Germany Beer Market Report: Trends, Growth and Forecast (2026-2032)

By Product Type (Dark Beer (Ale, Sorghum Beer, Weissbier/Weizen/Wheat Beer), Lager (Flavoured/Mixed Lager, Standard Lager (Premium Lager (Domestic Premium Lager, Imported Premium Lager), Mid-Priced Lager (Domestic Mid-Priced Lager, Imported Mid-Priced Lager), Economy Lager (Domestic Economy Lager, Imported Economy Lager))), Non/Low Alcohol Beer (Low Alcohol Beer, Non Alcoholic Beer), Stout, Others (Porter, Malt etc.)), By Production (Macro Brewery, Micro Brewery, Craft Brewery), By Packaging Type (Bottles, Cans, Others), By Sales Channel (On-Trade, Off-Trade) ... Read more

|

Major Players

|

Germany Beer Market Statistics and Insights, 2026

- Market Size Statistics

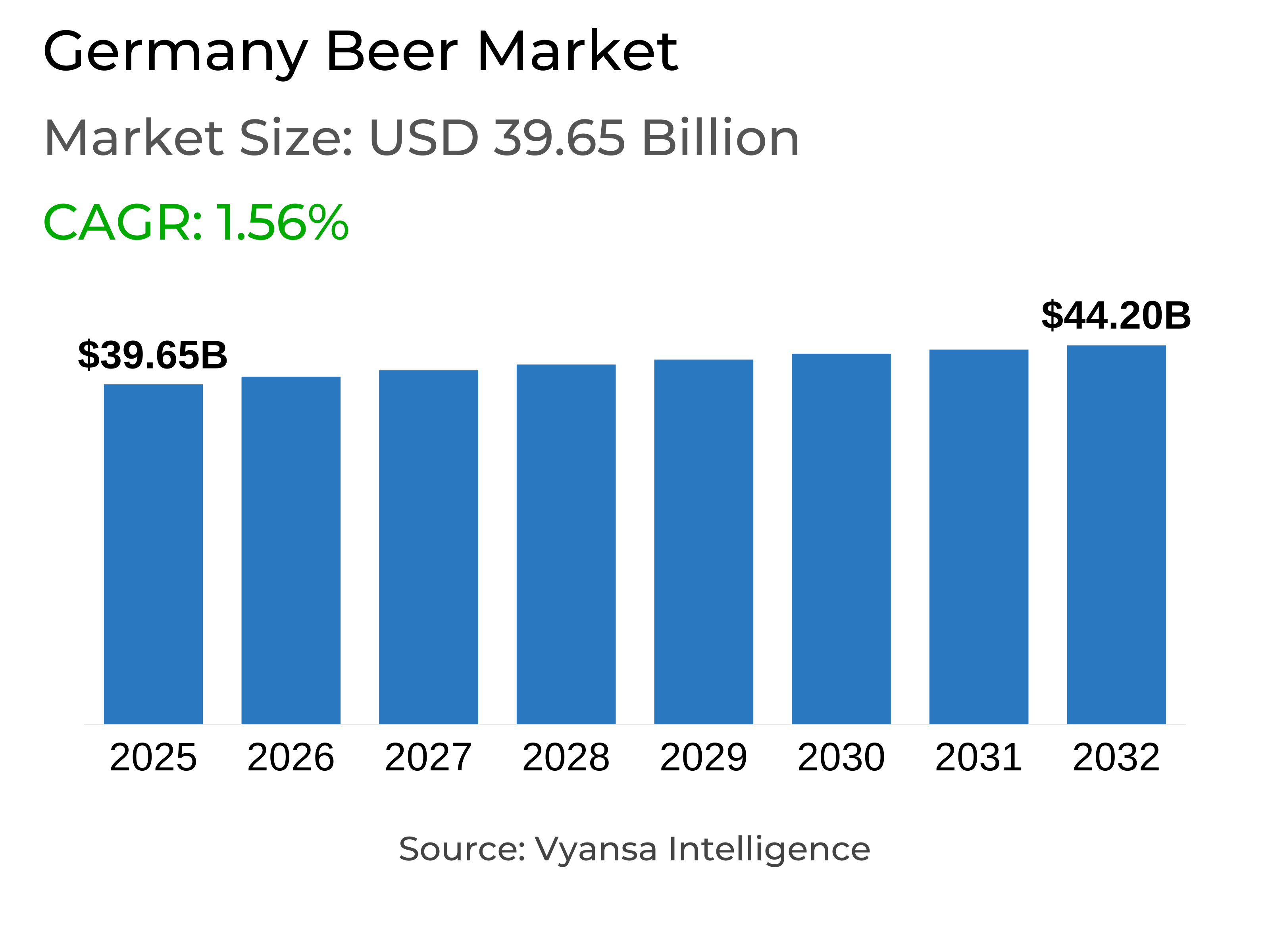

- Beer in germany is estimated at USD 39.65 billion.

