Germany Alcoholic Drinks Market Report: Trends, Growth and Forecast (2026-2032)

By Type (Beer, Cider/Perry, RTDs, Spirits, Wine), By Alcohol Content (High, Medium, Low), By Flavor (Unflavored, Flavored), By Packaging Type (Glass Bottles, Tins, Plastic Bottles, Others), By Sales Channel (On-Trade, Off-Trade (Retail Offline, Retail Online)) ... Read more

|

Major Players

|

Germany Alcoholic Drinks Market Statistics and Insights, 2026

- Market Size Statistics

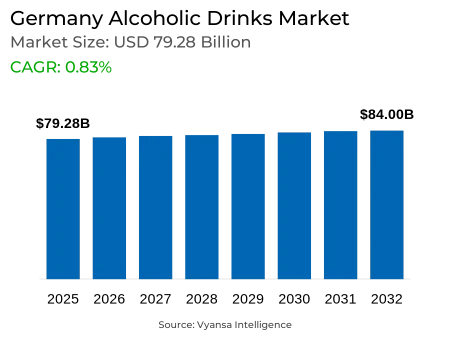

- Alcoholic Drinks in Germany is estimated at $ 79.28 Billion.

- The market size is expected to grow to $ 84 Billion by 2032.

- Market to register a CAGR of around 0.83% during 2026-32.

- Type Shares

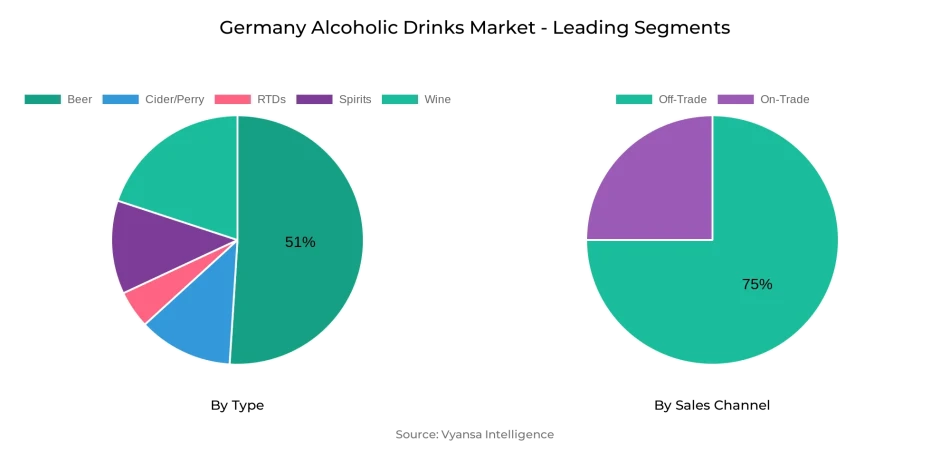

- Beer grabbed market share of 51%.

