displacement pumps find application in niche applications demanding accurate flow regulation, and thus they are a niche market. Centrifugal systems are still the industry norm, which means that they continue to dominate new installations as well as replacement projects in Germany's built environment.

By End-User

- Residential

- Commercial

- Industrial

Commercial end users are the market share leader in the Germany Fire Pump Market and account for 52% of installations. Such dominance is a result of the size and complexity of the commercial infrastructure of the country, including office towers, retail complexes, hospitality complexes, and public institutions. These installations have stringent fire protection needs owing to high population density, multiple exit routes, and having to protect high-value assets, making sound pumping systems critical. Compliance and risk considerations drive steady investment in innovative solutions throughout this sector.

The residential sector, in the meanwhile, is the quickest growing segment, anticipated to develop at a 6.9% CAGR. More stringent building codes, increased safety consciousness, and renewed residential construction activity drive this expansion. Even during periods of fluctuations in permitting activity, demand continues to be strong for efficient and affordable residential fire safety solutions. Government incentives encouraging safer and energy-efficient housing also support adoption, especially in retrofitting. With tightening safety standards and increasing consciousness, residential end users are a dynamic growth driver in tandem with the leading commercial segment.

Top Companies in Germany Fire Pump Market

The top companies operating in the market include WILO SE, Ebara Corporation, ITT Goulds Pumps, Flowserve Corporation, Pentair PLC, Sulzer Limited, Grundfos Holding A/S, KSB SE & Co. KGaA, Patterson (Gorman Rupp), Armstrong, etc., are the top players operating in the Germany Fire Pump Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Germany Fire Pump Market Policies, Regulations, and Standards

4. Germany Fire Pump Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Germany Fire Pump Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1.By Revenues in US$ Million

5.2. Market Segmentation & Growth Outlook

5.2.1.By Pump Type

5.2.1.1. Centrifugal Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1.1. Overhung Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1.2. Vertical Inline- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1.3. Horizontal End Suction- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Split Case Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.1. Single/Two Stage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2.2. Multi Stage- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Positive Displacement Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Diaphragm Pumps- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Piston Pumps - Market Insights and Forecast 2022-2032, USD Million

5.2.2.By Mode of Operation

5.2.2.1. Diesel Fire Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Electric Fire Pump- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.3.By End-User

5.2.3.1. Residential- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Commercial- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Industrial- Market Insights and Forecast 2022-2032, USD Million

5.2.4.By Competitors

5.2.4.1. Competition Characteristics

5.2.4.2. Market Share & Analysis

6. Germany Centrifugal Fire Pump Market Statistics, 2020-2030F

6.1. Market Size & Growth Outlook

6.1.1.By Revenues in US$ Million

6.2. Market Segmentation & Growth Outlook

6.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2.By Mode of Operation- Market Insights and Forecast 2022-2032, USD Million

6.2.3.By End-User- Market Insights and Forecast 2022-2032, USD Million

7. Germany Positive Displacement Fire Pump Market Statistics, 2020-2030F

7.1. Market Size & Growth Outlook

7.1.1.By Revenues in US$ Million

7.2. Market Segmentation & Growth Outlook

7.2.1.By Pump Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2.By Mode of Operation- Market Insights and Forecast 2022-2032, USD Million

7.2.3.By End-User- Market Insights and Forecast 2022-2032, USD Million

8. Competitive Outlook

8.1. Company Profiles

8.1.1.Flowserve Corporation

8.1.1.1. Business Description

8.1.1.2. Product Portfolio

8.1.1.3. Collaborations & Alliances

8.1.1.4. Recent Developments

8.1.1.5. Financial Details

8.1.1.6. Others

8.1.2.Pentair PLC

8.1.2.1. Business Description

8.1.2.2. Product Portfolio

8.1.2.3. Collaborations & Alliances

8.1.2.4. Recent Developments

8.1.2.5. Financial Details

8.1.2.6. Others

8.1.3.Sulzer Limited

8.1.3.1. Business Description

8.1.3.2. Product Portfolio

8.1.3.3. Collaborations & Alliances

8.1.3.4. Recent Developments

8.1.3.5. Financial Details

8.1.3.6. Others

8.1.4.Grundfos Holding A/S

8.1.4.1. Business Description

8.1.4.2. Product Portfolio

8.1.4.3. Collaborations & Alliances

8.1.4.4. Recent Developments

8.1.4.5. Financial Details

8.1.4.6. Others

8.1.5.KSB SE & Co. KGaA

8.1.5.1. Business Description

8.1.5.2. Product Portfolio

8.1.5.3. Collaborations & Alliances

8.1.5.4. Recent Developments

8.1.5.5. Financial Details

8.1.5.6. Others

8.1.6.WILO SE

8.1.6.1. Business Description

8.1.6.2. Product Portfolio

8.1.6.3. Collaborations & Alliances

8.1.6.4. Recent Developments

8.1.6.5. Financial Details

8.1.6.6. Others

8.1.7.Ebara Corporation

8.1.7.1. Business Description

8.1.7.2. Product Portfolio

8.1.7.3. Collaborations & Alliances

8.1.7.4. Recent Developments

8.1.7.5. Financial Details

8.1.7.6. Others

8.1.8.ITT Goulds Pumps

8.1.8.1. Business Description

8.1.8.2. Product Portfolio

8.1.8.3. Collaborations & Alliances

8.1.8.4. Recent Developments

8.1.8.5. Financial Details

8.1.8.6. Others

8.1.9.Patterson (Gorman Rupp)

8.1.9.1. Business Description

8.1.9.2. Product Portfolio

8.1.9.3. Collaborations & Alliances

8.1.9.4. Recent Developments

8.1.9.5. Financial Details

8.1.9.6. Others

8.1.10. Armstrong

8.1.10.1. Business Description

8.1.10.2. Product Portfolio

8.1.10.3. Collaborations & Alliances

8.1.10.4. Recent Developments

8.1.10.5. Financial Details

8.1.10.6. Others

9. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Pump Type |

|

| By Mode of Operation |

|

| By End-User |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.