- The market size is expected to grow to USD 44.2 billion by 2032.

- Market to register a cagr of around 1.56% during 2026-32.

- Product Type Shares

- Lager grabbed market share of 70%.

- Competition

- More than 20 companies are actively engaged in producing beer in germany.

- Top 5 companies acquired around 25% of the market share.

- Carlsberg Deutschland GmbH, Aldi Einkauf GmbH & Co oHG, Kulmbacher Brauerei AG, Radeberger Gruppe KG, Krombacher Brauerei Bhd Schadeberg GmbH & Co KG etc., are few of the top companies.

- Sales Channel

- On-trade grabbed 70% of the market.

Germany Beer Market Outlook

The Germany beer market is valued at $39.65 billion in 2025 and is expected to grow to $44.2 billion by 2032, at a CAGR of approximately 1.56% from 2026–2032. Overall volume sales of beer are set to drop slightly during the forecast period, capturing the continued trend among young adults towards moderate consumption and alternative alcoholic drinks like RTDs. In spite of this, value sales are set to stay stable because of premiumisation and innovation in specialty beers. Domestic premium lager remains to lead the market, thanks to the popularity of Helles and other regional trends.

Lager accounts for a 70% market share, still the biggest product type. Mid-range and premium lagers will remain subject to price competition, but stouts are poised for modest growth as they continue to build momentum in the on-trade channel. Flavoured and mixed lagers will be set to become a significant growth area, aimed at competing with RTDs and appealing to those looking for novelty and variety. Non-alcoholic beer will benefit from rising health awareness and wider product availability, with new launches across multiple beer styles enhancing its appeal.

By distribution channel, on-trade is 70% of the market, followed by bars, cafés, and pubs. Though the number of foodservice outlets has reduced, important cities and tourist destinations offer good potential for expansion in premium, stout, and craft products. Off-trade channels, such as supermarkets and discounters, will continue to lead volumes sales via promotions, competitive pricing, and small pack sizes. Discounters are still active, targeting price-conscious end users under a moderate economic climate.

The competitive market will be highly fragmented and subject to regional loyalty, with bigger players such as Radeberger Gruppe and Krombacher Brauerei staying at the forefront, but remaining niche players smaller craft breweries and microbreweries staying niche-based. Flavour innovation, alcohol content, and packaging, along with non-alcoholic beers, will dictate the market, keeping Germany's beer Market competitive in line with evolving end users culture while maintaining sustainable growth through the forecast period.

Germany Beer Market Growth DriverExpansion of Non-Alcoholic Beer

Germany Beer Market is fueled by the increasing popularity of non-alcoholic beers as end users increasingly practice responsible drinking and health-oriented living. Categories such as Clausthaler, Jever Fun, Beck's Blue Lemon 0.0, Einbecker Null Bock, and Augustiner Alkoholfrei Hell 0.5% appeal both younger adults and the sober-curious crowd, broadening the category's appeal.

Technological progress in brewing retains flavour while eliminating alcohol, improving the experience for those looking for alternatives to regular beer or RTDs. Non-alcoholic beer is gaining prominence across grocery retailers and specialist stores, backed by new products and flavor innovation. It drives volume and value sales, enabling breweries to diversify portfolios, build brand affinity, and respond to changing drinking habits. Growing health consciousness and lifestyle factors make non-alcoholic beer a major growth engine for the Germany Beer Market.

Germany Beer Market TrendPremiumization and Flavour Innovation

A strong shift toward premiumization and innovative flavors is shaping the Germany beer market, as end users increasingly seek unique and high-quality drinking experiences. end users are more and more opting for premium lagers, stouts, and specialty beers due to their quality, taste, and authenticity. Manufacturers launch new flavoured and blended lagers such as X² Cola, X² Ice Boost Energy, and X² Spritz to rival spirits-based and wine-based RTDs.