- Competition

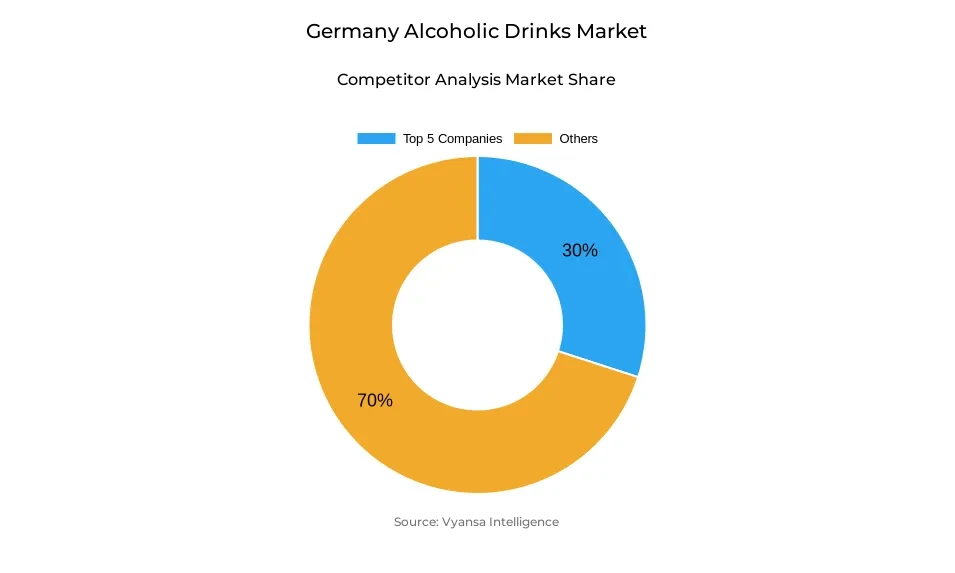

- More than 10 companies are actively engaged in producing Alcoholic Drinks in Germany.

- Top 5 companies acquired 30% of the market share.

- Carlsberg A/S, Oettinger Brauerei GmbH, Brauerei C & A Veltins GmbH & Co KG, Oetker-Gruppe, Paulaner Brauerei GmbH & Co KG etc., are few of the top companies.

- Sales Channel

- Off-Trade grabbed 75% of the market.

Germany Alcoholic Drinks Market Outlook

The Germany alcoholic drinks market was valued at USD 79.28 billion and is expected to grow to USD 84 billion by 2032. The growth during the forecast period will be moderate, indicating a mature market with changing end users behavior. Beer, the largest category, will continue to be pressured by decreasing consumption among young adults and price competition from RTDs and other alternative drinks. Domestic premium lager will be the leading segment, with a range of styles including Helles, to benefit from, while imported and low-alcohol beers will enjoy steady growth through innovation and focused promotions.

RTDs will experience good volume growth, boosted by spirit-based variants among younger drinkers. Innovation in products with energy-giving and flavour varieties, plus strategic promotions, will drive increased occasions of consumption. Non-alcoholic beers and spirits will be on the rise, influenced by growing health consciousness and the need for lower-alcohol products. The movement towards apéritifs and non-alcoholic ranges of well-known spirits, including Finsbury 0.0 and Ramazzotti Aperitivo 0.0%, will continue to influence the market over the next few years.

Off-trade will continue to be the dominant channel, with approximately 75% of market share. Supermarkets and discounters, particularly Aldi and Lidl, will still lead the way through aggressive promotion and pricing. Independent local grocers will also be active, notably for RTDs, based on convenience and proximity to end users. Channels such as on-trade will gradually return as foodservice establishments rebuild, but growth in volume will be constrained by fewer numbers of establishments, greater operating costs, and ongoing popularity in the home entertainment area.

In the future, the market will experience steady growth driven by premiumisation, innovation, and changing end users behaviour. Innovative and affordable alcoholic beverages that harmonise quality, taste, and convenience will be key to value capture in a constrained end users setting. Non-alcoholic and low-alcohol alternatives will grow in response to health-aware end users, and RTDs and flavoured spirits will remain popular among younger audiences. In total, the German Alcoholic Drinks Market is predicted to increase steadily, registering a value of USD 84 billion in 2032.

Germany Alcoholic Drinks Market Growth Driver

Increasing Demand for Non-Alcoholic Drinks

Growing health awareness among German end users propels the growth of non-alcoholic drinks. German end users are increasingly looking for substitutes for normal alcoholic beverages, hence creating a boost in demand for non-alcoholic beer, wine, and spirits. Leading brands are increasing shelf space and promotion efforts to reach this segment, further increasing its share in the market.

Non-alcoholic alternatives are also popularizing owing to changing lifestyles, with young end users more so opting for a drink that permits moderation or total abstinence from alcohol. Product innovations, such as enhanced brewing processes that retain taste without alcohol, enhance these beverages' appeal. Therefore, non-alcoholic drinks are a key growth driver, appealing to more end users and motivating greater frequency of purchase.

Germany Alcoholic Drinks Market Trend

Rise of RTDs with Functional Ingredients

Ready-to-Drink (RTD) drinks are adding more functional ingredients, to target younger end users. RTDs are providing convenience and new experience, in line with changing end users attitudes for on-trade beverages that offer alcohol combined with added value. The innovation of energy-boosting RTDs signifies the move of the market towards experimentation and creativity.

In addition to spirit-based RTDs, the increasing number of products with different end users segments and occasions reinforces this trend. New product launches with distinct flavors, together with promotional efforts, fuel end users demand. RTDs continue to increase their popularity, engaging young adults who prioritize convenience, flavor, and functional characteristics, influencing the future consumption pattern in the German Alcoholic Drinks Market .

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany Alcoholic Drinks Market Opportunity

Expansion of Non-Alcoholic Variants

The German Alcoholic Drinks Market shows a strong opportunity in growing non-alcoholic versions of well-known spirits and apéritifs. In the next few years, brands will introduce new alcohol-free versions of established brands, mimicking the flavor and experience of classic drinks without alcohol. This enables companies to win over health-aware end users and individuals who desire moderation.

The movement is most pronounced in gin and apéritif segments, where non-alcoholic variants are expected to increase in popularity. Ongoing innovation and flavor creation will fuel end users uptake and create market differentiation. Investing in these launches allows companies to tap into untapped potential, grow their product lines, and deepen their position among new end users groups that focus on taste, well-being, and lifestyle preferences

Unlock Market Intelligence

Explore the market potential with our data-driven report

Germany Alcoholic Drinks Market Segmentation Analysis

By Type

- Beer

- Cider/Perry

- RTDs

- Spirits

- Wine

The segment with highest market share under Type is Beer, with 51% share of the whole German Alcoholic Drinks Market . Home premium lager was the biggest segment among beer, representing more than 40% of the volume sales of beer, and keeps the end users drawn with a varied range of beer styles. Increasing popularity of Helles, a Bavarian-style lager characterized by light flavour, has also contributed to beer consumption.

Imported lagers and flavour/mix lager variants are also driving the growth in the beer segment. Non-alcoholic beer is also becoming popular, with recent new products like Augustiner Alkoholfrei Hell and Andechser Hell alkoholfrei widening the category. In-shop promotions and shelf display in supermarkets and discounters are supporting beer's market leading position.

By Sales Channel

- On-Trade

- Off-Trade

The segment with highest market share under sales channel is Off-Trade with 75% of the Alcoholic Drinks Market in Germany. Supermarkets are the leading distribution network, ably supported by discount stores like Aldi and Lidl, who have aggressive price promotion to woo end users. Convenience of access and proximity of Off-Trade outlets, complemented by robust marketing campaigns, drive beer, RTD, and spirits sales despite economic instability.

Small independent grocery stores are also a significant contributor, especially for Ready-to-Drink products, where convenience and on-the-go consumption are crucial drivers. Hypermarkets and specialist stores complement the wider market with carefully curated and non-alcoholic portfolios for health-conscious or specialist end users. As a whole, Off-Trade remains ahead of On-Trade through convenience, competitive pricing, and wider availability across regions.

Top Companies in Germany Alcoholic Drinks Market

The top companies operating in the market include Carlsberg A/S, Oettinger Brauerei GmbH, Brauerei C & A Veltins GmbH & Co KG, Oetker-Gruppe, Paulaner Brauerei GmbH & Co KG, Anheuser-Busch InBev NV, Bitburger Braugruppe GmbH, Krombacher Brauerei Bhd Schadeberg GmbH & Co KG, Warsteiner Brauerei Haus Cramer GmbH & Co KG, Rotkäppchen-Mumm Sektkellereien GmbH, etc., are the top players operating in the Germany Alcoholic Drinks Market.