Smaller-pack sizes, seasonal offerings, and local beer variants appeal to women, ales newcomers, and young adults. Helles, a Bavarian-style lager, picking up favor outside its home region also reflects the trend toward distinctive, quality brewing experiences. These trends fuel value growth and differentiation in a split market, making brewers continue to innovate while staying relevant amid flat overall Germany beer volumes. Premiumization and flavor-based innovation remain key to market dynamics.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany Beer Market OpportunityInnovative Formats and Specialty Variants

Germany Beer Market offers opportunities with innovative formats, flavoured lagers, and specialty variants. With moderate consumption becoming increasingly popular, breweries can create fruit-flavored, mixed, or season-specific beers with appeal for younger adults and health-oriented end users. Products such as Bitburger's X² range, Beck's Blue Lemon 0.0, and non-alcoholic Bock beer provide differentiation and tap seasonal or occasion-based consumption.

Increased product availability in discounters, specialty stores, and urban on-trade channels offers additional growth opportunities. Smaller pack sizes, regional exclusives, and limited-edition products enable brewers to capture end users who are looking for variety. New developments in flavor, alcohol strength, and packaging enable brands to gain incremental sales, build brand loyalty, and compete in Germany's changing beer market during the forecast period.

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany Beer Market Segmentation Analysis

By Product Type

- Dark Beer

- Lager

- Non/Low Alcohol Beer

- Stout

The segment with highest market share under Product Type is lager, of which this largest market share is around 70%. Lager is the most popular type of beer consumed in Germany, enjoying its powerful tradition, extensive coverage, and end users familiarity. Though its volume sales are flat, premium and craft versions of lager are slowly increasing in popularity, demonstrating end users' affinity for quality and distinctive flavour experiences.

During the forecast period, lager is set to continue with its leading role with backing from flavour, packaging, and limited-edition innovations. Pack sizes of 0.33L cans and bottles will appeal to young end users and moderation seekers, while premium and craft offerings of lager will fuel value growth. These tactics help lager remain at the heart of Germany's beer market despite competition from emerging beer styles.

By Sales Channel

- On-Trade

- Off-Trade

The segment with highest market share under Sales Channel is on-trade, with this highest market share being approximately 70%. The key channels for beer consumption in Germany are pubs, bars, and restaurants, indicating the strong beer culture and social consumption orientation of the country. On-trade is preferred for fresh draught beer and premium occasions by end users, thereby retaining its stronghold even with off-trade retail growth.

On-trade will continue to be the most important channel for beer sales during the forecast period, with support from draught innovation, seasonals, and craft beer occasions. Breweries will cooperate with restaurants and pubs to introduce limited series and taproom exclusives. Emphasis on on-trade guarantees ongoing end users interaction and underlines the cultural and social significance of beer in Germany.

Top Companies in Germany Beer Market

The top companies operating in the market include Carlsberg Deutschland GmbH, Aldi Einkauf GmbH & Co oHG, Kulmbacher Brauerei AG, Radeberger Gruppe KG, Krombacher Brauerei Bhd Schadeberg GmbH & Co KG, Oettinger Brauerei GmbH, Brauerei C & A Veltins GmbH & Co KG, Paulaner Brauerei GmbH & Co KG, Warsteiner Brauerei Haus Cramer GmbH & Co KG, Karlsberg Brauerei GmbH & Co KG, etc., are the top players operating in the germany beer market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Germany Beer Market Policies, Regulations, and Standards

4. Germany Beer Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Germany Beer Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1. By Revenues in US$ Million

5.1.2. By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1. By Product Type

5.2.1.1. Dark Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.1. Ale- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.2. Sorghum Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.1.3. Weissbier/Weizen/Wheat Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.1. Flavoured/Mixed Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2. Standard Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.1. Premium Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.1.1. Domestic Premium Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.1.2. Imported Premium Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.2. Mid-Priced Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.2.1. Domestic Mid-Priced Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.2.2. Imported Mid-Priced Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.3. Economy Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.3.1. Domestic Economy Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2.2.3.2. Imported Economy Lager- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. Non/Low Alcohol Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.1. Low Alcohol Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3.2. Non Alcoholic Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Stout- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Others (Porter, Malt etc.) - Market Insights and Forecast 2022-2032, USD Million