Frequently Asked Questions

Related Report

1. Market Segmentation

1.1. Research Scope

1.2. Research Methodology

1.3. Definitions and Assumptions

2. Executive Summary

3. Germany Alcoholic Drinks Market Policies, Regulations, and Standards

4. Germany Alcoholic Drinks Market Dynamics

4.1. Growth Factors

4.2. Challenges

4.3. Trends

4.4. Opportunities

5. Germany Alcoholic Drinks Market Statistics, 2022-2032F

5.1. Market Size & Growth Outlook

5.1.1. By Revenues in US$ Million

5.1.2. By Quantity Sold in Million Litres

5.2. Market Segmentation & Growth Outlook

5.2.1. By Type

5.2.1.1. Beer- Market Insights and Forecast 2022-2032, USD Million

5.2.1.2. Cider/Perry- Market Insights and Forecast 2022-2032, USD Million

5.2.1.3. RTDs- Market Insights and Forecast 2022-2032, USD Million

5.2.1.4. Spirits- Market Insights and Forecast 2022-2032, USD Million

5.2.1.5. Wine- Market Insights and Forecast 2022-2032, USD Million

5.2.2. By Alcohol Content

5.2.2.1. High- Market Insights and Forecast 2022-2032, USD Million

5.2.2.2. Medium- Market Insights and Forecast 2022-2032, USD Million

5.2.2.3. Low- Market Insights and Forecast 2022-2032, USD Million

5.2.3. By Flavor

5.2.3.1. Unflavored- Market Insights and Forecast 2022-2032, USD Million

5.2.3.2. Flavored- Market Insights and Forecast 2022-2032, USD Million

5.2.4. By Packaging Type

5.2.4.1. Glass Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.2. Tins- Market Insights and Forecast 2022-2032, USD Million

5.2.4.3. Plastic Bottles- Market Insights and Forecast 2022-2032, USD Million

5.2.4.4. Others- Market Insights and Forecast 2022-2032, USD Million

5.2.5. By Sales Channel

5.2.5.1. On-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2. Off-Trade- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2.1. Retail Offline- Market Insights and Forecast 2022-2032, USD Million

5.2.5.2.2. Retail Online- Market Insights and Forecast 2022-2032, USD Million

5.2.6. By Competitors

5.2.6.1. Competition Characteristics

5.2.6.2. Market Share & Analysis

6. Germany Beer Market Statistics, 2022-2032F

6.1. Market Size & Growth Outlook

6.1.1. By Revenues in US$ Million

6.1.2. By Quantity Sold in Million Litres

6.2. Market Segmentation & Growth Outlook

6.2.1. By Alcohol Content- Market Insights and Forecast 2022-2032, USD Million

6.2.2. By Flavor- Market Insights and Forecast 2022-2032, USD Million

6.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

6.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

7. Germany Cider/Perry Market Statistics, 2022-2032F

7.1. Market Size & Growth Outlook

7.1.1. By Revenues in US$ Million

7.1.2. By Quantity Sold in Million Litres

7.2. Market Segmentation & Growth Outlook

7.2.1. By Alcohol Content- Market Insights and Forecast 2022-2032, USD Million

7.2.2. By Flavor- Market Insights and Forecast 2022-2032, USD Million

7.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

7.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

8. Germany Ready-to-Drink Market Statistics, 2022-2032F

8.1. Market Size & Growth Outlook

8.1.1. By Revenues in US$ Million

8.1.2. By Quantity Sold in Million Litres

8.2. Market Segmentation & Growth Outlook

8.2.1. By Alcohol Content- Market Insights and Forecast 2022-2032, USD Million

8.2.2. By Flavor- Market Insights and Forecast 2022-2032, USD Million

8.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

8.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

9. Germany Spirits Market Statistics, 2022-2032F

9.1. Market Size & Growth Outlook

9.1.1. By Revenues in US$ Million

9.1.2. By Quantity Sold in Million Litres

9.2. Market Segmentation & Growth Outlook

9.2.1. By Alcohol Content- Market Insights and Forecast 2022-2032, USD Million

9.2.2. By Flavor- Market Insights and Forecast 2022-2032, USD Million

9.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

9.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

10. Germany Wine Market Statistics, 2022-2032F

10.1.Market Size & Growth Outlook

10.1.1. By Revenues in US$ Million

10.1.2. By Quantity Sold in Million Litres

10.2.Market Segmentation & Growth Outlook

10.2.1. By Alcohol Content- Market Insights and Forecast 2022-2032, USD Million

10.2.2. By Flavor- Market Insights and Forecast 2022-2032, USD Million

10.2.3. By Packaging Type- Market Insights and Forecast 2022-2032, USD Million

10.2.4. By Sales Channel- Market Insights and Forecast 2022-2032, USD Million

11. Competitive Outlook

11.1.Company Profiles

11.1.1. Oetker-Gruppe

11.1.1.1. Business Description

11.1.1.2. Product Portfolio

11.1.1.3. Collaborations & Alliances

11.1.1.4. Recent Developments

11.1.1.5. Financial Details

11.1.1.6. Others

11.1.2. Paulaner Brauerei GmbH & Co KG

11.1.2.1. Business Description

11.1.2.2. Product Portfolio

11.1.2.3. Collaborations & Alliances

11.1.2.4. Recent Developments

11.1.2.5. Financial Details

11.1.2.6. Others

11.1.3. Anheuser-Busch InBev NV

11.1.3.1. Business Description

11.1.3.2. Product Portfolio

11.1.3.3. Collaborations & Alliances

11.1.3.4. Recent Developments

11.1.3.5. Financial Details

11.1.3.6. Others

11.1.4. Bitburger Braugruppe GmbH

11.1.4.1. Business Description

11.1.4.2. Product Portfolio

11.1.4.3. Collaborations & Alliances

11.1.4.4. Recent Developments

11.1.4.5. Financial Details

11.1.4.6. Others

11.1.5. Krombacher Brauerei Bhd Schadeberg GmbH & Co KG

11.1.5.1. Business Description

11.1.5.2. Product Portfolio

11.1.5.3. Collaborations & Alliances

11.1.5.4. Recent Developments

11.1.5.5. Financial Details

11.1.5.6. Others

11.1.6. Carlsberg A/S

11.1.6.1. Business Description

11.1.6.2. Product Portfolio

11.1.6.3. Collaborations & Alliances

11.1.6.4. Recent Developments

11.1.6.5. Financial Details

11.1.6.6. Others

11.1.7. Oettinger Brauerei GmbH

11.1.7.1. Business Description

11.1.7.2. Product Portfolio

11.1.7.3. Collaborations & Alliances

11.1.7.4. Recent Developments

11.1.7.5. Financial Details

11.1.7.6. Others

11.1.8. Brauerei C & A Veltins GmbH & Co KG

11.1.8.1. Business Description

11.1.8.2. Product Portfolio

11.1.8.3. Collaborations & Alliances

11.1.8.4. Recent Developments

11.1.8.5. Financial Details

11.1.8.6. Others

11.1.9. Warsteiner Brauerei Haus Cramer GmbH & Co KG

11.1.9.1. Business Description

11.1.9.2. Product Portfolio

11.1.9.3. Collaborations & Alliances

11.1.9.4. Recent Developments

11.1.9.5. Financial Details

11.1.9.6. Others

11.1.10. Rotkäppchen-Mumm Sektkellereien GmbH

11.1.10.1. Business Description

11.1.10.2. Product Portfolio

11.1.10.3. Collaborations & Alliances

11.1.10.4. Recent Developments

11.1.10.5. Financial Details

11.1.10.6. Others

12. Disclaimer

| Segment | Sub-Segment |

|---|---|

| By Type |

|

| By Alcohol Content |

|

| By Flavor |

|

| By Packaging Type |

|

| By Sales Channel |

|

Research Methodology

This study followed a structured approach comprising four key phases to assess the size and scope of the electro-oxidation market. The process began with thorough secondary research to collect data on the target market, related markets, and broader industry context. These findings, along with preliminary assumptions and estimates, were then validated through extensive primary research involving industry experts from across the value chain. To calculate the overall market size, both top-down and bottom-up methodologies were employed. Finally, market segmentation and data triangulation techniques were applied to refine and validate segment-level estimations.