5.2.2. By Production

5.2.2.1. Macro Brewery- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Micro Brewery- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Craft Brewery- Market Insights and Forecast 2022-2032, USD Million

5.2.3. By Packaging Type

5.2.3.1. Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Cans- Market Insights and Forecast 2022-2032, USD Million

5.2.3.3. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.4. By Sales Channel

5.2.4.1. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5. By Competitors

5.2.5.1. Competition Characteristics

5.2.5.2. Market Share & Analysis

6. Germany Dark Beer Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1. By Revenues in US$ Million

6.1.2. By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

6.2.2. By Production- Market Insights and Forecast 2022-2032, USD Million

6.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Germany Lager Beer Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1. By Revenues in US$ Million

7.1.2. By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1. By Product Type- Market Insights and Forecast 2022-2032, USD Million

7.2.2. By Production- Market Insights and Forecast 2022-2032, USD Million

7.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Germany Non/Low Alcohol Beer Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1. By Revenues in US$ Million

8.1.2. By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1. By Production- Market Insights and Forecast 2022-2032, USD Million

8.2.2. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.3. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Germany Stout Beer Market Statistics, 2022-2032F

9.1. Market Size & Growth Outlook

9.1.1. By Revenues in US$ Million

9.1.2. By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1. By Production- Market Insights and Forecast 2022-2032, USD Million

9.2.2. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.3. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Competitive Outlook

10.1.Company Profiles

10.1.1. Radeberger Gruppe KG

10.1.1.1. Business Description

10.1.1.2. Product Portfolio

10.1.1.3. Collaborations & Alliances

10.1.1.4. Recent Developments

10.1.1.5. Financial Details

10.1.1.6. Others

10.1.2. Krombacher Brauerei Bhd Schadeberg GmbH & Co KG

10.1.2.1. Business Description

10.1.2.2. Product Portfolio

10.1.2.3. Collaborations & Alliances

10.1.2.4. Recent Developments

10.1.2.5. Financial Details

10.1.2.6. Others

10.1.3. Oettinger Brauerei GmbH

10.1.3.1. Business Description

10.1.3.2. Product Portfolio

10.1.3.3. Collaborations & Alliances

10.1.3.4. Recent Developments

10.1.3.5. Financial Details

10.1.3.6. Others

10.1.4. Brauerei C & A Veltins GmbH & Co KG

10.1.4.1. Business Description

10.1.4.2. Product Portfolio

10.1.4.3. Collaborations & Alliances

10.1.4.4. Recent Developments

10.1.4.5. Financial Details

10.1.4.6. Others

10.1.5. Paulaner Brauerei GmbH & Co KG

10.1.5.1. Business Description

10.1.5.2. Product Portfolio

10.1.5.3. Collaborations & Alliances

10.1.5.4. Recent Developments

10.1.5.5. Financial Details

10.1.5.6. Others

10.1.6. Carlsberg Deutschland GmbH

10.1.6.1. Business Description

10.1.6.2. Product Portfolio

10.1.6.3. Collaborations & Alliances

10.1.6.4. Recent Developments

10.1.6.5. Financial Details

10.1.6.6. Others

10.1.7. Aldi Einkauf GmbH & Co oHG

10.1.7.1. Business Description

10.1.7.2. Product Portfolio

10.1.7.3. Collaborations & Alliances

10.1.7.4. Recent Developments

10.1.7.5. Financial Details

10.1.7.6. Others

10.1.8. Kulmbacher Brauerei AG

10.1.8.1. Business Description

10.1.8.2. Product Portfolio

10.1.8.3. Collaborations & Alliances

10.1.8.4. Recent Developments

10.1.8.5. Financial Details

10.1.8.6. Others

10.1.9. Warsteiner Brauerei Haus Cramer GmbH & Co KG

10.1.9.1. Business Description

10.1.9.2. Product Portfolio

10.1.9.3. Collaborations & Alliances

10.1.9.4. Recent Developments

10.1.9.5. Financial Details

10.1.9.6. Others

10.1.10. Karlsberg Brauerei GmbH & Co KG

10.1.10.1. Business Description

10.1.10.2. Product Portfolio

10.1.10.3. Collaborations & Alliances

10.1.10.4. Recent Developments

10.1.10.5. Financial Details

10.1.10.6. Others

11. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Product Type |

|

| By Production |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.