Secondary Research

The secondary research phase involved gathering data from a wide range of credible and published sources. This step helped in identifying industry trends, defining market segmentation, and understanding the market landscape and value chain.

Sources consulted during this phase included:

- Company annual reports, investor presentations, and press releases

- Industry white papers and certified publications

- Trade directories and market-recognized databases

- Articles from authoritative authors and reputable journals

- Gold and silver standard websites

Secondary research was critical in mapping out the industry's value chain and monetary flow, identifying key market segments, understanding regional variations, and tracking significant industry developments.

Other key sources:

- Financial disclosures

- Industry associations and trade bodies

- News outlets and business magazines

- Academic journals and research studies

- Paid industry databases

Primary Research

To validate secondary data and gain deeper market insights, primary research was conducted with key stakeholders across both the supply and demand sides of the market.

On the demand side, participants included decision-makers and influencers from end-user industries—such as CIOs, CTOs, and CSOs—who provided first-hand perspectives on market needs, product usage, and future expectations.

On the supply side, interviews were conducted with manufacturers, industry associations, and institutional participants to gather insights into current offerings, product pipelines, and market challenges.

Primary interviews provided critical inputs such as:

- Market size and revenue data

- Product and service breakdowns

- Market forecasts

- Regional and application-specific trends

Stakeholders consulted included:

- Leading OEM and solution providers

- Channel and distribution partners

- End users across various applications

- Independent consultants and industry specialists

Market Size Estimation and Data Triangulation

- Identifying Key Market Participants (Secondary Research)

- Goal: To identify the major players or companies in the target market. This typically involves using publicly available data sources such as industry reports, market research publications, and financial statements of companies.

- Tools: Reports from firms like Gartner, Forrester, Euromonitor, Statista, IBISWorld, and others. Public financial statements, news articles, and press releases from top market players.

- Extracting Earnings of Key Market Participants

- Goal: To estimate the earnings generated from the product or service being analyzed. This step helps in understanding the revenue potential of each market player in a specific geography.

- Methods: Earnings data can be gathered from:

- Publicly available financial reports (for listed companies).

- Interviews and primary data sources from professionals, such as Directors, VPs, SVPs, etc. This is especially useful for understanding more nuanced, internal data that isn't publicly disclosed.

- Annual reports and investor presentations of key players.

- Data Collation and Development of a Relevant Data Model

- Goal: To collate inputs from both primary and secondary sources into a structured, data-driven model for market estimation. This model will incorporate key market KPIs and any independent variables relevant to the market.

- Key KPIs: These could include:

- Market size, growth rate, and demand drivers.

- Industry-specific metrics like market share, average revenue per customer (ARPC), or average deal size.

- External variables, such as economic growth rates, inflation rates, or commodity prices, that could affect the market.

- Data Modeling: Based on this data, the market forecasts are developed for the next 5 years. A combination of trend analysis, scenario modeling, and statistical regression might be used to generate projections.

- Scenario Analysis

- Goal: To test different assumptions and validate how sensitive the market is to changes in key variables (e.g., market demand, regulatory changes, technological disruptions).

- Types of Scenarios:

- Base Case: Based on current assumptions and historical data.

- Best-Case Scenario: Assuming favorable market conditions, regulatory environments, and technological advancements.

- Worst-Case Scenario: Accounting for adverse factors, such as economic downturns, stricter regulations, or unexpected disruptions.